What is Global Polyester TPU Films Market?

The Global Polyester TPU Films Market refers to the worldwide industry focused on the production and distribution of thermoplastic polyurethane (TPU) films made from polyester. These films are known for their exceptional properties such as high elasticity, transparency, and resistance to oil, grease, and abrasion. They are widely used in various applications due to their durability and versatility. The market encompasses a range of industries including automotive, construction, aerospace, medical, textiles, and sportswear. The demand for polyester TPU films is driven by their ability to provide superior performance in harsh environments, making them a preferred choice for manufacturers looking for reliable and high-quality materials. The market is characterized by continuous innovation and development to meet the evolving needs of different sectors, ensuring that the films remain relevant and effective in their applications.

Low Breathable TPU Film, Medium Breathable TPU Film, High Breathable TPU Film in the Global Polyester TPU Films Market:

Low Breathable TPU Film, Medium Breathable TPU Film, and High Breathable TPU Film are three categories within the Global Polyester TPU Films Market, each offering different levels of breathability to suit various applications. Low Breathable TPU Film is designed to allow minimal air and moisture permeability, making it ideal for applications where a high level of protection against external elements is required. This type of film is commonly used in protective clothing, medical devices, and packaging materials where maintaining a barrier is crucial. Medium Breathable TPU Film strikes a balance between breathability and protection, allowing for moderate air and moisture exchange. This makes it suitable for applications such as sportswear, outdoor gear, and footwear, where comfort and performance are important. High Breathable TPU Film offers the highest level of breathability, allowing for maximum air and moisture permeability. This type of film is often used in applications where ventilation and moisture management are critical, such as in high-performance athletic wear, medical textiles, and advanced filtration systems. Each type of breathable TPU film is engineered to meet specific performance criteria, ensuring that they provide the necessary functionality for their intended use. The development and innovation in breathable TPU films are driven by the need to enhance user comfort, improve product performance, and meet regulatory standards across various industries. The versatility of these films allows them to be tailored to specific requirements, making them a valuable component in a wide range of products.

Automotive, Construction, Aerospace & Defense, Medical & Healthcare, Textile, Sports Shoes and Clothing, Other in the Global Polyester TPU Films Market:

The usage of Global Polyester TPU Films Market spans across several key areas including automotive, construction, aerospace & defense, medical & healthcare, textile, sports shoes and clothing, and other sectors. In the automotive industry, polyester TPU films are used for interior and exterior applications such as protective coatings, seat covers, and dashboard components due to their durability and resistance to wear and tear. In construction, these films are utilized for waterproofing membranes, roofing materials, and protective barriers, providing long-lasting protection against environmental factors. The aerospace & defense sector benefits from the high-performance characteristics of polyester TPU films in applications such as aircraft interiors, protective gear, and flexible fuel tanks, where reliability and safety are paramount. In the medical & healthcare industry, polyester TPU films are used in medical devices, wound care products, and surgical drapes, offering biocompatibility and resistance to sterilization processes. The textile industry incorporates these films into fabrics to enhance durability, water resistance, and breathability, making them ideal for outdoor clothing, sportswear, and fashion items. Sports shoes and clothing manufacturers use polyester TPU films to improve the performance and comfort of their products, providing features such as moisture management, flexibility, and abrasion resistance. Other sectors that utilize polyester TPU films include packaging, electronics, and consumer goods, where the films' versatility and high-performance characteristics offer significant advantages. The widespread use of polyester TPU films across these diverse industries highlights their importance and the continuous demand for innovative solutions to meet specific application needs.

Global Polyester TPU Films Market Outlook:

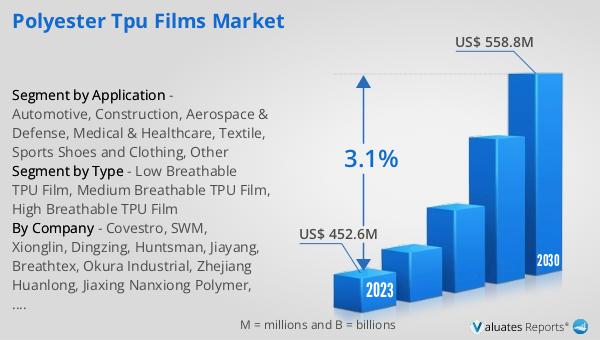

The global Polyester TPU Films market was valued at US$ 452.6 million in 2023 and is anticipated to reach US$ 558.8 million by 2030, witnessing a CAGR of 3.1% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for high-performance materials across various industries. The market's valuation reflects the significant role that polyester TPU films play in enhancing product performance and durability. The projected growth underscores the continuous innovation and development within the industry to meet the evolving needs of different sectors. As manufacturers seek reliable and high-quality materials, the demand for polyester TPU films is expected to rise, contributing to the market's expansion. The CAGR of 3.1% highlights the market's resilience and potential for sustained growth, driven by the ongoing advancements in technology and material science. This positive outlook for the global Polyester TPU Films market emphasizes the importance of these films in providing superior performance and meeting the stringent requirements of various applications.

| Report Metric | Details |

| Report Name | Polyester TPU Films Market |

| Accounted market size in 2023 | US$ 452.6 million |

| Forecasted market size in 2030 | US$ 558.8 million |

| CAGR | 3.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Covestro, SWM, Xionglin, Dingzing, Huntsman, Jiayang, Breathtex, Okura Industrial, Zhejiang Huanlong, Jiaxing Nanxiong Polymer, Takeda Sangyo, Dongguan TongLong, Permali Ltd, Taorun TPU, Novotex Italiana SpA, American Polyfilm, Wiman, Polysan, Asher |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |