What is Global E-Frac Market?

The Global E-Frac Market refers to the market for electric fracturing technology used in the oil and gas industry. This technology is an alternative to traditional hydraulic fracturing, which relies on diesel-powered pumps. E-Frac, or electric fracturing, uses electric pumps to inject high-pressure fluid into rock formations to release oil and gas. The shift towards electric fracturing is driven by the need for more environmentally friendly and efficient methods of extraction. Electric fracturing reduces emissions, noise, and operational costs compared to conventional methods. The market for E-Frac technology is growing as companies seek to adopt cleaner and more sustainable practices. This market encompasses various components, including electric pumping units, tech command centers, wireline units, and ancillary equipment. The adoption of E-Frac technology is expected to increase as the oil and gas industry continues to prioritize sustainability and efficiency.

Electric Pumping Unit, Tech Command Center (TCC), Wireline Unit, Ancillary Equipment, Others in the Global E-Frac Market:

An Electric Pumping Unit is a crucial component of the Global E-Frac Market. These units replace traditional diesel-powered pumps with electric motors, providing a more efficient and environmentally friendly solution for hydraulic fracturing. Electric pumps offer several advantages, including reduced emissions, lower noise levels, and improved operational efficiency. They are powered by electricity, which can be sourced from renewable energy, further enhancing their environmental benefits. The Tech Command Center (TCC) is another essential element in the E-Frac market. The TCC is a centralized control hub that monitors and manages the entire fracturing operation. It integrates data from various sensors and equipment, allowing operators to make real-time decisions and optimize the fracturing process. The TCC enhances safety, efficiency, and accuracy in E-Frac operations. The Wireline Unit is used to deploy and retrieve downhole tools and equipment during the fracturing process. It plays a vital role in ensuring the proper placement and operation of fracturing tools, contributing to the overall success of the E-Frac operation. Ancillary Equipment includes various supporting components such as power generators, transformers, and cooling systems. These components are essential for the smooth operation of electric fracturing units and ensure that the entire system functions efficiently. Other elements in the E-Frac market include software and automation technologies that enhance the precision and effectiveness of fracturing operations. These technologies enable operators to monitor and control the fracturing process remotely, reducing the need for on-site personnel and minimizing the risk of human error. The integration of advanced technologies in the E-Frac market is driving innovation and improving the overall performance of hydraulic fracturing operations.

Shale Oil, Conventional Oil in the Global E-Frac Market:

The Global E-Frac Market finds significant usage in the extraction of Shale Oil and Conventional Oil. Shale oil extraction involves the hydraulic fracturing of shale rock formations to release trapped oil and gas. E-Frac technology is particularly beneficial in shale oil extraction due to its efficiency and environmental advantages. Electric fracturing reduces emissions and noise, making it a more sustainable option for shale oil operations. The use of electric pumps in shale oil extraction also enhances operational efficiency by providing consistent and reliable power. This leads to more effective fracturing and higher recovery rates of oil and gas. In conventional oil extraction, E-Frac technology is used to enhance the productivity of existing wells. Conventional oil extraction typically involves drilling into reservoirs of liquid oil. By using electric fracturing, operators can increase the permeability of the rock formations, allowing for more oil to flow into the wellbore. This results in higher production rates and improved recovery of conventional oil. The environmental benefits of E-Frac technology are also significant in conventional oil extraction. Reduced emissions and noise levels contribute to a lower environmental impact, making E-Frac a more sustainable choice for conventional oil operations. Additionally, the use of electric fracturing in conventional oil extraction can lead to cost savings by reducing fuel consumption and maintenance requirements. The adoption of E-Frac technology in both shale oil and conventional oil extraction is driven by the need for more efficient and environmentally friendly methods of production. As the oil and gas industry continues to prioritize sustainability, the use of E-Frac technology is expected to grow, providing significant benefits in terms of efficiency, environmental impact, and cost savings.

Global E-Frac Market Outlook:

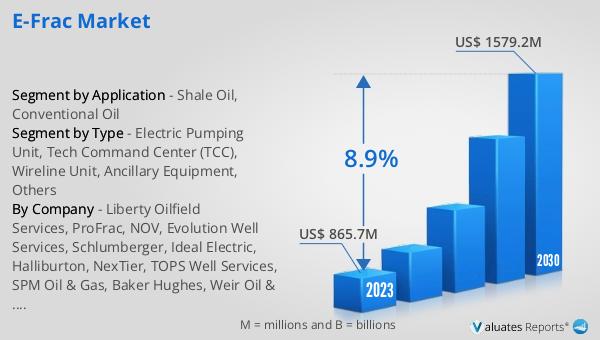

The global E-Frac market was valued at US$ 865.7 million in 2023 and is anticipated to reach US$ 1579.2 million by 2030, witnessing a CAGR of 8.9% during the forecast period 2024-2030. This growth reflects the increasing adoption of electric fracturing technology in the oil and gas industry. The shift towards more sustainable and efficient methods of extraction is driving the demand for E-Frac technology. Companies are investing in electric fracturing to reduce emissions, lower operational costs, and improve the overall efficiency of their operations. The market's growth is also supported by advancements in technology, such as the development of more efficient electric pumping units and the integration of advanced control systems like the Tech Command Center. These innovations are enhancing the performance and reliability of E-Frac operations, making them a more attractive option for oil and gas companies. The increasing focus on environmental sustainability and regulatory pressures to reduce emissions are also contributing to the growth of the E-Frac market. As the industry continues to evolve, the adoption of E-Frac technology is expected to increase, driving further growth in the market.

| Report Metric | Details |

| Report Name | E-Frac Market |

| Accounted market size in 2023 | US$ 865.7 million |

| Forecasted market size in 2030 | US$ 1579.2 million |

| CAGR | 8.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Liberty Oilfield Services, ProFrac, NOV, Evolution Well Services, Schlumberger, Ideal Electric, Halliburton, NexTier, TOPS Well Services, SPM Oil & Gas, Baker Hughes, Weir Oil & Gas, KCF Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |