What is Global Human Coagulation Factor VII Market?

The Global Human Coagulation Factor VII Market is a specialized segment within the pharmaceutical industry, focusing on the production and distribution of Factor VII, a crucial protein in the blood coagulation process. This market is driven by the demand for effective treatments for bleeding disorders, particularly hemophilia. Factor VII is essential for initiating the clotting cascade, which is vital for preventing excessive bleeding in individuals with clotting deficiencies. The market encompasses both recombinant and plasma-derived forms of Factor VII, catering to different patient needs and preferences. Advances in biotechnology have enabled the development of recombinant Factor VII, which offers a safer and more consistent alternative to plasma-derived products. The market is characterized by a few key players who dominate the landscape, leveraging their expertise in biotechnology and pharmaceuticals to innovate and expand their product offerings. As awareness of bleeding disorders increases and diagnostic capabilities improve, the demand for Factor VII products is expected to grow, driving further research and development in this field. The market's growth is also supported by the increasing prevalence of hemophilia and other bleeding disorders, as well as the expansion of healthcare infrastructure in emerging economies.

Prefilled Syringe, Vial in the Global Human Coagulation Factor VII Market:

Prefilled syringes and vials are two primary forms of packaging and delivery systems used in the Global Human Coagulation Factor VII Market. Prefilled syringes offer several advantages, including ease of use, reduced risk of contamination, and precise dosing, making them a preferred choice for both healthcare providers and patients. These syringes are designed for single-use, ensuring sterility and minimizing the risk of infection. The convenience of prefilled syringes is particularly beneficial in emergency situations where rapid administration of Factor VII is critical. Additionally, they reduce the preparation time required for healthcare professionals, allowing for more efficient patient care. On the other hand, vials are a more traditional form of packaging, offering flexibility in dosing and the ability to store larger quantities of the product. Vials are often used in hospital settings where multiple doses may be required, and healthcare professionals have the expertise to handle and prepare the medication. The choice between prefilled syringes and vials depends on various factors, including the setting in which the product is used, the patient's condition, and the healthcare provider's preference. Both forms play a crucial role in ensuring the availability and accessibility of Factor VII products to patients in need. The development of these delivery systems is driven by the need for safe, effective, and user-friendly options that enhance patient compliance and improve treatment outcomes. As the market continues to evolve, manufacturers are investing in research and development to improve the design and functionality of prefilled syringes and vials, ensuring they meet the highest standards of quality and safety. Innovations in materials and manufacturing processes are also contributing to the advancement of these delivery systems, making them more reliable and efficient. The growing demand for prefilled syringes and vials is also influenced by the increasing prevalence of bleeding disorders and the need for effective treatment options. As awareness of these conditions rises, more patients are seeking treatment, driving the demand for convenient and accessible delivery systems. The market for prefilled syringes and vials is expected to expand as healthcare providers and patients recognize the benefits of these delivery systems in managing bleeding disorders. The focus on patient-centric care is also encouraging manufacturers to develop products that are easy to use and enhance the overall treatment experience. In conclusion, prefilled syringes and vials are integral components of the Global Human Coagulation Factor VII Market, providing essential delivery systems that ensure the safe and effective administration of Factor VII products. Their continued development and innovation are crucial for meeting the growing demand for bleeding disorder treatments and improving patient outcomes.

Congenital Hemophilia, Acquired Hemophilia, Other in the Global Human Coagulation Factor VII Market:

The Global Human Coagulation Factor VII Market plays a vital role in the treatment of various bleeding disorders, including congenital hemophilia, acquired hemophilia, and other related conditions. Congenital hemophilia is a genetic disorder characterized by a deficiency in clotting factors, leading to excessive bleeding. Factor VII is used as a replacement therapy to help initiate the clotting process and prevent bleeding episodes in individuals with this condition. The availability of recombinant Factor VII has significantly improved the management of congenital hemophilia, offering a safer and more effective treatment option compared to plasma-derived products. Patients with congenital hemophilia often require regular infusions of Factor VII to maintain adequate clotting levels and prevent spontaneous bleeding. Acquired hemophilia, on the other hand, is a rare autoimmune disorder where the body's immune system mistakenly attacks its own clotting factors, leading to severe bleeding. Factor VII is used as a bypassing agent in the treatment of acquired hemophilia, helping to control bleeding episodes by activating the clotting cascade. The use of Factor VII in acquired hemophilia has been shown to be effective in managing bleeding episodes and improving patient outcomes. In addition to congenital and acquired hemophilia, Factor VII is also used in the treatment of other bleeding disorders, such as Glanzmann's thrombasthenia and factor VII deficiency. These conditions are characterized by a lack of specific clotting factors, leading to an increased risk of bleeding. Factor VII is used as a replacement therapy to help restore normal clotting function and prevent bleeding episodes. The use of Factor VII in these conditions has been shown to be effective in reducing the frequency and severity of bleeding episodes, improving the quality of life for patients. The Global Human Coagulation Factor VII Market is driven by the increasing prevalence of bleeding disorders and the growing demand for effective treatment options. Advances in biotechnology have enabled the development of recombinant Factor VII, offering a safer and more consistent alternative to plasma-derived products. The market is characterized by a few key players who dominate the landscape, leveraging their expertise in biotechnology and pharmaceuticals to innovate and expand their product offerings. As awareness of bleeding disorders increases and diagnostic capabilities improve, the demand for Factor VII products is expected to grow, driving further research and development in this field. The market's growth is also supported by the expansion of healthcare infrastructure in emerging economies, providing greater access to treatment for patients with bleeding disorders. In conclusion, the Global Human Coagulation Factor VII Market is essential for the treatment of various bleeding disorders, offering effective solutions for patients with congenital hemophilia, acquired hemophilia, and other related conditions. The continued development and innovation in this market are crucial for meeting the growing demand for bleeding disorder treatments and improving patient outcomes.

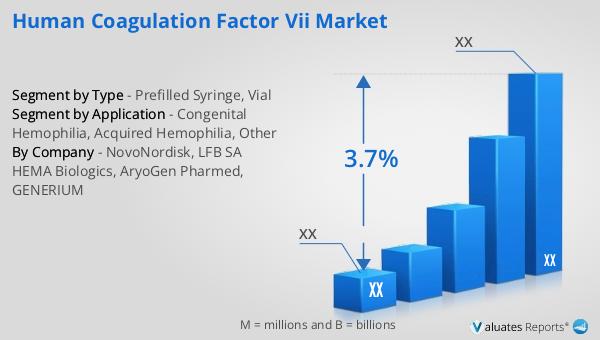

Global Human Coagulation Factor VII Market Outlook:

In 2024, the global market size for Human Coagulation Factor VII was valued at approximately US$ 1,251 million, with projections indicating it could reach around US$ 1,608 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2025 to 2031. The market is predominantly controlled by three major manufacturers of recombinant human coagulation VIIa: Novo Nordisk, LFB SA, HEMA Biologics, and GENERIUM, which collectively hold a market share exceeding 99%. North America stands out as the most significant consumer market for recombinant human coagulation VIIa, accounting for about 45% of the global market share. This dominance is attributed to the region's advanced healthcare infrastructure, high awareness of bleeding disorders, and strong presence of key market players. The market's growth is driven by the increasing prevalence of bleeding disorders, advancements in biotechnology, and the expansion of healthcare infrastructure in emerging economies. As awareness of bleeding disorders rises and diagnostic capabilities improve, the demand for Factor VII products is expected to grow, driving further research and development in this field. The market's growth is also supported by the expansion of healthcare infrastructure in emerging economies, providing greater access to treatment for patients with bleeding disorders. In conclusion, the Global Human Coagulation Factor VII Market is essential for the treatment of various bleeding disorders, offering effective solutions for patients with congenital hemophilia, acquired hemophilia, and other related conditions. The continued development and innovation in this market are crucial for meeting the growing demand for bleeding disorder treatments and improving patient outcomes.

| Report Metric | Details |

| Report Name | Human Coagulation Factor VII Market |

| CAGR | 3.7% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | NovoNordisk, LFB SA HEMA Biologics, AryoGen Pharmed, GENERIUM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |