What is Global Medical Package Testing Market?

The Global Medical Package Testing Market is a specialized sector focused on ensuring the safety, integrity, and efficacy of medical packaging. This market encompasses a variety of testing methods and standards designed to evaluate the performance of packaging materials used for medical devices, pharmaceuticals, and other healthcare products. The primary goal is to ensure that these packages can protect their contents from contamination, physical damage, and environmental factors throughout their lifecycle, from manufacturing to end-use. This involves rigorous testing protocols that assess various attributes such as durability, seal integrity, and resistance to external factors like temperature and humidity. The market is driven by stringent regulatory requirements, technological advancements, and the increasing demand for safe and reliable medical products. As healthcare continues to evolve, the importance of robust medical package testing becomes even more critical, ensuring that patients receive safe and effective treatments.

Accelerated Package Aging Testing, Seal Strength Testing, Medical Package Performance Testing, Others in the Global Medical Package Testing Market:

Accelerated Package Aging Testing is a crucial component of the Global Medical Package Testing Market. This testing method simulates the long-term effects of environmental conditions on packaging materials in a shorter time frame. By exposing packages to elevated temperatures and humidity levels, manufacturers can predict how their products will perform over time. This is particularly important for medical devices and pharmaceuticals that may have extended shelf lives. Seal Strength Testing, on the other hand, focuses on the integrity of the seals used in medical packaging. A strong seal is essential to prevent contamination and ensure the sterility of the product. This testing involves applying pressure to the sealed areas and measuring their resistance to breaking. Medical Package Performance Testing encompasses a broader range of evaluations, including physical, chemical, and biological assessments. These tests ensure that the packaging can withstand various stresses during transportation, storage, and usage. Other testing methods in this market include microbial barrier testing, which assesses the package's ability to prevent microbial contamination, and biocompatibility testing, which ensures that the packaging materials do not cause adverse reactions when in contact with the human body. Each of these testing methods plays a vital role in ensuring the safety and efficacy of medical products, ultimately protecting patient health.

Pharmaceutical, Medical Industries in the Global Medical Package Testing Market:

The usage of the Global Medical Package Testing Market is particularly significant in the pharmaceutical and medical industries. In the pharmaceutical sector, packaging plays a critical role in maintaining the stability and efficacy of drugs. Medical package testing ensures that pharmaceutical products are protected from environmental factors such as moisture, light, and temperature fluctuations, which can degrade the active ingredients. This is especially important for sensitive medications like biologics and vaccines, which require stringent storage conditions. In the medical industry, packaging is equally crucial for devices such as syringes, implants, and diagnostic kits. These products must remain sterile and intact until they are used by healthcare professionals. Medical package testing verifies that the packaging can withstand the rigors of transportation and handling without compromising the sterility and functionality of the devices. Additionally, regulatory bodies like the FDA and EMA mandate rigorous testing standards for medical packaging to ensure patient safety. Compliance with these regulations is essential for market approval and commercialization of medical products. Overall, the Global Medical Package Testing Market provides the necessary assurance that medical and pharmaceutical products are safe, effective, and reliable, thereby supporting the broader healthcare ecosystem.

Global Medical Package Testing Market Outlook:

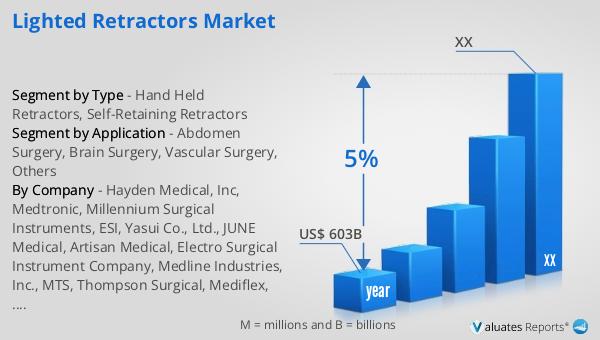

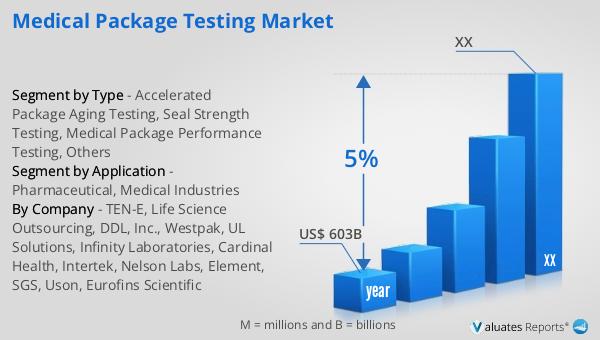

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing healthcare expenditure, and the rising prevalence of chronic diseases. The expanding elderly population also contributes to the demand for medical devices, as older individuals typically require more medical care. Additionally, emerging markets are experiencing rapid growth in healthcare infrastructure, further boosting the demand for medical devices. The continuous innovation in medical device technology, such as minimally invasive surgical instruments and advanced diagnostic tools, is also a significant driver of market growth. As the market expands, the importance of rigorous medical package testing becomes even more critical to ensure that these devices are safe and effective for patient use.

| Report Metric | Details |

| Report Name | Medical Package Testing Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | TEN-E, Life Science Outsourcing, DDL, Inc., Westpak, UL Solutions, Infinity Laboratories, Cardinal Health, Intertek, Nelson Labs, Element, SGS, Uson, Eurofins Scientific |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |