What is Companion Cancer Diagnostics - Global Market?

Companion cancer diagnostics represent a significant advancement in the global healthcare market, offering personalized treatment options for cancer patients. These diagnostics are tests or tools used alongside specific cancer therapies to determine their suitability for individual patients. By analyzing genetic, protein, or other molecular markers, companion diagnostics help identify which patients are most likely to benefit from a particular treatment, thereby enhancing the efficacy and safety of cancer therapies. This approach not only improves patient outcomes but also reduces unnecessary side effects and healthcare costs by avoiding ineffective treatments. The global market for companion cancer diagnostics is expanding rapidly, driven by the increasing prevalence of cancer, advancements in precision medicine, and growing awareness about personalized healthcare solutions. As pharmaceutical companies continue to develop targeted therapies, the demand for companion diagnostics is expected to rise, making it a crucial component of modern cancer care. This market is characterized by continuous innovation, with new diagnostic tests being developed to match the growing pipeline of targeted cancer therapies. Overall, companion cancer diagnostics play a vital role in the shift towards more personalized and effective cancer treatment strategies worldwide.

Breast Cancer, Lung Cancer, Colorectal Cancer, Melanoma, Gastric Cancer in the Companion Cancer Diagnostics - Global Market:

Breast cancer is one of the most common cancers affecting women globally, and companion cancer diagnostics have become essential in its management. These diagnostics help identify specific biomarkers, such as hormone receptors and HER2 status, which are crucial in determining the most effective treatment plan. For instance, patients with HER2-positive breast cancer can benefit from targeted therapies like trastuzumab, which specifically addresses this protein. Similarly, hormone receptor-positive cancers can be treated with hormone-blocking therapies, making companion diagnostics vital in tailoring treatment plans. Lung cancer, another prevalent cancer type, benefits significantly from companion diagnostics. These tests can identify mutations in genes such as EGFR, ALK, and ROS1, which are targets for specific drugs. By determining the genetic makeup of a lung tumor, healthcare providers can prescribe targeted therapies that improve survival rates and reduce side effects compared to traditional chemotherapy. Colorectal cancer, which affects the colon or rectum, also sees advancements through companion diagnostics. Tests for KRAS, NRAS, and BRAF mutations help oncologists decide on the best course of treatment, particularly when considering the use of EGFR inhibitors. These diagnostics ensure that patients receive the most effective therapies based on their tumor's genetic profile. Melanoma, a type of skin cancer, has seen a revolution in treatment options thanks to companion diagnostics. Tests for BRAF mutations, for example, allow for the use of targeted therapies like vemurafenib, which specifically inhibit the mutated protein driving cancer growth. This personalized approach has significantly improved outcomes for patients with advanced melanoma. Gastric cancer, or stomach cancer, is another area where companion diagnostics are making a difference. HER2 testing in gastric cancer patients can identify those who may benefit from trastuzumab, similar to its use in breast cancer. Additionally, testing for PD-L1 expression can guide the use of immunotherapies, offering new hope for patients with advanced disease. Overall, companion cancer diagnostics are transforming the landscape of cancer treatment by enabling more precise and effective therapies tailored to individual patients' needs.

Pharmaceutical & Biopharmaceutical Companies, Reference Laboratories, CROs, Others in the Companion Cancer Diagnostics - Global Market:

Companion cancer diagnostics play a crucial role in various sectors, including pharmaceutical and biopharmaceutical companies, reference laboratories, contract research organizations (CROs), and others. In pharmaceutical and biopharmaceutical companies, these diagnostics are integral to the development and commercialization of targeted therapies. By identifying specific biomarkers associated with cancer, these companies can design drugs that precisely target these markers, improving treatment efficacy and patient outcomes. Companion diagnostics also facilitate the regulatory approval process by providing evidence of a drug's effectiveness in specific patient populations. Reference laboratories are key players in the companion cancer diagnostics market, offering specialized testing services to healthcare providers. These labs perform complex molecular and genetic tests that are essential for identifying the biomarkers needed to guide treatment decisions. By providing accurate and timely results, reference laboratories help ensure that patients receive the most appropriate therapies based on their unique cancer profiles. Contract research organizations (CROs) also benefit from the growth of the companion cancer diagnostics market. These organizations conduct clinical trials and research studies on behalf of pharmaceutical companies, and companion diagnostics are often used to stratify patients and assess treatment responses. By incorporating these diagnostics into their studies, CROs can enhance the quality and relevance of their research, ultimately contributing to the development of more effective cancer therapies. Other stakeholders in the companion cancer diagnostics market include healthcare providers, payers, and patients. Healthcare providers rely on these diagnostics to make informed treatment decisions, while payers use them to justify the cost of targeted therapies. Patients, on the other hand, benefit from more personalized and effective treatment options that improve their quality of life and survival rates. Overall, the companion cancer diagnostics market is a dynamic and rapidly evolving field that is transforming the way cancer is diagnosed and treated across various sectors.

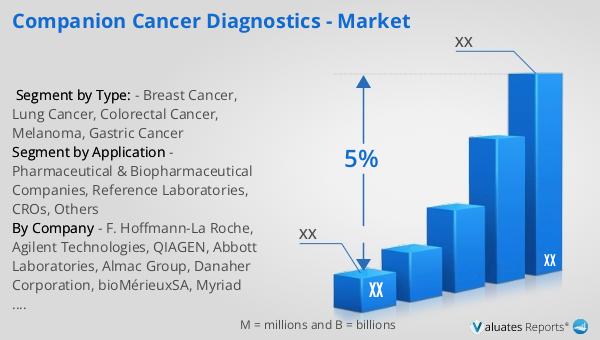

Companion Cancer Diagnostics - Global Market Outlook:

The global pharmaceutical market was valued at approximately 1,475 billion USD in 2022, with projections indicating a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in drug development, and rising healthcare expenditures worldwide. In comparison, the chemical drug market has shown a steady increase, growing from 1,005 billion USD in 2018 to an estimated 1,094 billion USD in 2022. This growth reflects the ongoing demand for chemical-based therapies, which continue to play a significant role in the treatment of various medical conditions. The expansion of the pharmaceutical market, including both chemical and biological drugs, underscores the importance of innovation and research in developing new and effective treatments. As the market continues to evolve, the integration of companion diagnostics is expected to further enhance the precision and efficacy of cancer therapies, contributing to the overall growth and transformation of the healthcare industry. The increasing focus on personalized medicine and targeted therapies highlights the critical role of companion diagnostics in shaping the future of cancer treatment and improving patient outcomes.

| Report Metric | Details |

| Report Name | Companion Cancer Diagnostics - Market |

| CAGR | 5% |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | F. Hoffmann-La Roche, Agilent Technologies, QIAGEN, Abbott Laboratories, Almac Group, Danaher Corporation, bioMérieuxSA, Myriad Genetics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |