What is Global Flat Panel Antennas Market?

The Global Flat Panel Antennas Market refers to the industry focused on the development, production, and distribution of flat panel antennas. These antennas are characterized by their slim, flat design, which makes them highly suitable for various applications where space and aesthetics are important. Unlike traditional parabolic antennas, flat panel antennas offer a more compact and often more efficient solution for signal transmission and reception. They are used in a wide range of sectors, including telecommunications, military, aerospace, and maritime industries. The market for these antennas is driven by the increasing demand for high-speed internet and reliable communication systems, especially in remote and mobile environments. As technology advances, the capabilities of flat panel antennas continue to improve, making them an essential component in modern communication infrastructure. The market is also influenced by the growing need for advanced satellite communication systems, which require efficient and reliable antennas to function effectively. Overall, the Global Flat Panel Antennas Market is a dynamic and rapidly evolving industry with significant growth potential.

Electronically-steered Antenna, Mechanically-steered Antenna in the Global Flat Panel Antennas Market:

Electronically-steered antennas and mechanically-steered antennas are two primary types of flat panel antennas used in the Global Flat Panel Antennas Market. Electronically-steered antennas, also known as phased array antennas, use electronic signals to direct the antenna beam without moving the antenna itself. This technology allows for rapid and precise beam steering, making it ideal for applications that require quick adjustments and high accuracy, such as satellite communications and military operations. These antennas are highly efficient and can handle multiple signals simultaneously, which enhances their performance in complex communication environments. On the other hand, mechanically-steered antennas rely on physical movement to adjust the direction of the antenna beam. While they may not offer the same level of speed and precision as electronically-steered antennas, they are often more cost-effective and simpler to maintain. Mechanically-steered antennas are commonly used in applications where the antenna does not need to change direction frequently, such as in certain maritime and land-mobile communication systems. Both types of antennas have their unique advantages and are chosen based on the specific requirements of the application. The choice between electronically-steered and mechanically-steered antennas depends on factors such as cost, performance, and the operational environment. As the demand for reliable and efficient communication systems continues to grow, both types of antennas play a crucial role in meeting the needs of various industries.

Aerospace, Maritime, Land-mobile, Others in the Global Flat Panel Antennas Market:

The Global Flat Panel Antennas Market finds extensive usage in several key areas, including aerospace, maritime, land-mobile, and others. In the aerospace sector, flat panel antennas are essential for ensuring reliable communication between aircraft and ground stations. They provide high-speed data transmission and are crucial for navigation, surveillance, and in-flight connectivity. The compact design of flat panel antennas makes them ideal for use in aircraft, where space and weight are critical considerations. In the maritime industry, flat panel antennas are used for ship-to-shore communication, navigation, and tracking. They enable vessels to maintain constant communication with ports and other ships, ensuring safe and efficient operations. The ability to provide reliable communication in remote and harsh environments makes flat panel antennas indispensable for maritime applications. In land-mobile applications, flat panel antennas are used in vehicles such as trucks, buses, and emergency response vehicles. They provide reliable communication and internet connectivity on the move, which is essential for navigation, fleet management, and emergency response. The versatility and robustness of flat panel antennas make them suitable for use in various land-mobile applications. Additionally, flat panel antennas are used in other areas such as satellite communication, military operations, and remote sensing. Their ability to provide high-speed, reliable communication in diverse environments makes them a valuable asset in these applications. Overall, the Global Flat Panel Antennas Market plays a crucial role in enhancing communication and connectivity across various sectors.

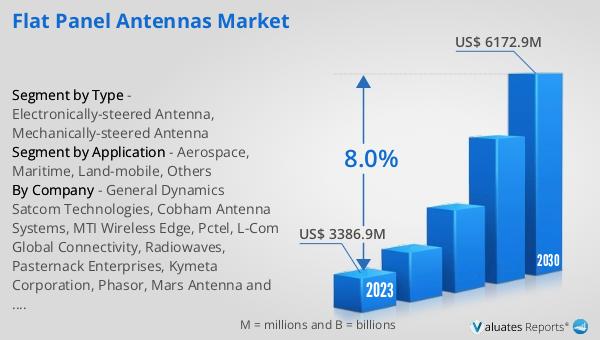

Global Flat Panel Antennas Market Outlook:

The global Flat Panel Antennas market was valued at US$ 3386.9 million in 2023 and is anticipated to reach US$ 6172.9 million by 2030, witnessing a CAGR of 8.0% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced communication systems and the expanding applications of flat panel antennas across various industries. The market's robust growth is driven by the need for reliable and efficient communication solutions in remote and mobile environments. As technology continues to evolve, the capabilities of flat panel antennas are expected to improve, further driving their adoption in the market. The growing demand for high-speed internet and advanced satellite communication systems is also contributing to the market's expansion. With the increasing reliance on communication systems for various applications, the Global Flat Panel Antennas Market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | Flat Panel Antennas Market |

| Accounted market size in 2023 | US$ 3386.9 million |

| Forecasted market size in 2030 | US$ 6172.9 million |

| CAGR | 8.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | General Dynamics Satcom Technologies, Cobham Antenna Systems, MTI Wireless Edge, Pctel, L-Com Global Connectivity, Radiowaves, Pasternack Enterprises, Kymeta Corporation, Phasor, Mars Antenna and RF Systems, ThinKom, SatCube, Starwin, SatPro, Gilat Satellite Networks, TTI Norte, L3Harria Technologies, Ball Aerospace, NXT Communications, ALCAN Systems, C-COM Satellites, Isotropic Systems, OneWeb, ST Engineering, Inmarsat |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |