What is Global Botox Market?

The Global Botox Market refers to the worldwide industry centered around the production, distribution, and application of botulinum toxin, commonly known as Botox. This market encompasses a wide range of products and services related to Botox, which is primarily used for both medical and cosmetic purposes. Botox is a neurotoxic protein produced by the bacterium Clostridium botulinum, and it is used in small, controlled doses to temporarily paralyze muscles. This property makes it highly effective in treating various medical conditions such as chronic migraines, muscle stiffness, and excessive sweating, as well as in cosmetic procedures to reduce the appearance of wrinkles and fine lines. The market is driven by increasing demand for minimally invasive procedures, rising awareness about aesthetic treatments, and advancements in medical technology. Key players in the market include major pharmaceutical companies that manufacture and distribute Botox products globally. The market is characterized by intense competition, ongoing research and development, and regulatory considerations that impact the approval and use of Botox products in different regions. As the demand for both medical and cosmetic applications of Botox continues to grow, the market is expected to expand, offering new opportunities for innovation and growth.

50U, 100U, Others in the Global Botox Market:

In the Global Botox Market, products are often categorized based on their unit measurements, such as 50U, 100U, and others. These units refer to the dosage strength of the botulinum toxin in each vial, which is crucial for determining the appropriate amount needed for various treatments. The 50U and 100U vials are among the most commonly used in both medical and cosmetic applications. The 50U vial is typically used for smaller treatment areas or for patients who require a lower dosage. This can include cosmetic procedures such as treating fine lines around the eyes or forehead, where a smaller amount of Botox is sufficient to achieve the desired effect. In medical applications, a 50U vial might be used for conditions that require less intensive muscle relaxation, such as mild cases of muscle stiffness or minor instances of excessive sweating. On the other hand, the 100U vial is often used for larger treatment areas or for conditions that require a higher dosage of Botox. In cosmetic applications, this might include more extensive treatments for deeper wrinkles or larger areas of the face. In medical contexts, a 100U vial could be used for more severe cases of chronic migraines, where a higher dosage is necessary to achieve effective relief. Additionally, the 100U vial is commonly used in treating conditions like cervical dystonia, where significant muscle relaxation is required to alleviate symptoms. Beyond the standard 50U and 100U vials, the "others" category includes various formulations and dosages that cater to specific needs or preferences. This can include customized dosages for unique medical conditions or specialized cosmetic treatments. Some manufacturers offer vials with different concentrations or formulations designed to enhance the stability or efficacy of the Botox product. These variations allow healthcare providers to tailor treatments to individual patient needs, ensuring optimal results. The choice between 50U, 100U, and other dosages depends on several factors, including the specific condition being treated, the patient's medical history, and the desired outcome. Healthcare providers must carefully assess each patient's needs to determine the most appropriate dosage and formulation. This requires a thorough understanding of the pharmacology of Botox, as well as experience in administering the product safely and effectively. The availability of different dosages and formulations in the Global Botox Market reflects the diverse range of applications and the growing demand for personalized treatment options. As the market continues to evolve, manufacturers are likely to develop new products and formulations that further enhance the versatility and effectiveness of Botox treatments. This ongoing innovation is driven by advances in medical research, as well as feedback from healthcare providers and patients who seek improved outcomes and experiences. In summary, the categorization of Botox products into 50U, 100U, and others highlights the importance of dosage in achieving successful treatment outcomes. Whether used for medical or cosmetic purposes, the appropriate dosage and formulation are critical to ensuring patient safety and satisfaction. As the Global Botox Market continues to grow, the availability of diverse product options will play a key role in meeting the needs of a wide range of patients and healthcare providers.

Medical, Cosmetic in the Global Botox Market:

The Global Botox Market is widely recognized for its applications in both medical and cosmetic fields, each offering distinct benefits and addressing different needs. In the medical realm, Botox is utilized for its muscle-relaxing properties, which can provide relief for a variety of conditions. One of the most common medical uses of Botox is in the treatment of chronic migraines. By injecting Botox into specific areas of the head and neck, healthcare providers can help reduce the frequency and severity of migraine attacks, offering significant relief to patients who suffer from this debilitating condition. Additionally, Botox is used to treat muscle stiffness and spasms, particularly in conditions like cervical dystonia, where involuntary muscle contractions cause discomfort and pain. By relaxing the affected muscles, Botox can improve mobility and quality of life for patients. Another medical application of Botox is in the treatment of hyperhidrosis, or excessive sweating. By injecting Botox into the sweat glands, it can effectively reduce sweating in targeted areas, such as the underarms, hands, or feet, providing relief for individuals who struggle with this condition. In the cosmetic field, Botox is primarily used to reduce the appearance of wrinkles and fine lines, offering a non-surgical solution for individuals seeking to enhance their appearance. The most common cosmetic application of Botox is in the treatment of dynamic wrinkles, which are caused by repeated facial expressions such as frowning or squinting. By temporarily paralyzing the underlying muscles, Botox can smooth out these wrinkles, resulting in a more youthful and refreshed appearance. Popular treatment areas include the forehead, crow's feet around the eyes, and frown lines between the eyebrows. The effects of Botox in cosmetic applications are typically temporary, lasting several months before the treatment needs to be repeated. This allows individuals to maintain their desired appearance with regular maintenance treatments. The popularity of Botox in cosmetic applications is driven by its minimally invasive nature, quick procedure time, and relatively low risk of side effects. As a result, it has become a popular choice for individuals seeking to enhance their appearance without undergoing surgery. The dual usage of Botox in both medical and cosmetic fields highlights its versatility and effectiveness as a treatment option. In both contexts, the success of Botox treatments depends on the skill and expertise of the healthcare provider administering the injections. Proper training and experience are essential to ensure that the injections are performed safely and effectively, minimizing the risk of complications and achieving the desired results. As the Global Botox Market continues to grow, ongoing research and development efforts are likely to expand the range of applications for Botox, offering new opportunities for innovation and improved patient outcomes.

Global Botox Market Outlook:

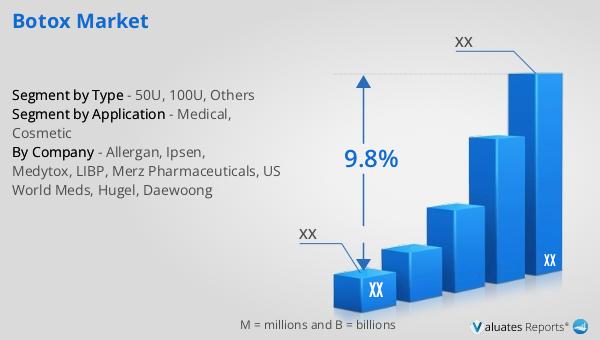

In 2024, the global market size for Botox was valued at approximately $5,658 million, with projections indicating a significant increase to around $10,790 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 9.8% during the forecast period from 2025 to 2031. The market is dominated by key manufacturers such as Allergan, Ipsen, Medytox, LIBP, and Merz Pharmaceuticals, which collectively hold an impressive 87% share of the market. North America stands out as the largest regional market for Botox, accounting for about 63% of the total market share. This dominance is largely attributed to the high demand for cosmetic procedures in the region, as well as the presence of major industry players. The most prevalent application of Botox is in the cosmetic sector, which constitutes over 50% of the market share. This highlights the significant role that aesthetic treatments play in driving the demand for Botox products. As the market continues to expand, the influence of these key manufacturers and the growing popularity of cosmetic applications are expected to shape the future landscape of the Global Botox Market.

| Report Metric | Details |

| Report Name | Botox Market |

| CAGR | 9.8% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Allergan, Ipsen, Medytox, LIBP, Merz Pharmaceuticals, US World Meds, Hugel, Daewoong |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |