What is Global Aircraft Wheel Scanning System Market?

The Global Aircraft Wheel Scanning System Market is a specialized segment within the aviation industry that focuses on the technology and equipment used to inspect and analyze aircraft wheels. These systems are crucial for ensuring the safety and efficiency of aircraft operations. Aircraft wheels endure significant stress and wear during takeoff, landing, and taxiing, making regular inspection essential. The scanning systems utilize advanced technologies to detect any defects, wear, or damage that could compromise the wheel's integrity. By providing precise and detailed data, these systems help maintenance teams make informed decisions about repairs or replacements, ultimately enhancing aircraft safety and performance. The market for these systems is driven by the increasing demand for air travel, the need for efficient maintenance practices, and stringent safety regulations. As airlines and aircraft operators strive to minimize downtime and maximize operational efficiency, the adoption of advanced wheel scanning systems is becoming increasingly important. These systems not only improve safety but also contribute to cost savings by preventing unexpected failures and extending the lifespan of aircraft wheels. Overall, the Global Aircraft Wheel Scanning System Market plays a vital role in the aviation industry's ongoing efforts to enhance safety, reliability, and efficiency.

Laser 3D Scanner, Structured Light 3D Scanner, Others in the Global Aircraft Wheel Scanning System Market:

In the realm of the Global Aircraft Wheel Scanning System Market, various types of scanners are employed to ensure the precise inspection and maintenance of aircraft wheels. Among these, the Laser 3D Scanner stands out for its ability to provide highly accurate and detailed scans. This technology uses laser beams to capture the exact dimensions and surface characteristics of the wheel. The laser scanner's precision is invaluable in detecting minute defects or wear that might not be visible to the naked eye. By creating a three-dimensional model of the wheel, maintenance teams can analyze the data to identify any potential issues that could affect the wheel's performance or safety. This level of detail is crucial for maintaining the high safety standards required in aviation. Structured Light 3D Scanners are another key technology used in the aircraft wheel scanning market. These scanners project a pattern of light onto the wheel's surface and capture the deformation of the pattern with cameras. The captured data is then processed to create a 3D model of the wheel. This method is particularly effective for capturing complex geometries and surface details, making it ideal for inspecting aircraft wheels. The structured light technology is known for its speed and accuracy, allowing for quick inspections without compromising on detail. This efficiency is essential in the fast-paced aviation industry, where minimizing downtime is a priority. In addition to Laser and Structured Light 3D Scanners, the market also includes other types of scanning technologies. These may include photogrammetry, which uses photographs to create 3D models, or ultrasonic scanning, which uses sound waves to detect internal defects. Each of these technologies has its own advantages and is chosen based on the specific requirements of the inspection. For instance, photogrammetry might be used for its ease of use and cost-effectiveness, while ultrasonic scanning could be preferred for its ability to detect subsurface defects. The diversity of scanning technologies available in the market ensures that aircraft operators can choose the most suitable option for their specific needs. The integration of these advanced scanning technologies into the maintenance routines of aircraft operators is driven by the need for enhanced safety and efficiency. By providing detailed and accurate data, these scanners enable maintenance teams to make informed decisions about repairs and replacements. This not only improves the safety and reliability of aircraft operations but also contributes to cost savings by preventing unexpected failures and extending the lifespan of aircraft wheels. As the aviation industry continues to grow and evolve, the demand for advanced wheel scanning systems is expected to increase, further driving innovation and development in this market.

Commercial Aircraft, Business Aircraft, Military Aircraft, General Aviation Aircraft, Others in the Global Aircraft Wheel Scanning System Market:

The Global Aircraft Wheel Scanning System Market finds its application across various types of aircraft, each with unique requirements and challenges. In the realm of Commercial Aircraft, these systems are indispensable due to the high frequency of flights and the significant passenger loads they carry. Regular and precise inspections of aircraft wheels are crucial to ensure safety and compliance with stringent aviation regulations. The use of advanced scanning systems allows airlines to detect wear and potential defects early, preventing costly delays and enhancing passenger safety. By maintaining optimal wheel conditions, airlines can ensure smoother operations and reduce the risk of unexpected maintenance issues. For Business Aircraft, which often operate on tight schedules and require high reliability, the use of wheel scanning systems is equally important. These aircraft, typically used by corporations and high-net-worth individuals, demand the highest standards of safety and performance. The ability to quickly and accurately assess the condition of aircraft wheels ensures that these aircraft can operate efficiently and safely, meeting the expectations of their discerning clientele. The adoption of advanced scanning technologies in this segment underscores the commitment to maintaining the highest levels of safety and reliability. In the Military Aircraft sector, the stakes are even higher. Military operations require aircraft to be in peak condition at all times, as any failure could have serious consequences. The use of aircraft wheel scanning systems in this context is critical for ensuring the readiness and safety of military aircraft. These systems provide detailed insights into the condition of the wheels, allowing for proactive maintenance and reducing the risk of operational failures. The ability to maintain aircraft in optimal condition is essential for the success of military missions and the safety of personnel. General Aviation Aircraft, which includes a wide range of aircraft used for personal, recreational, and instructional purposes, also benefit from the use of wheel scanning systems. While these aircraft may not operate as frequently as commercial or military aircraft, ensuring their safety is equally important. The use of scanning systems allows owners and operators to maintain their aircraft in top condition, enhancing safety and performance. By providing detailed data on the condition of the wheels, these systems help prevent accidents and extend the lifespan of the aircraft. In addition to these primary categories, the Global Aircraft Wheel Scanning System Market also serves other segments, such as cargo aircraft and specialized aviation services. Each of these segments has unique requirements, but the underlying need for safety and efficiency remains constant. The adoption of advanced scanning technologies across these diverse segments highlights the critical role these systems play in the aviation industry. By ensuring the safety and reliability of aircraft wheels, these systems contribute to the overall safety and efficiency of aviation operations worldwide.

Global Aircraft Wheel Scanning System Market Outlook:

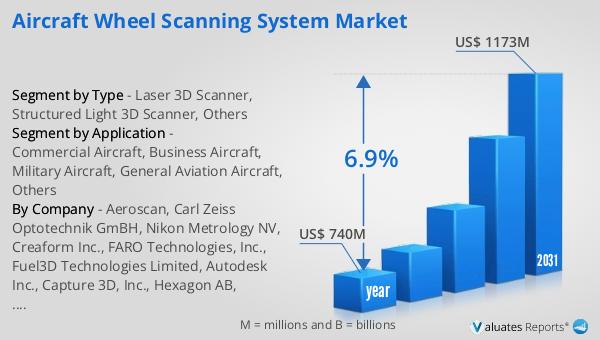

The outlook for the Global Aircraft Wheel Scanning System Market indicates a promising growth trajectory. In 2024, the market was valued at approximately US$ 740 million. Looking ahead, it is anticipated to expand significantly, reaching an estimated size of US$ 1173 million by the year 2031. This growth represents a compound annual growth rate (CAGR) of 6.9% over the forecast period. The increasing demand for air travel, coupled with the need for efficient maintenance practices and stringent safety regulations, is driving this growth. As airlines and aircraft operators strive to enhance safety and minimize downtime, the adoption of advanced wheel scanning systems is becoming increasingly important. These systems not only improve safety but also contribute to cost savings by preventing unexpected failures and extending the lifespan of aircraft wheels. The market's expansion reflects the aviation industry's ongoing efforts to enhance safety, reliability, and efficiency. As the industry continues to evolve, the demand for advanced wheel scanning systems is expected to increase, further driving innovation and development in this market. The promising growth outlook underscores the critical role these systems play in the aviation industry's commitment to safety and efficiency.

| Report Metric | Details |

| Report Name | Aircraft Wheel Scanning System Market |

| Accounted market size in year | US$ 740 million |

| Forecasted market size in 2031 | US$ 1173 million |

| CAGR | 6.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Aeroscan, Carl Zeiss Optotechnik GmBH, Nikon Metrology NV, Creaform Inc., FARO Technologies, Inc., Fuel3D Technologies Limited, Autodesk Inc., Capture 3D, Inc., Hexagon AB, Shenzhen HOLON Technology Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |