What is Global Food Aluminum Foil Packaging Market?

The Global Food Aluminum Foil Packaging Market refers to the industry that produces and sells aluminum foil packaging specifically designed for food products. Aluminum foil is a versatile material used for packaging due to its excellent barrier properties, which protect food from light, oxygen, moisture, and contaminants. This market encompasses a wide range of products, including wraps, pouches, containers, and lids, all made from aluminum foil. These products are used in various food sectors such as fast food, delicatessens, and other food service industries. The market is driven by the increasing demand for convenient, hygienic, and sustainable packaging solutions. Aluminum foil packaging is also favored for its recyclability, which aligns with the growing consumer preference for eco-friendly products. The market is global, with significant contributions from regions like North America, Europe, Asia-Pacific, and others. The continuous innovation in packaging technology and the rising awareness about food safety and preservation are key factors propelling the growth of this market.

Heavy Gauge Foil, Medium Gauge Foil, Light Gauge Foil, Other in the Global Food Aluminum Foil Packaging Market:

Heavy Gauge Foil, Medium Gauge Foil, Light Gauge Foil, and Other types of aluminum foil are integral components of the Global Food Aluminum Foil Packaging Market. Heavy Gauge Foil is typically used for applications requiring robust protection and durability. It is thicker and provides excellent barrier properties, making it ideal for packaging products that need long-term storage or are sensitive to environmental factors. This type of foil is often used in the packaging of meat, poultry, and other perishable items. Medium Gauge Foil strikes a balance between durability and flexibility. It is commonly used for packaging products that require moderate protection and are not as sensitive as those needing heavy gauge foil. This type of foil is often found in the packaging of baked goods, dairy products, and ready-to-eat meals. Light Gauge Foil is the thinnest and most flexible type of aluminum foil. It is widely used for packaging snacks, confectioneries, and other lightweight food items. Despite its thinness, it still offers good barrier properties and is easy to mold into various shapes and sizes, making it highly versatile. Other types of aluminum foil in the market include specialized foils designed for specific applications, such as embossed or coated foils that provide additional aesthetic or functional benefits. These specialized foils cater to niche markets and specific customer requirements. The choice of foil type depends on the specific needs of the food product being packaged, including factors like shelf life, sensitivity to environmental conditions, and the desired presentation. Each type of foil plays a crucial role in ensuring the safety, quality, and longevity of food products, thereby contributing to the overall growth and development of the Global Food Aluminum Foil Packaging Market.

Fast Food, Delicatessen, Other in the Global Food Aluminum Foil Packaging Market:

The usage of Global Food Aluminum Foil Packaging Market in areas such as Fast Food, Delicatessen, and Other food services is extensive and varied. In the fast food industry, aluminum foil packaging is essential for maintaining the freshness and temperature of food items. It is commonly used for wrapping burgers, sandwiches, and other hot foods to keep them warm and prevent them from becoming soggy. The foil's excellent barrier properties also help in retaining the flavors and aromas of the food, enhancing the overall customer experience. In delicatessens, aluminum foil packaging is used for a wide range of products, including cold cuts, cheeses, and prepared salads. The foil helps in preserving the freshness and quality of these items by protecting them from exposure to air and moisture. It also provides a convenient and hygienic way to package and transport these products, ensuring they reach the consumer in optimal condition. Other food services, such as catering and meal delivery, also rely heavily on aluminum foil packaging. It is used for packaging a variety of dishes, from appetizers to main courses and desserts. The foil's versatility allows it to be used for both hot and cold foods, making it a popular choice for caterers and meal delivery services. Additionally, aluminum foil containers are often used for baking and reheating food, providing a convenient and efficient solution for both food preparation and storage. The recyclability of aluminum foil also makes it an attractive option for food service providers looking to reduce their environmental impact. Overall, the usage of aluminum foil packaging in these areas highlights its importance in ensuring food safety, quality, and convenience, thereby driving the growth of the Global Food Aluminum Foil Packaging Market.

Global Food Aluminum Foil Packaging Market Outlook:

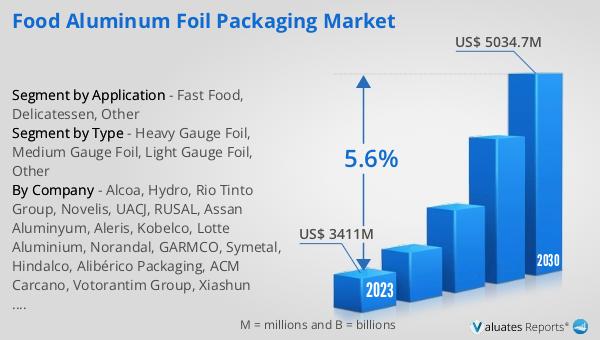

The global Food Aluminum Foil Packaging market was valued at US$ 3411 million in 2023 and is anticipated to reach US$ 5034.7 million by 2030, witnessing a CAGR of 5.6% during the forecast period from 2024 to 2030. The market is dominated by the top five global players, who collectively hold a share of about 40%. Among the various product segments, Light Gauge Foil stands out as the largest, accounting for approximately 50% of the market share. This significant share can be attributed to the versatility and wide range of applications of Light Gauge Foil in the food packaging industry. The market's growth is driven by the increasing demand for convenient, hygienic, and sustainable packaging solutions. The recyclability of aluminum foil also aligns with the growing consumer preference for eco-friendly products, further boosting the market's expansion. The continuous innovation in packaging technology and the rising awareness about food safety and preservation are key factors propelling the growth of this market.

| Report Metric | Details |

| Report Name | Food Aluminum Foil Packaging Market |

| Accounted market size in 2023 | US$ 3411 million |

| Forecasted market size in 2030 | US$ 5034.7 million |

| CAGR | 5.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Alcoa, Hydro, Rio Tinto Group, Novelis, UACJ, RUSAL, Assan Aluminyum, Aleris, Kobelco, Lotte Aluminium, Norandal, GARMCO, Symetal, Hindalco, Alibérico Packaging, ACM Carcano, Votorantim Group, Xiashun Holdings, SNTO, Shenhuo Aluminium Foil, LOFTEN, Nanshan Light Alloy, Zhenjiang Dingsheng Aluminum, CHINALCO, Kunshan Aluminium, Henan Zhongfu Industrial, Huaxi Aluminum |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |