What is Global Fire Fighting Respirator Market?

The Global Fire Fighting Respirator Market is a specialized segment within the broader safety equipment industry, focusing on devices designed to protect firefighters from inhaling harmful substances during fire incidents. These respirators are crucial for ensuring the safety and health of firefighters as they navigate through smoke, toxic gases, and other hazardous environments. The market encompasses a variety of respirators, including air-purifying respirators (APRs) and atmosphere-supplying respirators (ASRs), each tailored to specific needs and scenarios encountered in firefighting. The demand for these respirators is driven by stringent safety regulations, increasing awareness about firefighter health, and advancements in technology that enhance the effectiveness and comfort of these devices. As fire incidents continue to pose significant risks globally, the importance of reliable and efficient firefighting respirators cannot be overstated. The market is characterized by continuous innovation, with manufacturers striving to develop respirators that offer better protection, ease of use, and durability.

Air-purifying Respirators, Atmosphere-supplying Respirators in the Global Fire Fighting Respirator Market:

Air-purifying respirators (APRs) and atmosphere-supplying respirators (ASRs) are two primary types of respirators used in the Global Fire Fighting Respirator Market. APRs work by filtering out contaminants from the air, making them suitable for environments where the air contains particulate matter, gases, or vapors that can be harmful if inhaled. These respirators typically include components such as filters, cartridges, and masks that fit snugly over the face to ensure that only purified air is inhaled. APRs are often used in situations where the air quality is compromised but still contains sufficient oxygen levels for breathing. On the other hand, ASRs provide a clean air supply from an external source, making them ideal for environments where the air is severely contaminated or lacks sufficient oxygen. ASRs include self-contained breathing apparatus (SCBA) and supplied-air respirators (SAR). SCBAs are commonly used by firefighters as they provide a portable air supply, allowing them to move freely in hazardous environments. SARs, however, are connected to an external air source via a hose, which can limit mobility but ensures a continuous supply of clean air. Both types of respirators are essential in firefighting operations, with the choice between APRs and ASRs depending on the specific conditions and risks present at the scene. The development and deployment of these respirators are guided by rigorous standards and regulations to ensure maximum protection for firefighters. Manufacturers in this market are continually innovating to improve the performance, comfort, and usability of these devices, incorporating advanced materials and technologies to enhance their effectiveness. The Global Fire Fighting Respirator Market is thus a dynamic and critical component of the broader safety equipment industry, playing a vital role in safeguarding the lives of those who risk their lives to protect others.

Fire Department, Corporation in the Global Fire Fighting Respirator Market:

The usage of firefighting respirators in fire departments and corporations is crucial for ensuring the safety and health of personnel involved in fire response and prevention activities. In fire departments, respirators are an essential part of the personal protective equipment (PPE) used by firefighters. These devices protect firefighters from inhaling smoke, toxic gases, and other hazardous substances encountered during fire suppression and rescue operations. The use of respirators allows firefighters to operate in environments with compromised air quality, enabling them to perform their duties effectively while minimizing health risks. Fire departments invest significantly in training their personnel on the proper use and maintenance of respirators to ensure they function correctly in critical situations. Additionally, regular drills and simulations are conducted to familiarize firefighters with the equipment and procedures, enhancing their readiness and response capabilities. In corporations, particularly those in industries with high fire risks such as manufacturing, chemical processing, and oil and gas, respirators are used as part of comprehensive fire safety and emergency response plans. These corporations are required to comply with occupational safety regulations that mandate the provision of appropriate respiratory protection for employees exposed to fire hazards. Respirators are used during fire drills, emergency evacuations, and in situations where employees must enter areas with poor air quality due to fire or chemical releases. The implementation of respirators in corporate settings involves thorough risk assessments, employee training, and regular equipment inspections to ensure compliance with safety standards. By equipping their workforce with reliable respirators, corporations not only protect their employees but also mitigate potential liabilities and enhance their overall safety culture. The integration of firefighting respirators in both fire departments and corporations underscores the importance of respiratory protection in safeguarding lives and maintaining operational continuity in the face of fire-related emergencies.

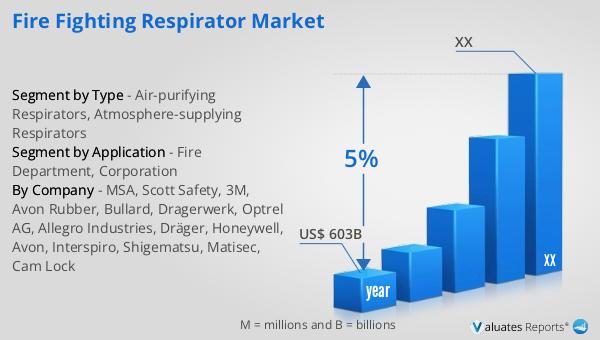

Global Fire Fighting Respirator Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately US$ 603 billion by the year 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory reflects the increasing demand for advanced medical technologies and innovations that enhance patient care and treatment outcomes. The medical device industry encompasses a wide range of products, including diagnostic equipment, surgical instruments, and life-support devices, all of which play a critical role in modern healthcare systems. The steady growth of this market is driven by factors such as the rising prevalence of chronic diseases, an aging global population, and ongoing advancements in medical technology. Additionally, the expansion of healthcare infrastructure in emerging economies and increased healthcare spending are contributing to the robust growth of the medical device market. As the industry continues to evolve, manufacturers are focusing on developing more efficient, cost-effective, and user-friendly devices to meet the diverse needs of healthcare providers and patients worldwide. The projected growth rate underscores the dynamic nature of the medical device market and its pivotal role in advancing global health outcomes.

| Report Metric | Details |

| Report Name | Fire Fighting Respirator Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | MSA, Scott Safety, 3M, Avon Rubber, Bullard, Dragerwerk, Optrel AG, Allegro Industries, Dräger, Honeywell, Avon, Interspiro, Shigematsu, Matisec, Cam Lock |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |