What is Global Vehicle 4D Imaging Radar Market?

The Global Vehicle 4D Imaging Radar Market is a rapidly evolving sector within the automotive industry, focusing on advanced radar technology that provides high-resolution imaging for vehicles. Unlike traditional radar systems that offer limited dimensional data, 4D imaging radar captures detailed information about the environment, including the height, distance, speed, and direction of objects. This technology is crucial for enhancing the safety and efficiency of autonomous and semi-autonomous vehicles. It enables precise object detection and tracking, even in challenging weather conditions or poor visibility. The market is driven by the increasing demand for advanced driver-assistance systems (ADAS) and the growing trend towards autonomous driving. Major automotive manufacturers and tech companies are investing heavily in this technology to improve vehicle safety and performance. The integration of 4D imaging radar into vehicles is expected to revolutionize the automotive industry by providing more accurate and reliable data for navigation and collision avoidance systems. As a result, the Global Vehicle 4D Imaging Radar Market is poised for significant growth in the coming years, driven by technological advancements and increasing consumer demand for safer and smarter vehicles.

Single Radar-on-Chip, MIMO Multi-Chip Cascaded in the Global Vehicle 4D Imaging Radar Market:

Single Radar-on-Chip (RoC) and Multiple Input Multiple Output (MIMO) Multi-Chip Cascaded systems are two prominent technologies within the Global Vehicle 4D Imaging Radar Market. The Single Radar-on-Chip technology integrates all radar functions onto a single silicon chip, making it a compact and cost-effective solution for automotive applications. This integration simplifies the design and manufacturing process, reducing the overall cost and size of the radar system. Single RoC systems are particularly beneficial for passenger cars, where space and cost constraints are critical. They provide high-resolution imaging and accurate object detection, enhancing the vehicle's safety features. On the other hand, MIMO Multi-Chip Cascaded systems involve multiple radar chips working together to create a more comprehensive and detailed image of the vehicle's surroundings. This technology leverages the principles of MIMO, which uses multiple transmitters and receivers to improve the resolution and accuracy of the radar system. MIMO Multi-Chip Cascaded systems are ideal for commercial vehicles, which require more robust and reliable radar systems due to their larger size and higher operational demands. These systems provide superior performance in terms of range, resolution, and accuracy, making them suitable for applications such as long-haul trucking and fleet management. Both Single RoC and MIMO Multi-Chip Cascaded systems play a crucial role in the development of advanced driver-assistance systems (ADAS) and autonomous driving technologies. They enable vehicles to detect and track objects with high precision, even in challenging environments such as heavy traffic or adverse weather conditions. The integration of these technologies into vehicles enhances their safety, efficiency, and overall performance. As the demand for safer and smarter vehicles continues to grow, the adoption of Single RoC and MIMO Multi-Chip Cascaded systems is expected to increase, driving the growth of the Global Vehicle 4D Imaging Radar Market. These technologies represent a significant advancement in radar technology, offering improved performance and reliability compared to traditional radar systems. They are essential for the development of next-generation vehicles that can navigate complex environments and avoid collisions with greater accuracy. In summary, Single Radar-on-Chip and MIMO Multi-Chip Cascaded systems are key technologies within the Global Vehicle 4D Imaging Radar Market, providing high-resolution imaging and accurate object detection for both passenger and commercial vehicles. Their adoption is driven by the increasing demand for advanced driver-assistance systems and autonomous driving technologies, which require precise and reliable radar systems to ensure vehicle safety and performance.

Passenger Car, Commercial Car in the Global Vehicle 4D Imaging Radar Market:

The usage of Global Vehicle 4D Imaging Radar Market technology in passenger cars and commercial vehicles is transforming the automotive industry by enhancing safety and efficiency. In passenger cars, 4D imaging radar is primarily used to improve advanced driver-assistance systems (ADAS). These systems rely on high-resolution radar data to detect and track objects around the vehicle, such as other cars, pedestrians, and obstacles. The detailed imaging provided by 4D radar enables features like adaptive cruise control, lane-keeping assistance, and automatic emergency braking. These features enhance the safety of the vehicle by providing real-time data that helps prevent collisions and improve overall driving experience. Additionally, 4D imaging radar can operate effectively in various weather conditions and low visibility scenarios, making it a reliable technology for passenger cars. In commercial vehicles, the application of 4D imaging radar is even more critical due to the larger size and higher operational demands of these vehicles. Commercial vehicles, such as trucks and buses, require robust and reliable radar systems to ensure safe and efficient operation. 4D imaging radar provides detailed information about the vehicle's surroundings, enabling features like collision avoidance, blind-spot detection, and lane departure warning. These features are essential for preventing accidents and ensuring the safety of both the vehicle and its occupants. Moreover, 4D imaging radar is crucial for fleet management and logistics, as it provides real-time data that can be used to optimize routes, monitor vehicle performance, and improve overall operational efficiency. The integration of 4D imaging radar into commercial vehicles also supports the development of autonomous driving technologies. Autonomous trucks and buses rely on high-resolution radar data to navigate complex environments and avoid collisions. The detailed imaging provided by 4D radar enables these vehicles to detect and track objects with high precision, even in challenging conditions. This technology is essential for the safe and efficient operation of autonomous commercial vehicles, which are expected to play a significant role in the future of transportation. In summary, the usage of Global Vehicle 4D Imaging Radar Market technology in passenger cars and commercial vehicles is driving significant advancements in vehicle safety and efficiency. The detailed imaging provided by 4D radar enhances advanced driver-assistance systems and supports the development of autonomous driving technologies. As the demand for safer and smarter vehicles continues to grow, the adoption of 4D imaging radar is expected to increase, transforming the automotive industry and improving the overall driving experience.

Global Vehicle 4D Imaging Radar Market Outlook:

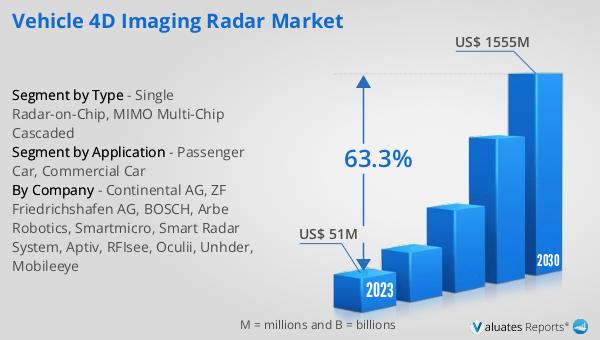

The global Vehicle 4D Imaging Radar market experienced a valuation of US$ 51 million in 2023 and is projected to soar to US$ 1555 million by 2030, reflecting a remarkable compound annual growth rate (CAGR) of 63.3% during the forecast period from 2024 to 2030. This substantial growth underscores the increasing demand for advanced radar technologies in the automotive industry. The rapid adoption of 4D imaging radar is driven by the need for enhanced vehicle safety and the growing trend towards autonomous driving. As more automotive manufacturers and tech companies invest in this technology, the market is expected to witness significant advancements and innovations. The integration of 4D imaging radar into vehicles is set to revolutionize the automotive industry by providing more accurate and reliable data for navigation and collision avoidance systems. This technology enables precise object detection and tracking, even in challenging weather conditions or poor visibility, making it a crucial component of advanced driver-assistance systems (ADAS) and autonomous driving technologies. The projected growth of the Global Vehicle 4D Imaging Radar Market highlights the increasing importance of this technology in the development of next-generation vehicles. As consumer demand for safer and smarter vehicles continues to rise, the market is poised for substantial expansion, driven by technological advancements and increasing investments from key industry players.

| Report Metric | Details |

| Report Name | Vehicle 4D Imaging Radar Market |

| Accounted market size in 2023 | US$ 51 million |

| Forecasted market size in 2030 | US$ 1555 million |

| CAGR | 63.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Continental AG, ZF Friedrichshafen AG, BOSCH, Arbe Robotics, Smartmicro, Smart Radar System, Aptiv, RFIsee, Oculii, Unhder, Mobileeye |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |