What is Global BPADA Market?

The Global BPADA Market, or Bisphenol A Diglycidyl Ether (BPADA) market, is a specialized segment within the chemical industry that focuses on the production and distribution of BPADA, a key chemical compound used in various industrial applications. BPADA is primarily utilized in the manufacturing of high-performance polymers, particularly polyetherimides, which are known for their exceptional thermal stability, mechanical strength, and chemical resistance. These properties make BPADA an essential component in industries such as automotive, aerospace, electronics, and telecommunications, where materials are required to withstand extreme conditions. The market for BPADA is driven by the increasing demand for advanced materials that can meet the rigorous standards of modern technology and industrial applications. As industries continue to innovate and develop new products, the need for reliable and high-quality BPADA is expected to grow, making it a critical area of focus for chemical manufacturers and suppliers worldwide. The market is characterized by a competitive landscape with several key players striving to enhance their production capabilities and expand their market presence through strategic partnerships and technological advancements.

Below 99.0%, Above 99.0% in the Global BPADA Market:

In the Global BPADA Market, the purity levels of BPADA are categorized into two main segments: Below 99.0% and Above 99.0%. These purity levels are crucial as they determine the quality and performance of the end products in which BPADA is used. BPADA with a purity level Below 99.0% is typically used in applications where ultra-high purity is not a critical requirement. This category is often more cost-effective and is suitable for general industrial applications where the performance demands are moderate. Industries that utilize BPADA with Below 99.0% purity include those involved in the production of coatings, adhesives, and certain types of plastics where the material properties do not need to meet the highest standards of thermal and chemical resistance. On the other hand, BPADA with a purity level Above 99.0% is essential for high-performance applications where superior material properties are required. This includes the production of polyetherimides, which are used in demanding environments such as aerospace and automotive industries. The higher purity ensures that the polymers exhibit excellent thermal stability, mechanical strength, and resistance to harsh chemicals, making them ideal for use in components that are exposed to extreme conditions. The demand for BPADA with Above 99.0% purity is driven by the need for advanced materials that can meet the stringent requirements of modern technology and industrial applications. As industries continue to push the boundaries of innovation, the importance of high-purity BPADA is expected to increase, leading to a growing market segment focused on the production and supply of this critical chemical compound. Manufacturers in the BPADA market are continuously investing in research and development to improve the purity levels of their products and meet the evolving needs of their customers. This involves the adoption of advanced purification technologies and processes that can enhance the quality and performance of BPADA. Additionally, regulatory standards and environmental considerations play a significant role in shaping the market dynamics for BPADA. Companies are required to comply with stringent regulations regarding the production and use of chemical compounds, which necessitates continuous monitoring and improvement of their manufacturing processes. The competitive landscape of the BPADA market is characterized by the presence of several key players who are actively engaged in expanding their production capacities and enhancing their product offerings. These companies are focused on developing strategic partnerships and collaborations to strengthen their market position and gain a competitive edge. The market is also witnessing an increasing trend towards sustainability, with manufacturers exploring eco-friendly alternatives and processes to reduce the environmental impact of BPADA production. This includes the development of bio-based BPADA and the implementation of green chemistry principles in the manufacturing process. As the demand for high-performance materials continues to rise, the Global BPADA Market is poised for significant growth, driven by the increasing need for advanced polymers and the ongoing advancements in purification technologies.

Polyetherimide, Others in the Global BPADA Market:

The Global BPADA Market plays a crucial role in the production of polyetherimides, which are high-performance polymers known for their exceptional thermal stability, mechanical strength, and chemical resistance. Polyetherimides are widely used in industries such as aerospace, automotive, electronics, and telecommunications, where materials are required to withstand extreme conditions. The unique properties of polyetherimides make them ideal for use in components that are exposed to high temperatures, harsh chemicals, and mechanical stress. In the aerospace industry, polyetherimides are used in the production of aircraft components, such as interior panels, ducting systems, and electrical connectors, where their lightweight and durable nature contribute to improved fuel efficiency and performance. In the automotive industry, polyetherimides are used in the manufacturing of under-the-hood components, such as engine covers, intake manifolds, and electrical connectors, where their ability to withstand high temperatures and harsh chemicals is critical. In the electronics industry, polyetherimides are used in the production of connectors, sockets, and other components that require high thermal and electrical insulation properties. The demand for polyetherimides is driven by the increasing need for advanced materials that can meet the stringent requirements of modern technology and industrial applications. As industries continue to innovate and develop new products, the need for reliable and high-quality polyetherimides is expected to grow, making it a critical area of focus for chemical manufacturers and suppliers worldwide. In addition to polyetherimides, BPADA is also used in the production of other high-performance polymers and materials. These include epoxy resins, which are used in the production of coatings, adhesives, and composites, where their excellent mechanical properties and chemical resistance are highly valued. BPADA-based epoxy resins are used in a wide range of applications, including the construction, automotive, and electronics industries, where they provide enhanced durability and performance. The versatility of BPADA makes it a valuable component in the development of advanced materials that can meet the diverse needs of various industries. As the demand for high-performance materials continues to rise, the Global BPADA Market is poised for significant growth, driven by the increasing need for advanced polymers and the ongoing advancements in material science and technology.

Global BPADA Market Outlook:

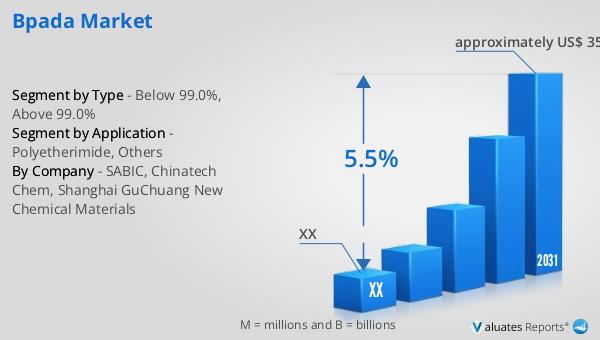

In 2024, the global market size of BPADA was valued at approximately US$ 244 million. This figure highlights the significant role BPADA plays in various industrial applications, particularly in the production of high-performance polymers like polyetherimides. The market is projected to experience substantial growth over the coming years, with forecasts indicating that it will reach around US$ 353 million by 2031. This anticipated growth is driven by a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2025 to 2031. The steady increase in market size underscores the growing demand for BPADA, fueled by its critical applications in industries such as aerospace, automotive, electronics, and telecommunications. As these industries continue to evolve and innovate, the need for advanced materials that can withstand extreme conditions and meet stringent performance standards is expected to rise. This, in turn, will drive the demand for BPADA, making it a key area of focus for chemical manufacturers and suppliers worldwide. The projected growth of the BPADA market also reflects the ongoing advancements in purification technologies and the increasing trend towards sustainability, as manufacturers strive to develop eco-friendly alternatives and processes to reduce the environmental impact of BPADA production. As the market continues to expand, companies are likely to invest in research and development to enhance their production capabilities and meet the evolving needs of their customers. The competitive landscape of the BPADA market is characterized by the presence of several key players who are actively engaged in expanding their market presence through strategic partnerships and collaborations. These efforts are aimed at strengthening their position in the market and gaining a competitive edge in the rapidly growing BPADA industry.

| Report Metric | Details |

| Report Name | BPADA Market |

| Forecasted market size in 2031 | approximately US$ 353 million |

| CAGR | 5.5% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | SABIC, Chinatech Chem, Shanghai GuChuang New Chemical Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |