What is Global HVAC Sensors & Controllers Market?

The Global HVAC Sensors & Controllers Market is a crucial segment within the broader HVAC (Heating, Ventilation, and Air Conditioning) industry. This market focuses on the development and distribution of sensors and controllers that are integral to the efficient functioning of HVAC systems. These components are essential for maintaining optimal indoor air quality and temperature, ensuring energy efficiency, and enhancing the overall comfort of residential, commercial, and industrial spaces. HVAC sensors are responsible for detecting changes in environmental conditions such as temperature, humidity, and air quality, while controllers process this data to adjust the HVAC system's operations accordingly. The market is driven by the increasing demand for energy-efficient solutions, advancements in sensor technology, and the growing awareness of the importance of indoor air quality. As buildings become smarter and more connected, the role of HVAC sensors and controllers becomes even more significant, contributing to the sustainability and efficiency of modern infrastructure. The market is characterized by continuous innovation, with manufacturers striving to develop more accurate, reliable, and cost-effective solutions to meet the evolving needs of consumers and businesses worldwide.

Sensors, Controllers in the Global HVAC Sensors & Controllers Market:

Sensors and controllers are the backbone of the Global HVAC Sensors & Controllers Market, playing a pivotal role in the functionality and efficiency of HVAC systems. Sensors are devices that detect and measure physical properties such as temperature, humidity, pressure, and air quality. They provide real-time data that is crucial for the HVAC system to operate effectively. For instance, temperature sensors monitor the ambient temperature and send this information to the controller, which then adjusts the heating or cooling output to maintain the desired temperature. Humidity sensors, on the other hand, measure the moisture level in the air, ensuring that the indoor environment remains comfortable and healthy. Pressure sensors are used to monitor the pressure levels within the HVAC system, preventing potential malfunctions or inefficiencies. Air quality sensors detect pollutants and other harmful substances in the air, prompting the system to increase ventilation or filtration as needed. Controllers, on the other hand, are the brains of the HVAC system. They receive data from the sensors and use this information to make decisions about how the system should operate. Controllers can be simple thermostats that regulate temperature or more complex systems that manage multiple aspects of the HVAC system, including ventilation, air quality, and energy consumption. Advanced controllers are equipped with algorithms that enable them to learn from past data and optimize system performance over time. They can also be integrated with building management systems, allowing for centralized control and monitoring of the HVAC system. This integration is particularly beneficial in large commercial or industrial settings, where maintaining optimal environmental conditions is critical for productivity and safety. The Global HVAC Sensors & Controllers Market is witnessing significant advancements in technology, driven by the increasing demand for smart and energy-efficient solutions. The development of wireless sensors and controllers has revolutionized the market, offering greater flexibility and ease of installation. These wireless devices can be easily integrated into existing systems, reducing the need for extensive wiring and minimizing installation costs. Additionally, the rise of the Internet of Things (IoT) has enabled the development of connected sensors and controllers that can communicate with other devices and systems, providing real-time data and insights for improved decision-making. Another key trend in the market is the growing emphasis on sustainability and energy efficiency. As governments and organizations worldwide strive to reduce their carbon footprint, the demand for energy-efficient HVAC systems is on the rise. Sensors and controllers play a crucial role in achieving this goal by optimizing system performance and reducing energy consumption. For example, occupancy sensors can detect when a room is empty and adjust the HVAC system accordingly, preventing unnecessary energy use. Similarly, advanced controllers can analyze data from multiple sensors to identify patterns and make adjustments that enhance system efficiency. In conclusion, sensors and controllers are essential components of the Global HVAC Sensors & Controllers Market, driving innovation and efficiency in the HVAC industry. As technology continues to evolve, these devices will play an increasingly important role in creating smarter, more sustainable buildings that meet the needs of modern consumers and businesses.

Commercial, Residential, Industrial, Transportation & Logistics in the Global HVAC Sensors & Controllers Market:

The usage of Global HVAC Sensors & Controllers Market spans across various sectors, including commercial, residential, industrial, and transportation & logistics, each with its unique requirements and challenges. In commercial settings, such as office buildings, shopping malls, and hospitals, HVAC sensors and controllers are vital for maintaining a comfortable and healthy indoor environment. These systems ensure that temperature, humidity, and air quality are kept within optimal ranges, enhancing the comfort and productivity of occupants. In large commercial buildings, advanced controllers can manage multiple zones, allowing for precise control of environmental conditions in different areas. This zoned approach not only improves comfort but also enhances energy efficiency by ensuring that heating and cooling are only provided where needed. In residential applications, HVAC sensors and controllers are becoming increasingly popular as homeowners seek to improve comfort and reduce energy costs. Smart thermostats, which are a type of controller, allow homeowners to set and adjust temperature settings remotely via smartphone apps. These devices can learn from user behavior and preferences, automatically adjusting settings to optimize comfort and energy use. Additionally, sensors can detect changes in temperature and humidity, ensuring that the HVAC system responds promptly to maintain a comfortable indoor environment. The integration of sensors and controllers with home automation systems further enhances convenience, allowing homeowners to manage their HVAC systems alongside other smart home devices. The industrial sector also benefits significantly from the use of HVAC sensors and controllers. In manufacturing facilities, warehouses, and other industrial settings, maintaining precise environmental conditions is crucial for product quality and worker safety. Sensors monitor temperature, humidity, and air quality, ensuring that conditions remain within specified limits. Controllers use this data to adjust the HVAC system, preventing fluctuations that could impact production processes or compromise safety. In addition to maintaining optimal conditions, sensors and controllers help industrial facilities reduce energy consumption and operational costs by optimizing system performance and identifying areas for improvement. In the transportation and logistics sector, HVAC sensors and controllers are essential for maintaining the quality and safety of goods during transit. In refrigerated trucks and containers, temperature and humidity sensors ensure that perishable goods are kept within the required conditions, preventing spoilage and ensuring compliance with regulatory standards. Controllers use this data to adjust the HVAC system, maintaining consistent conditions throughout the journey. Additionally, sensors can detect changes in air quality, alerting operators to potential issues that could impact the safety or quality of goods. The integration of sensors and controllers with telematics systems allows for real-time monitoring and control, providing operators with valuable insights into system performance and enabling proactive maintenance. Overall, the Global HVAC Sensors & Controllers Market plays a critical role in enhancing comfort, efficiency, and safety across various sectors. As technology continues to advance, the capabilities of sensors and controllers will expand, offering even greater benefits to consumers and businesses worldwide.

Global HVAC Sensors & Controllers Market Outlook:

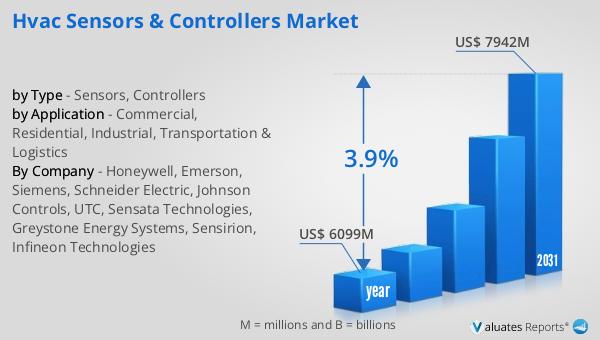

The global market for HVAC Sensors & Controllers was valued at approximately $6,099 million in 2024. This market is anticipated to grow steadily, reaching an estimated size of $7,942 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.9% over the forecast period. The steady increase in market size reflects the rising demand for energy-efficient and smart HVAC solutions across various sectors. As more buildings and facilities prioritize sustainability and energy efficiency, the adoption of advanced sensors and controllers is expected to rise. These devices play a crucial role in optimizing HVAC system performance, reducing energy consumption, and enhancing indoor comfort and air quality. The market's growth is also driven by technological advancements, such as the development of wireless and IoT-enabled sensors and controllers, which offer greater flexibility and integration capabilities. As the market continues to evolve, manufacturers are focusing on innovation and product development to meet the changing needs of consumers and businesses. This includes the creation of more accurate, reliable, and cost-effective solutions that can be easily integrated into existing systems. Overall, the Global HVAC Sensors & Controllers Market is poised for steady growth, driven by the increasing demand for smart and sustainable building solutions.

| Report Metric | Details |

| Report Name | HVAC Sensors & Controllers Market |

| Accounted market size in year | US$ 6099 million |

| Forecasted market size in 2031 | US$ 7942 million |

| CAGR | 3.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Honeywell, Emerson, Siemens, Schneider Electric, Johnson Controls, UTC, Sensata Technologies, Greystone Energy Systems, Sensirion, Infineon Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |