What is Global Semi-Closed Rebreather Market?

The Global Semi-Closed Rebreather Market refers to a specialized segment within the broader diving equipment industry, focusing on devices that allow divers to recycle a portion of the exhaled gas. These rebreathers are designed to extend dive times and reduce the amount of gas a diver needs to carry. Unlike open-circuit systems, which release exhaled gases into the environment, semi-closed rebreathers mix the exhaled gas with fresh gas, allowing for more efficient use of the breathing mixture. This technology is particularly beneficial for deep-sea divers, military operations, and scientific research, where extended underwater time is crucial. The market for these devices is driven by advancements in technology, increasing interest in underwater exploration, and the growing need for efficient diving solutions. As more industries recognize the benefits of semi-closed rebreathers, the demand for these systems is expected to rise, leading to innovations and improvements in design and functionality. The market is characterized by a mix of established manufacturers and new entrants, all striving to offer the most reliable and user-friendly products.

Active, Passive in the Global Semi-Closed Rebreather Market:

In the Global Semi-Closed Rebreather Market, the terms "active" and "passive" refer to the different operational mechanisms of these devices. Active semi-closed rebreathers are equipped with electronic systems that actively monitor and adjust the gas mixture being delivered to the diver. These systems use sensors to measure the partial pressures of oxygen and other gases, ensuring that the diver receives the optimal breathing mixture at all times. The active systems are often preferred by professional divers and those engaged in complex underwater tasks, as they offer a higher level of control and safety. On the other hand, passive semi-closed rebreathers rely on mechanical systems to regulate the gas mixture. These devices do not have electronic monitoring systems and instead use a fixed orifice or a constant mass flow system to deliver the breathing gas. While passive systems are generally simpler and more robust, they may not offer the same level of precision as active systems. However, they are often favored by recreational divers and those who prefer a more straightforward approach to diving. The choice between active and passive systems often depends on the diver's experience level, the nature of the dive, and personal preference. Both types of systems have their advantages and disadvantages, and the market continues to evolve as manufacturers strive to improve the safety, efficiency, and user experience of these devices. As technology advances, we can expect to see further innovations in both active and passive semi-closed rebreather systems, offering divers even more options to enhance their underwater adventures.

Commerical, Research, Personal, Others in the Global Semi-Closed Rebreather Market:

The Global Semi-Closed Rebreather Market finds its applications across various sectors, including commercial, research, personal, and others. In the commercial sector, these rebreathers are used extensively by professional divers engaged in underwater construction, maintenance, and repair work. The ability to stay underwater for extended periods without the need for frequent resurfacing makes semi-closed rebreathers an invaluable tool for commercial diving operations. In the research sector, scientists and marine biologists use these devices to conduct underwater studies and collect data on marine life and ecosystems. The extended dive times and reduced noise levels associated with semi-closed rebreathers allow researchers to observe marine life in its natural habitat without causing significant disturbances. For personal use, recreational divers are increasingly turning to semi-closed rebreathers to enhance their diving experiences. These devices offer the thrill of longer dives and the opportunity to explore deeper waters, making them a popular choice among diving enthusiasts. Additionally, the market also caters to other sectors, such as military and rescue operations, where the ability to operate stealthily and efficiently underwater is crucial. The versatility and adaptability of semi-closed rebreathers make them a valuable asset across these diverse applications, driving their demand and fostering innovation in the market.

Global Semi-Closed Rebreather Market Outlook:

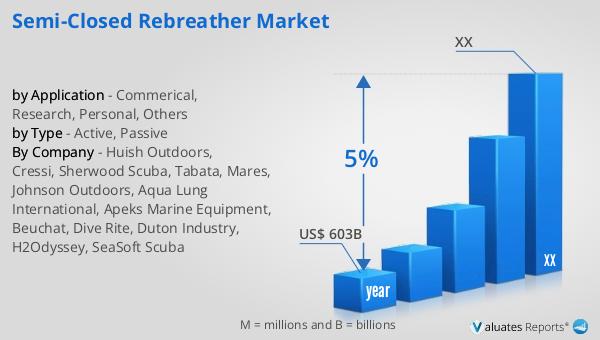

Our research indicates that the global market for medical devices, which includes the Global Semi-Closed Rebreather Market, is projected to be valued at approximately US$ 603 billion in 2023. This market is anticipated to experience a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including technological advancements, increasing demand for efficient and reliable medical devices, and the expanding applications of these devices across various sectors. The semi-closed rebreather market, as a part of this broader medical device market, is expected to benefit from these trends. As more industries recognize the advantages of semi-closed rebreathers, such as extended dive times and reduced environmental impact, the demand for these devices is likely to increase. Additionally, the growing interest in underwater exploration and the need for advanced diving solutions are expected to contribute to the market's growth. The market is characterized by a mix of established manufacturers and new entrants, all striving to offer innovative and user-friendly products. As the market continues to evolve, we can expect to see further advancements in technology and design, enhancing the safety, efficiency, and user experience of semi-closed rebreathers.

| Report Metric | Details |

| Report Name | Semi-Closed Rebreather Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Huish Outdoors, Cressi, Sherwood Scuba, Tabata, Mares, Johnson Outdoors, Aqua Lung International, Apeks Marine Equipment, Beuchat, Dive Rite, Duton Industry, H2Odyssey, SeaSoft Scuba |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |