What is Global Petroleum Flash Point Tester Market?

The Global Petroleum Flash Point Tester Market is a specialized segment within the broader testing and measurement industry. Flash point testers are essential instruments used to determine the lowest temperature at which a liquid can form an ignitable mixture in air. This is crucial for ensuring safety and compliance with various regulations in industries that handle flammable liquids. The market for these testers is driven by the need for accurate and reliable testing methods to prevent accidents and ensure the safe handling of petroleum products. The global market encompasses a range of products, including both open cup and closed cup flash point testers, each designed to meet specific testing requirements. The demand for these testers is influenced by factors such as the growth of the petroleum industry, stringent safety regulations, and the increasing need for quality control in various industrial processes. As industries continue to prioritize safety and compliance, the market for petroleum flash point testers is expected to grow steadily.

Open Cup Flash Point Tester, Closed Cup Flash Point Tester in the Global Petroleum Flash Point Tester Market:

Open Cup Flash Point Testers and Closed Cup Flash Point Testers are two primary types of instruments used in the Global Petroleum Flash Point Tester Market. Open cup testers, as the name suggests, involve an open sample container where the liquid is gradually heated, and a flame is passed over the surface at intervals to determine the flash point. This method is typically used for testing materials with higher flash points and is considered less precise than closed cup testing. However, it is still widely used due to its simplicity and cost-effectiveness. On the other hand, closed cup flash point testers involve a sealed container where the sample is heated, and the vapor is exposed to a flame through a small opening. This method is more accurate and is preferred for testing materials with lower flash points. Closed cup testers are often used in regulatory testing and quality control processes due to their higher precision and reproducibility. Both types of testers play a crucial role in ensuring the safety and compliance of petroleum products, with each having its own advantages and applications. The choice between open cup and closed cup testers depends on factors such as the type of material being tested, the required level of accuracy, and regulatory requirements. As the demand for reliable and accurate testing methods continues to grow, both open cup and closed cup flash point testers are expected to see increased adoption in various industries.

Chemical, Pharmaceutical, Oil, Other in the Global Petroleum Flash Point Tester Market:

The usage of Global Petroleum Flash Point Tester Market spans across several key industries, including Chemical, Pharmaceutical, Oil, and others. In the chemical industry, flash point testers are essential for ensuring the safe handling and storage of various chemicals. These instruments help in identifying the flammability characteristics of chemicals, which is crucial for preventing accidents and ensuring compliance with safety regulations. In the pharmaceutical industry, flash point testers are used to test the flammability of solvents and other liquid ingredients used in drug formulation and manufacturing. This helps in ensuring the safety of pharmaceutical products and compliance with regulatory standards. In the oil industry, flash point testers are used to determine the flammability of various petroleum products, including crude oil, gasoline, diesel, and lubricants. This is crucial for ensuring the safe transportation, storage, and handling of these products. Additionally, flash point testers are used in other industries such as food and beverage, cosmetics, and automotive, where the flammability of liquids needs to be assessed for safety and quality control purposes. The widespread usage of flash point testers across these industries highlights their importance in ensuring safety, compliance, and quality control. As industries continue to prioritize safety and regulatory compliance, the demand for reliable and accurate flash point testers is expected to grow.

Global Petroleum Flash Point Tester Market Outlook:

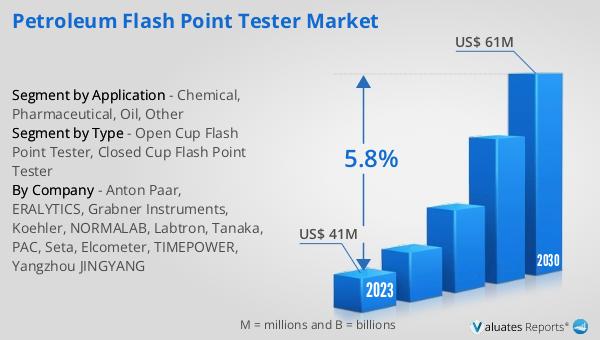

The global Petroleum Flash Point Tester market was valued at US$ 41 million in 2023 and is anticipated to reach US$ 61 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. This growth can be attributed to the increasing demand for accurate and reliable testing methods to ensure the safe handling and storage of petroleum products. The market is driven by factors such as the growth of the petroleum industry, stringent safety regulations, and the increasing need for quality control in various industrial processes. As industries continue to prioritize safety and compliance, the market for petroleum flash point testers is expected to grow steadily. The demand for these testers is influenced by the need for accurate and reliable testing methods to prevent accidents and ensure the safe handling of petroleum products. The global market encompasses a range of products, including both open cup and closed cup flash point testers, each designed to meet specific testing requirements. The choice between open cup and closed cup testers depends on factors such as the type of material being tested, the required level of accuracy, and regulatory requirements. As the demand for reliable and accurate testing methods continues to grow, both open cup and closed cup flash point testers are expected to see increased adoption in various industries.

| Report Metric | Details |

| Report Name | Petroleum Flash Point Tester Market |

| Accounted market size in 2023 | US$ 41 million |

| Forecasted market size in 2030 | US$ 61 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Anton Paar, ERALYTICS, Grabner Instruments, Koehler, NORMALAB, Labtron, Tanaka, PAC, Seta, Elcometer, TIMEPOWER, Yangzhou JINGYANG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |