What is Global Lighted Surgical Retractor Market?

The Global Lighted Surgical Retractor Market refers to the worldwide industry focused on the production, distribution, and innovation of surgical retractors equipped with integrated lighting systems. These specialized medical devices are designed to enhance visibility and access during surgical procedures by illuminating the surgical site. The market encompasses a variety of retractors used in different types of surgeries, including abdominal, brain, and vascular surgeries, among others. The integration of lighting in these retractors helps surgeons perform more precise and efficient operations, reducing the risk of complications and improving patient outcomes. The market is driven by advancements in medical technology, increasing demand for minimally invasive surgeries, and the growing prevalence of chronic diseases requiring surgical intervention. As healthcare systems around the world continue to evolve, the Global Lighted Surgical Retractor Market is expected to expand, offering new opportunities for innovation and improved surgical care.

Hand Held Retractors, Self-Retaining Retractors in the Global Lighted Surgical Retractor Market:

Hand-held retractors and self-retaining retractors are two primary types of devices within the Global Lighted Surgical Retractor Market. Hand-held retractors are manually operated by the surgical team, requiring an assistant to hold and adjust the retractor during the procedure. These retractors are versatile and can be used in various types of surgeries, providing the surgeon with the flexibility to manipulate the surgical site as needed. The integration of lighting in hand-held retractors enhances visibility, allowing for more precise and efficient surgical interventions. On the other hand, self-retaining retractors are designed to hold themselves in place without the need for manual assistance. These retractors often come with adjustable arms and locking mechanisms that can be positioned to maintain a clear view of the surgical site. The built-in lighting in self-retaining retractors further improves visibility, reducing the need for additional lighting equipment in the operating room. Both types of retractors play a crucial role in modern surgical practices, offering distinct advantages depending on the specific requirements of the procedure. The choice between hand-held and self-retaining retractors often depends on factors such as the complexity of the surgery, the surgeon's preference, and the availability of surgical staff. As the Global Lighted Surgical Retractor Market continues to grow, innovations in both hand-held and self-retaining retractors are expected to enhance surgical outcomes and improve patient care.

Abdomen Surgery, Brain Surgery, Vascular Surgery, Others in the Global Lighted Surgical Retractor Market:

The usage of lighted surgical retractors in various types of surgeries highlights their importance in modern medical practices. In abdominal surgery, these retractors are essential for providing a clear view of the abdominal cavity, allowing surgeons to perform procedures such as appendectomies, hernia repairs, and bowel resections with greater precision. The integrated lighting helps to illuminate deep and narrow areas, reducing the risk of accidental damage to surrounding tissues and organs. In brain surgery, lighted retractors are crucial for maintaining a clear and well-lit surgical field, enabling neurosurgeons to navigate the complex structures of the brain with accuracy. These retractors help to minimize the risk of complications and improve the overall success rate of delicate brain surgeries. Vascular surgery also benefits significantly from the use of lighted retractors, as they provide enhanced visibility of blood vessels and surrounding tissues. This is particularly important in procedures such as aneurysm repairs, bypass surgeries, and the removal of blood clots, where precision is critical to prevent excessive bleeding and ensure proper blood flow. Additionally, lighted surgical retractors are used in various other types of surgeries, including orthopedic, thoracic, and plastic surgeries. In each of these areas, the integration of lighting in retractors helps to improve surgical outcomes by providing better visibility, reducing the risk of complications, and enhancing the overall efficiency of the surgical procedure. As the Global Lighted Surgical Retractor Market continues to evolve, the adoption of these advanced devices is expected to increase, further improving the quality of surgical care across different medical specialties.

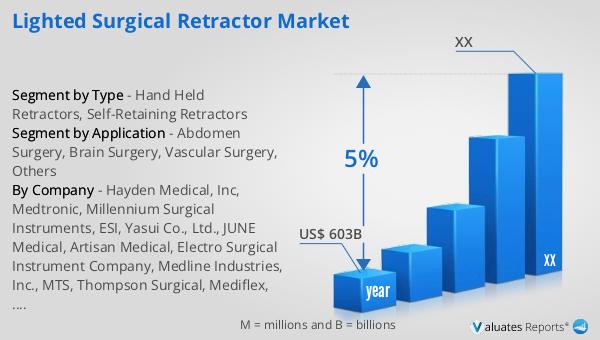

Global Lighted Surgical Retractor Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing demand for minimally invasive procedures, and the rising prevalence of chronic diseases that require surgical intervention. The integration of innovative features, such as lighting in surgical retractors, is a key contributor to the expansion of the market. These advancements not only enhance the precision and efficiency of surgical procedures but also improve patient outcomes by reducing the risk of complications. As healthcare systems worldwide continue to evolve and prioritize the adoption of advanced medical devices, the market for lighted surgical retractors is expected to see significant growth. This trend underscores the importance of continuous innovation and development in the medical device industry to meet the growing demands of modern healthcare.

| Report Metric | Details |

| Report Name | Lighted Surgical Retractor Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Hayden Medical, Inc, Medtronic, Millennium Surgical Instruments, ESI, Yasui Co., Ltd., JUNE Medical, Artisan Medical, Electro Surgical Instrument Company, Medline Industries, Inc., MTS, Thompson Surgical, Mediflex, Invuity, Roboz |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |