What is Global B2B Middleware Market?

The Global B2B Middleware Market is a crucial component in the realm of business-to-business interactions, serving as a bridge that facilitates seamless communication and data exchange between different software applications within and across organizations. Middleware acts as an intermediary layer that connects disparate systems, enabling them to work together efficiently without requiring direct communication. This technology is essential for businesses that rely on complex IT environments, as it simplifies integration processes, enhances interoperability, and improves overall operational efficiency. By providing a unified platform for data exchange, middleware solutions help organizations streamline their workflows, reduce redundancies, and ensure that critical business processes are executed smoothly. As businesses continue to adopt digital transformation strategies, the demand for robust middleware solutions is expected to grow, making the Global B2B Middleware Market a vital area of focus for companies looking to optimize their IT infrastructure and maintain a competitive edge in the market.

Small and Medium Enterprises (SMEs), Large Enterprises, Others in the Global B2B Middleware Market:

Small and Medium Enterprises (SMEs) play a significant role in the Global B2B Middleware Market, as these businesses often face unique challenges when it comes to integrating various software applications and systems. SMEs typically operate with limited resources and may not have the extensive IT infrastructure that larger enterprises possess. As a result, middleware solutions become essential for these businesses to streamline their operations and improve efficiency. By leveraging middleware, SMEs can connect their existing applications, automate workflows, and ensure seamless data exchange between different systems. This not only helps in reducing operational costs but also enhances productivity by minimizing manual interventions and errors. Middleware solutions also provide SMEs with the flexibility to scale their operations as they grow, allowing them to add new applications and systems without disrupting existing processes. For large enterprises, the Global B2B Middleware Market offers a different set of advantages. These organizations often have complex IT environments with numerous applications and systems that need to work together seamlessly. Middleware solutions provide the necessary infrastructure to integrate these disparate systems, enabling large enterprises to achieve greater operational efficiency and agility. By facilitating real-time data exchange and communication between different applications, middleware helps large enterprises make informed decisions quickly and respond to market changes effectively. Additionally, middleware solutions support the implementation of advanced technologies such as cloud computing, big data analytics, and the Internet of Things (IoT), which are crucial for large enterprises looking to stay competitive in today's digital landscape. In the context of the Global B2B Middleware Market, "Others" refers to organizations that do not fall into the traditional categories of SMEs or large enterprises. This can include non-profit organizations, government agencies, and educational institutions, among others. These entities also benefit from middleware solutions, as they often require efficient data exchange and integration capabilities to support their operations. For instance, government agencies may use middleware to connect various departmental systems, ensuring that information is shared accurately and securely across different branches. Educational institutions can leverage middleware to integrate their administrative systems with learning management platforms, providing a seamless experience for students and staff. Overall, the Global B2B Middleware Market caters to a diverse range of organizations, each with its own unique set of requirements and challenges. By offering flexible and scalable solutions, middleware providers enable these organizations to optimize their IT infrastructure, improve operational efficiency, and achieve their strategic objectives.

BFSI, Medical, Education, Telecommunications, Travel, Manufacturing, Aerospace and Defence, Energy and Utilities, Others in the Global B2B Middleware Market:

The Global B2B Middleware Market finds extensive usage across various industries, each leveraging the technology to address specific challenges and enhance operational efficiency. In the Banking, Financial Services, and Insurance (BFSI) sector, middleware solutions are crucial for integrating disparate systems and ensuring seamless data exchange between different financial applications. This enables financial institutions to provide better customer service, streamline operations, and comply with regulatory requirements. Middleware also supports the implementation of advanced technologies such as blockchain and artificial intelligence, which are increasingly being adopted in the BFSI sector to enhance security and improve decision-making processes. In the medical industry, middleware plays a vital role in connecting various healthcare systems and applications, facilitating the exchange of patient data and ensuring interoperability between different healthcare providers. This is essential for delivering high-quality patient care, as it enables healthcare professionals to access accurate and up-to-date information, make informed decisions, and coordinate care effectively. Middleware solutions also support the integration of electronic health records (EHRs) with other healthcare systems, improving the overall efficiency of healthcare delivery. The education sector benefits from middleware by enabling seamless integration between administrative systems, learning management platforms, and other educational applications. This ensures that students, teachers, and administrators have access to the information they need when they need it, enhancing the overall learning experience. Middleware solutions also support the implementation of digital learning tools and technologies, which are becoming increasingly important in today's education landscape. In the telecommunications industry, middleware is used to integrate various network systems and applications, ensuring seamless communication and data exchange between different components. This is essential for maintaining network reliability and performance, as well as supporting the deployment of new services and technologies. Middleware solutions also enable telecommunications companies to manage and analyze large volumes of data, providing valuable insights that can be used to improve customer service and optimize network operations. The travel industry leverages middleware to connect various systems and applications, such as booking platforms, customer relationship management (CRM) systems, and payment gateways. This ensures a seamless experience for travelers, as they can access real-time information, make bookings, and manage their travel plans with ease. Middleware solutions also support the integration of advanced technologies such as artificial intelligence and machine learning, which are being used to enhance customer service and personalize travel experiences. In the manufacturing sector, middleware is used to integrate various production systems and applications, enabling real-time data exchange and communication between different components of the manufacturing process. This is essential for optimizing production efficiency, reducing downtime, and ensuring product quality. Middleware solutions also support the implementation of Industry 4.0 technologies, such as the Internet of Things (IoT) and big data analytics, which are transforming the manufacturing landscape. The aerospace and defense industry relies on middleware to integrate complex systems and applications, ensuring seamless communication and data exchange between different components. This is crucial for maintaining operational efficiency and ensuring the safety and reliability of aerospace and defense systems. Middleware solutions also support the implementation of advanced technologies, such as unmanned aerial vehicles (UAVs) and autonomous systems, which are becoming increasingly important in the industry. In the energy and utilities sector, middleware is used to integrate various systems and applications, enabling real-time data exchange and communication between different components of the energy grid. This is essential for optimizing energy production and distribution, reducing costs, and ensuring the reliability and sustainability of energy systems. Middleware solutions also support the implementation of smart grid technologies, which are transforming the energy landscape. Overall, the Global B2B Middleware Market plays a critical role in enabling organizations across various industries to optimize their operations, enhance efficiency, and achieve their strategic objectives.

Global B2B Middleware Market Outlook:

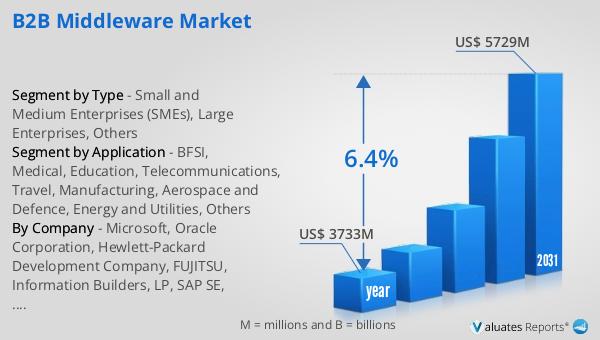

The worldwide market for B2B Middleware was estimated to be worth $3,733 million in 2024 and is anticipated to expand to a revised valuation of $5,729 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.4% over the forecast period. This growth trajectory underscores the increasing importance of middleware solutions in facilitating seamless integration and communication between disparate systems within and across organizations. As businesses continue to embrace digital transformation and adopt advanced technologies, the demand for robust middleware solutions is expected to rise. Middleware acts as a critical enabler, allowing organizations to streamline their operations, enhance interoperability, and improve overall efficiency. By providing a unified platform for data exchange, middleware solutions help businesses reduce redundancies, minimize errors, and ensure that critical processes are executed smoothly. This not only enhances productivity but also enables organizations to respond more effectively to market changes and customer demands. As the Global B2B Middleware Market continues to evolve, it is poised to play a vital role in helping organizations optimize their IT infrastructure and maintain a competitive edge in the market.

| Report Metric |

Details |

| Report Name |

B2B Middleware Market |

| Accounted market size in year |

US$ 3733 million |

| Forecasted market size in 2031 |

US$ 5729 million |

| CAGR |

6.4% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- Others

|

| Segment by Application |

- BFSI

- Medical

- Education

- Telecommunications

- Travel

- Manufacturing

- Aerospace and Defence

- Energy and Utilities

- Others

|

| By Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia) Rest of Europe

- Nordic Countries

- Asia-Pacific (China, Japan, South Korea)

- Southeast Asia (India, Australia)

- Rest of Asia

- Latin America (Mexico, Brazil)

- Rest of Latin America

- Middle East & Africa (Turkey, Saudi Arabia, UAE, Rest of MEA)

|

| By Company |

Microsoft, Oracle Corporation, Hewlett-Packard Development Company, FUJITSU, Information Builders, LP, SAP SE, OpenText Corp., Unisys, Software AG, Unisys Global Technologies, TIBCO Software Inc. |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |