What is Global WiFi Modules Market?

The Global WiFi Modules Market is a rapidly evolving sector that plays a crucial role in the connectivity landscape of today's digital world. WiFi modules are essential components that enable wireless communication between devices and networks, facilitating seamless data exchange and internet access. These modules are integrated into a wide range of products, from consumer electronics to industrial machinery, allowing them to connect to the internet and communicate with other devices. The market for WiFi modules is driven by the increasing demand for smart devices and the Internet of Things (IoT), which require reliable and efficient wireless connectivity solutions. As more industries and consumers adopt smart technologies, the need for advanced WiFi modules continues to grow, leading to innovations in module design, performance, and functionality. The global market is characterized by a diverse range of products, including embedded and external WiFi modules, each catering to specific application needs. With the ongoing advancements in wireless technology and the proliferation of connected devices, the Global WiFi Modules Market is poised for significant growth, offering numerous opportunities for manufacturers, developers, and end-users alike.

Embedded Wi-Fi Modules, External Wi-Fi Modules in the Global WiFi Modules Market:

Embedded Wi-Fi Modules and External Wi-Fi Modules are two primary categories within the Global WiFi Modules Market, each serving distinct purposes and applications. Embedded Wi-Fi Modules are integrated directly into devices, providing seamless wireless connectivity without the need for additional hardware. These modules are typically used in applications where space is limited, and a compact, efficient solution is required. They are commonly found in consumer electronics, such as smartphones, tablets, and smart home devices, where they enable features like remote control, data synchronization, and internet access. Embedded modules are designed to be energy-efficient, ensuring that devices can maintain connectivity without draining battery life excessively. On the other hand, External Wi-Fi Modules are standalone devices that connect to a host system via interfaces like USB, Ethernet, or serial ports. These modules are ideal for applications where flexibility and ease of installation are priorities. They are often used in industrial settings, where equipment may need to be retrofitted with wireless capabilities without altering the existing hardware. External modules offer the advantage of being easily replaceable or upgradeable, allowing users to adapt to changing technology standards or performance requirements. Both embedded and external Wi-Fi modules are crucial in enabling the connectivity of devices across various sectors, from consumer electronics to industrial automation. As the demand for wireless connectivity continues to rise, manufacturers are focusing on developing modules that offer enhanced performance, security, and compatibility with emerging technologies. This includes support for the latest Wi-Fi standards, such as Wi-Fi 6 and Wi-Fi 6E, which provide faster speeds, lower latency, and improved network efficiency. Additionally, there is a growing emphasis on security features, as connected devices become increasingly vulnerable to cyber threats. Manufacturers are incorporating advanced encryption and authentication protocols to ensure that data transmitted over Wi-Fi networks remains secure. The choice between embedded and external Wi-Fi modules often depends on the specific requirements of the application, including factors like size constraints, power consumption, and the need for flexibility. In consumer electronics, embedded modules are favored for their compactness and integration capabilities, while external modules are preferred in industrial and commercial applications where adaptability and ease of maintenance are critical. As the Global WiFi Modules Market continues to expand, both embedded and external modules will play vital roles in shaping the future of wireless connectivity, driving innovation and enabling new possibilities across a wide range of industries.

Smart Home and Consumer Electronics, Industrial Internet of Things, Automobile and Internet of Vehicles, Medical and Health Equipment, Retail and Commercial Equipment, Smart Cities and Public Facilities, Aerospace and Defense, Energy and Power Monitoring, Others in the Global WiFi Modules Market:

The Global WiFi Modules Market finds extensive usage across various sectors, each leveraging the technology to enhance connectivity and functionality. In the realm of Smart Home and Consumer Electronics, WiFi modules are integral to the operation of devices like smart thermostats, security cameras, and voice-activated assistants. These modules enable seamless communication between devices and users, allowing for remote control and automation of home environments. In the Industrial Internet of Things (IIoT), WiFi modules facilitate the connection of machinery and sensors to centralized systems, enabling real-time monitoring, data analysis, and process optimization. This connectivity is crucial for improving operational efficiency and reducing downtime in manufacturing and production environments. In the Automobile and Internet of Vehicles sector, WiFi modules are used to provide in-car connectivity, supporting features like navigation, entertainment, and vehicle diagnostics. They enable vehicles to communicate with each other and with infrastructure, paving the way for advancements in autonomous driving and smart transportation systems. In the Medical and Health Equipment industry, WiFi modules are employed to connect medical devices and equipment, allowing for remote monitoring of patient health and the transmission of critical data to healthcare providers. This connectivity enhances patient care and enables timely interventions. In Retail and Commercial Equipment, WiFi modules support point-of-sale systems, inventory management, and customer engagement tools, streamlining operations and improving the customer experience. Smart Cities and Public Facilities utilize WiFi modules to connect infrastructure like streetlights, traffic signals, and public transportation systems, enabling efficient management and data-driven decision-making. In Aerospace and Defense, WiFi modules are used to enhance communication and data exchange between aircraft, ground control, and other systems, improving situational awareness and operational efficiency. In the Energy and Power Monitoring sector, WiFi modules enable the remote monitoring and management of energy consumption, supporting efforts to optimize energy use and reduce costs. Across these diverse applications, WiFi modules play a critical role in enabling connectivity and driving innovation, underscoring their importance in the modern digital landscape.

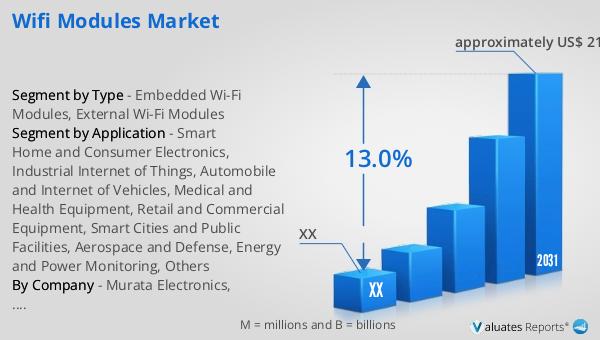

Global WiFi Modules Market Outlook:

In 2024, the global market for WiFi Modules was valued at approximately $9,319 million. Looking ahead, it is projected to grow significantly, reaching an estimated value of around $21,670 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 13.0% during the forecast period from 2025 to 2031. This substantial increase in market size reflects the rising demand for wireless connectivity solutions across various industries and applications. As more devices and systems become interconnected, the need for reliable and efficient WiFi modules continues to expand. The market's growth is driven by factors such as the proliferation of smart devices, the Internet of Things (IoT), and advancements in wireless technology. Manufacturers and developers are focusing on creating innovative WiFi modules that offer enhanced performance, security, and compatibility with emerging standards. This dynamic market environment presents numerous opportunities for stakeholders, from technology providers to end-users, as they seek to capitalize on the growing demand for wireless connectivity solutions. The projected growth of the Global WiFi Modules Market underscores its critical role in shaping the future of connectivity and enabling new possibilities across a wide range of sectors.

| Report Metric | Details |

| Report Name | WiFi Modules Market |

| Forecasted market size in 2031 | approximately US$ 21670 million |

| CAGR | 13.0% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Murata Electronics, USI, AzureWave, Advantech, Microchip Technology, Espressif, Silex Technogy, Silicon Laboratories, Digi International, Texas Instruments, Wurth Elektronik, Qualcomm, Fibocom, Quectel, Phoenix Contact, Doodle Labs, Broadcom Limited, Intel, Panasonic, Particle, Ai-thinker, Renesas Electronics, Maxchip, AmpedRF, Ebyte, Wi2Wi, AMPAK Tech, CEL (California Eastern Laboratories), Inventek Systems, I&C Technology, Feasycom, Jorjin, Ezurio, Sierra Wireless, Telit, Wiznet, Wireless-tag, Pycom, SIMCom Wireless Solutions, Sparklan, Rayson, RFCarzy |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |