What is Global Veterinary Vaccine Adjuvants Market?

The Global Veterinary Vaccine Adjuvants Market is a specialized segment within the broader veterinary pharmaceuticals industry, focusing on substances that enhance the immune response of vaccines administered to animals. These adjuvants are crucial in ensuring that vaccines are effective in preventing diseases in both livestock and companion animals. The market is driven by the increasing demand for animal-derived food products, the rising prevalence of zoonotic diseases, and the growing awareness of animal health. Veterinary vaccine adjuvants are used to improve the efficacy of vaccines by enhancing the body's immune response to the vaccine antigen. This market is characterized by a variety of adjuvant types, including emulsions, minerals, and others, each offering unique benefits and applications. The market is also influenced by regulatory frameworks and technological advancements in vaccine development. As the global population continues to grow, so does the demand for safe and effective vaccines to protect animal health, which in turn supports the growth of the veterinary vaccine adjuvants market. The market is expected to continue expanding as new adjuvant technologies are developed and as the importance of animal health in the context of global food security becomes increasingly recognized.

Emulsion Adjuvants, Mineral Adjuvants, Others in the Global Veterinary Vaccine Adjuvants Market:

Emulsion adjuvants are a significant component of the Global Veterinary Vaccine Adjuvants Market, known for their ability to enhance the immune response by creating a depot effect, which allows for the slow release of the antigen. This slow release ensures prolonged exposure of the immune system to the antigen, thereby enhancing the immune response. Emulsion adjuvants are typically oil-in-water or water-in-oil emulsions, with each type offering distinct advantages. Oil-in-water emulsions are known for their ability to induce strong humoral and cellular immune responses, making them suitable for vaccines that require a robust immune response. Water-in-oil emulsions, on the other hand, are often used in vaccines where a prolonged immune response is desired. These adjuvants are particularly useful in vaccines for diseases that require long-term immunity. Mineral adjuvants, another key category, are primarily composed of aluminum salts, such as aluminum hydroxide and aluminum phosphate. These adjuvants are widely used due to their ability to enhance the immune response by promoting antigen uptake by antigen-presenting cells. Mineral adjuvants are known for their safety and efficacy, making them a popular choice in veterinary vaccines. They are particularly effective in inducing a strong antibody response, which is crucial for the prevention of many infectious diseases. Other types of adjuvants in the market include liposomes, saponins, and cytokines, each offering unique mechanisms of action and benefits. Liposomes are spherical vesicles that can encapsulate antigens, enhancing their delivery to the immune system. Saponins, derived from plant sources, are known for their ability to stimulate both humoral and cellular immune responses. Cytokines, which are proteins that modulate the immune response, are used as adjuvants to enhance the efficacy of vaccines by promoting a more targeted immune response. The choice of adjuvant depends on various factors, including the type of vaccine, the desired immune response, and the target animal species. The development of new adjuvant technologies continues to be a focus of research and innovation in the veterinary vaccine industry, with the aim of improving vaccine efficacy and safety. As the demand for effective vaccines continues to grow, the role of adjuvants in enhancing vaccine performance becomes increasingly important. The Global Veterinary Vaccine Adjuvants Market is poised for growth as new adjuvant technologies are developed and as the importance of animal health in the context of global food security becomes increasingly recognized.

Livestock Vaccines, Companion Animals Vaccines in the Global Veterinary Vaccine Adjuvants Market:

The usage of Global Veterinary Vaccine Adjuvants Market in livestock vaccines is critical for ensuring the health and productivity of farm animals. Livestock vaccines are designed to protect animals such as cattle, pigs, sheep, and poultry from infectious diseases that can significantly impact their health and productivity. Adjuvants play a crucial role in enhancing the efficacy of these vaccines by boosting the immune response, ensuring that the animals develop strong and long-lasting immunity. This is particularly important in the context of livestock farming, where disease outbreaks can lead to significant economic losses. By improving the efficacy of vaccines, adjuvants help to reduce the incidence of disease, improve animal welfare, and increase the efficiency of food production. In the case of companion animals, such as dogs and cats, vaccines are essential for preventing diseases that can affect their health and well-being. Adjuvants are used in companion animal vaccines to enhance the immune response, ensuring that pets are protected against a range of infectious diseases. The use of adjuvants in companion animal vaccines is driven by the increasing demand for pet healthcare and the growing awareness of the importance of preventive healthcare for pets. Adjuvants help to improve the efficacy of vaccines, ensuring that pets receive the best possible protection against diseases. The use of adjuvants in both livestock and companion animal vaccines is supported by ongoing research and development efforts aimed at improving vaccine efficacy and safety. As new adjuvant technologies are developed, the potential for improving the performance of veterinary vaccines continues to grow. The Global Veterinary Vaccine Adjuvants Market is expected to continue expanding as the demand for effective vaccines for both livestock and companion animals increases. The role of adjuvants in enhancing vaccine efficacy is critical for ensuring the health and well-being of animals, and for supporting the global food supply chain.

Global Veterinary Vaccine Adjuvants Market Outlook:

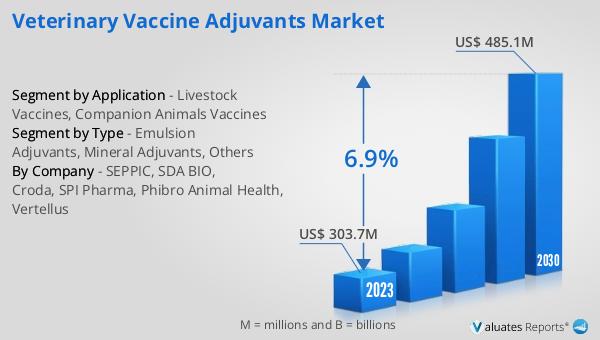

In 2024, the global market size for Veterinary Vaccine Adjuvants was valued at approximately US$ 345 million, with projections indicating it could reach around US$ 548 million by 2031, growing at a compound annual growth rate (CAGR) of 6.9% during the forecast period from 2025 to 2031. The market is dominated by the five largest manufacturers: SEPPIC, Croda, Vertellus, SPI Pharma, and SDA BIO, which collectively account for about 70% of the market share. SEPPIC leads the market with an estimated 35% share. Geographically, North America holds the largest market share, exceeding 30%, followed closely by the Asia-Pacific region and Europe, with shares of approximately 30% and 22%, respectively. Among the various product types, Emulsion Adjuvants represent the largest segment, comprising about 58% of the total market. This data highlights the significant role of key players and regions in shaping the market dynamics, as well as the predominant preference for emulsion adjuvants in veterinary vaccines. The market's growth is driven by the increasing demand for effective vaccines to protect animal health, supported by advancements in adjuvant technologies and the rising importance of animal health in global food security.

| Report Metric | Details |

| Report Name | Veterinary Vaccine Adjuvants Market |

| CAGR | 6.9% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | SEPPIC, SDA BIO, Croda, SPI Pharma, Phibro Animal Health, Vertellus |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |