What is Global Sulphur Recovery Market?

The Global Sulphur Recovery Market is a crucial segment of the energy and chemical industries, focusing on the extraction and recovery of sulphur from various industrial processes. Sulphur recovery is essential because sulphur compounds, particularly hydrogen sulfide (H2S), are often present in crude oil, natural gas, and other fossil fuels. These compounds need to be removed to prevent environmental pollution and to meet regulatory standards. The recovered sulphur is then used in various applications, including the production of sulfuric acid, fertilizers, and other chemicals. The market for sulphur recovery is driven by the increasing demand for clean energy and stringent environmental regulations that require industries to minimize their sulphur emissions. As industries continue to expand and environmental concerns grow, the demand for efficient sulphur recovery technologies is expected to rise. The market is characterized by the presence of several key players who are investing in research and development to improve the efficiency and cost-effectiveness of sulphur recovery processes. Overall, the Global Sulphur Recovery Market plays a vital role in promoting sustainable industrial practices and reducing the environmental impact of fossil fuel consumption.

Claus Process, Claus Process and Tail Gas Treatment in the Global Sulphur Recovery Market:

The Claus Process is a pivotal method in the Global Sulphur Recovery Market, primarily used to convert hydrogen sulfide (H2S) into elemental sulphur. This process is essential for industries dealing with natural gas and crude oil, where H2S is a common byproduct. The Claus Process involves two main stages: thermal and catalytic. In the thermal stage, H2S is partially combusted in a furnace to produce sulphur dioxide (SO2) and water. This reaction is exothermic, releasing significant heat, which is often utilized to generate steam for other industrial processes. The resulting gas mixture, containing SO2 and unreacted H2S, then enters the catalytic stage. Here, the gases pass over a series of catalysts, typically alumina or titanium dioxide, which facilitate the reaction between H2S and SO2 to form elemental sulphur and water. This process can achieve sulphur recovery efficiencies of up to 95-98%, making it highly effective for industrial applications. However, the Claus Process alone may not be sufficient to meet stringent environmental regulations, especially in regions with strict sulphur emission limits. This is where Tail Gas Treatment (TGT) comes into play. TGT processes are designed to treat the residual gases from the Claus Process, further reducing the sulphur content before the gases are released into the atmosphere. Various TGT methods exist, including the SCOT (Shell Claus Off-gas Treating) process, which uses a combination of hydrogenation and amine scrubbing to convert remaining sulphur compounds into H2S, which can then be recycled back into the Claus Process. Another method is the Beavon Sulfur Removal (BSR) process, which employs a similar approach but with different catalysts and operating conditions. These TGT processes can increase overall sulphur recovery efficiency to over 99%, ensuring compliance with environmental standards. The integration of the Claus Process and TGT is crucial for industries aiming to minimize their environmental footprint while maximizing sulphur recovery. As environmental regulations become more stringent, the demand for advanced sulphur recovery technologies is expected to grow, driving innovation and investment in this field. Companies are continuously exploring new catalysts, process optimizations, and energy-efficient solutions to enhance the performance of sulphur recovery systems. The Global Sulphur Recovery Market is thus a dynamic and evolving sector, with significant implications for environmental sustainability and industrial efficiency.

Petroleum and Coke, Natural Gas, Others in the Global Sulphur Recovery Market:

The Global Sulphur Recovery Market finds extensive applications across various sectors, including petroleum and coke, natural gas, and others. In the petroleum and coke industry, sulphur recovery is a critical process due to the high sulphur content in crude oil and petroleum products. Refineries employ sulphur recovery units to remove hydrogen sulfide (H2S) and other sulphur compounds from crude oil, ensuring compliance with environmental regulations and improving the quality of the final products. The recovered sulphur is often used to produce sulfuric acid, a key component in the manufacturing of fertilizers, chemicals, and other industrial products. In the natural gas sector, sulphur recovery is equally important. Natural gas often contains significant amounts of H2S, which must be removed to prevent corrosion in pipelines and equipment, as well as to meet safety and environmental standards. Sulphur recovery units in natural gas processing plants convert H2S into elemental sulphur, which can be sold or used in various applications. This not only helps in reducing emissions but also adds value to the natural gas production process. Beyond petroleum and natural gas, the Global Sulphur Recovery Market also serves other industries, such as chemical manufacturing and metal processing. In these sectors, sulphur recovery is essential for removing sulphur compounds from raw materials and waste streams, thereby minimizing environmental impact and enhancing process efficiency. The recovered sulphur can be utilized in the production of various chemicals, including sulfuric acid, which is widely used in the manufacture of fertilizers, detergents, and pharmaceuticals. Additionally, sulphur recovery plays a role in the production of construction materials, such as gypsum, which is used in cement and drywall manufacturing. Overall, the Global Sulphur Recovery Market is integral to a wide range of industries, providing environmental and economic benefits by reducing emissions, improving product quality, and creating valuable byproducts. As industries continue to prioritize sustainability and regulatory compliance, the demand for efficient sulphur recovery solutions is expected to grow, driving innovation and investment in this vital market.

Global Sulphur Recovery Market Outlook:

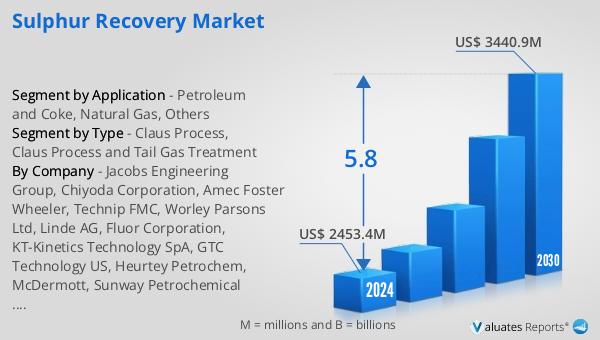

In 2024, the global market size for Sulphur Recovery was valued at approximately US$ 2,581 million, with projections indicating it could reach around US$ 3,810 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2025 to 2031. The Middle East and Africa region holds the largest share of the Sulphur Recovery Market, accounting for about 30% of the total market. Europe follows closely with a 25% market share. The industry is dominated by several key players, including Jacobs Engineering Group, Chiyoda Corporation, Amec Foster Wheeler, Technip FMC, and Worley Parsons Ltd. These top five manufacturers collectively hold approximately 50% of the market share, highlighting their significant influence and presence in the industry. The market's growth is driven by increasing environmental regulations and the need for cleaner energy solutions, prompting industries to adopt advanced sulphur recovery technologies. As the demand for sulphur recovery continues to rise, these leading companies are likely to play a crucial role in shaping the market's future, investing in research and development to enhance the efficiency and sustainability of sulphur recovery processes.

| Report Metric | Details |

| Report Name | Sulphur Recovery Market |

| CAGR | 5.8% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Jacobs Engineering Group, Chiyoda Corporation, Amec Foster Wheeler, Technip FMC, Worley Parsons Ltd, Linde AG, Fluor Corporation, KT-Kinetics Technology SpA, GTC Technology US, Heurtey Petrochem, McDermott, Sunway Petrochemical Engineering |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |