What is Off-Road Heavy Duty Engines - Global Market?

Off-road heavy-duty engines are a crucial component of machinery used in various industries that require robust and reliable power sources. These engines are designed to operate in challenging environments, providing the necessary power for equipment that performs tasks in construction, agriculture, mining, and other industrial applications. Unlike standard engines, off-road heavy-duty engines are built to withstand harsh conditions such as extreme temperatures, dust, and uneven terrains. They are typically larger, more durable, and have higher torque outputs to handle the demanding tasks they are subjected to. The global market for these engines is driven by the increasing demand for infrastructure development, mechanized farming, and mining activities. As industries continue to expand and modernize, the need for efficient and powerful engines grows, making off-road heavy-duty engines an essential part of the global industrial landscape. These engines not only enhance productivity but also contribute to the overall efficiency and sustainability of operations by reducing downtime and maintenance costs. With advancements in technology, these engines are becoming more fuel-efficient and environmentally friendly, aligning with global efforts to reduce carbon emissions and promote sustainable industrial practices.

Single Cylinder, Multi Cylinder, Others in the Off-Road Heavy Duty Engines - Global Market:

Off-road heavy-duty engines can be categorized into single-cylinder, multi-cylinder, and other types, each serving distinct purposes based on their design and application. Single-cylinder engines are typically smaller and simpler in design, making them suitable for applications where space and weight are constraints. They are often used in smaller machinery and equipment that require less power, such as compact tractors, small construction equipment, and certain types of agricultural machinery. The simplicity of single-cylinder engines makes them easier to maintain and repair, which is advantageous in remote or rural areas where access to specialized services might be limited. However, their power output is limited compared to multi-cylinder engines, which are more complex and capable of delivering higher power and torque. Multi-cylinder engines are the workhorses of the off-road heavy-duty engine market, providing the necessary power for larger and more demanding applications. These engines are commonly found in heavy construction equipment like bulldozers, excavators, and large agricultural machinery such as combines and harvesters. The multiple cylinders allow for smoother operation and greater power output, making them ideal for tasks that require sustained heavy-duty performance. Additionally, multi-cylinder engines are often equipped with advanced technologies that enhance fuel efficiency and reduce emissions, aligning with global environmental standards. Other types of off-road heavy-duty engines include those powered by alternative fuels such as natural gas or electricity. These engines are gaining traction as industries seek to reduce their carbon footprint and comply with stricter environmental regulations. Electric engines, in particular, are becoming more popular in applications where noise reduction and zero emissions are critical, such as in urban construction sites or environmentally sensitive areas. The versatility of off-road heavy-duty engines allows them to be tailored to specific needs, ensuring that industries can choose the most appropriate engine type for their operations. As technology continues to evolve, the development of more efficient and environmentally friendly engines will likely drive further growth in the global market for off-road heavy-duty engines.

Construction Industry, Agriculture, Mining, Industry, Others in the Off-Road Heavy Duty Engines - Global Market:

Off-road heavy-duty engines play a vital role in various sectors, including construction, agriculture, mining, and other industrial applications. In the construction industry, these engines power a wide range of equipment such as bulldozers, excavators, and cranes, which are essential for building infrastructure like roads, bridges, and buildings. The reliability and power of off-road heavy-duty engines ensure that construction projects can be completed efficiently and on time, even in challenging environments. In agriculture, these engines are used in tractors, harvesters, and other machinery that help farmers increase productivity and manage large-scale farming operations. The ability to operate in diverse weather conditions and terrains makes off-road heavy-duty engines indispensable for modern agriculture, where efficiency and sustainability are key. In the mining sector, off-road heavy-duty engines are used in equipment such as haul trucks, loaders, and drills, which are essential for extracting and transporting minerals and other resources. The harsh conditions of mining operations require engines that can withstand extreme temperatures, dust, and heavy loads, making off-road heavy-duty engines the preferred choice for this industry. Beyond these sectors, off-road heavy-duty engines are also used in various industrial applications, including material handling, forestry, and oil and gas exploration. Their versatility and durability make them suitable for a wide range of tasks, from powering forklifts and logging equipment to driving pumps and compressors in remote locations. As industries continue to evolve and face new challenges, the demand for reliable and efficient off-road heavy-duty engines is expected to grow, driving innovation and development in this critical market.

Off-Road Heavy Duty Engines - Global Market Outlook:

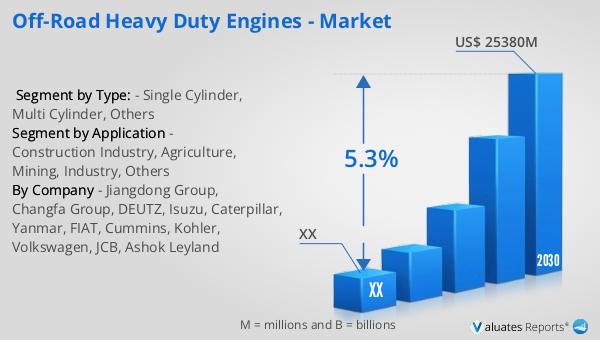

The global market for off-road heavy-duty engines was valued at approximately $17,530 million in 2023, with projections indicating a growth to around $25,380 million by 2030. This represents a compound annual growth rate (CAGR) of 5.3% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for robust and efficient engines across various industries, including construction, agriculture, and mining. The North American market, in particular, is expected to see significant growth, although specific figures were not provided. The rising need for infrastructure development, mechanized farming, and resource extraction are key factors contributing to the expansion of the off-road heavy-duty engine market. As industries continue to modernize and adopt more sustainable practices, the demand for engines that offer higher efficiency and lower emissions is expected to rise. This trend is further supported by advancements in technology that enhance the performance and environmental compatibility of these engines. Overall, the global market for off-road heavy-duty engines is poised for substantial growth, driven by the increasing need for powerful and reliable engines in various industrial applications.

| Report Metric | Details |

| Report Name | Off-Road Heavy Duty Engines - Market |

| Forecasted market size in 2030 | US$ 25380 million |

| CAGR | 5.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Jiangdong Group, Changfa Group, DEUTZ, Isuzu, Caterpillar, Yanmar, FIAT, Cummins, Kohler, Volkswagen, JCB, Ashok Leyland |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |