What is Mobile Emissions Catalyst - Global Market?

Mobile emissions catalysts are crucial components in reducing harmful emissions from vehicles, playing a significant role in the global market. These catalysts are designed to convert toxic gases produced by internal combustion engines into less harmful substances before they are released into the atmosphere. The global market for mobile emissions catalysts is driven by stringent environmental regulations and the increasing demand for cleaner and more efficient vehicles. As countries worldwide strive to reduce air pollution and meet emission standards, the demand for these catalysts continues to grow. They are used in various types of vehicles, including light vehicles, heavy-duty diesel engines, and motorcycles, among others. The market is characterized by continuous technological advancements aimed at improving the efficiency and effectiveness of these catalysts. Companies in this market are investing in research and development to create innovative solutions that meet the evolving needs of the automotive industry. The global market for mobile emissions catalysts is expected to expand significantly in the coming years, driven by the increasing adoption of electric and hybrid vehicles, as well as the ongoing efforts to reduce greenhouse gas emissions. This growth presents numerous opportunities for manufacturers and suppliers in the industry.

Three-Way Conversion Catalyst, Quaternary Conversion Catalyst, Others in the Mobile Emissions Catalyst - Global Market:

The mobile emissions catalyst market includes several types of catalysts, each serving a specific purpose in reducing vehicle emissions. The Three-Way Conversion Catalyst (TWC) is one of the most common types used in gasoline engines. It is designed to simultaneously convert three harmful pollutants—carbon monoxide (CO), hydrocarbons (HC), and nitrogen oxides (NOx)—into less harmful substances like carbon dioxide (CO2), water (H2O), and nitrogen (N2). This catalyst operates efficiently when the engine is running at the stoichiometric air-fuel ratio, which is the ideal balance of air and fuel for complete combustion. The TWC is highly effective in reducing emissions from gasoline-powered vehicles, making it a critical component in meeting emission standards. Another type of catalyst in the mobile emissions market is the Quaternary Conversion Catalyst. This catalyst is used in diesel engines and is designed to reduce four primary pollutants: carbon monoxide, hydrocarbons, nitrogen oxides, and particulate matter (PM). Diesel engines produce more particulate matter than gasoline engines, so the quaternary conversion catalyst is essential for reducing these emissions. It typically includes a diesel oxidation catalyst (DOC) and a diesel particulate filter (DPF) to capture and oxidize particulate matter. Additionally, selective catalytic reduction (SCR) technology is often used in conjunction with the quaternary conversion catalyst to further reduce nitrogen oxide emissions. This combination of technologies helps diesel engines meet stringent emission standards while maintaining performance and fuel efficiency. In addition to the Three-Way and Quaternary Conversion Catalysts, there are other types of catalysts used in the mobile emissions market. These include lean NOx traps (LNT) and ammonia slip catalysts (ASC). Lean NOx traps are used in lean-burn engines, which operate with excess air to improve fuel efficiency. These traps capture and store nitrogen oxides during lean operation and release them during rich operation, where they are reduced to nitrogen. Ammonia slip catalysts are used in conjunction with SCR systems to prevent the release of excess ammonia, which can occur when reducing nitrogen oxides. These catalysts ensure that ammonia is converted into harmless nitrogen and water, preventing it from being emitted into the atmosphere. The mobile emissions catalyst market is also influenced by the development of alternative fuels and powertrains. As the automotive industry shifts towards electric and hybrid vehicles, the demand for traditional emissions catalysts may decrease. However, there is still a need for catalysts in hybrid vehicles, which use internal combustion engines in conjunction with electric motors. Additionally, the development of hydrogen fuel cell vehicles presents new opportunities for catalyst manufacturers, as these vehicles require catalysts for the chemical reactions that produce electricity from hydrogen. Overall, the mobile emissions catalyst market is dynamic and evolving, driven by technological advancements and changing regulatory requirements. Manufacturers in this market must continue to innovate and adapt to meet the needs of the automotive industry and contribute to a cleaner, more sustainable future.

Light Vehicle, Heavy Duty Diesel Engine, Motorcycle, Others in the Mobile Emissions Catalyst - Global Market:

Mobile emissions catalysts are used in various applications, including light vehicles, heavy-duty diesel engines, motorcycles, and others. In light vehicles, which include passenger cars and small trucks, emissions catalysts are essential for meeting stringent emission standards. These vehicles primarily use gasoline engines, which are equipped with Three-Way Conversion Catalysts to reduce carbon monoxide, hydrocarbons, and nitrogen oxides. The effectiveness of these catalysts is crucial for ensuring that light vehicles comply with environmental regulations and contribute to cleaner air quality. As the demand for fuel-efficient and low-emission vehicles increases, the role of emissions catalysts in light vehicles becomes even more significant. Heavy-duty diesel engines, used in trucks, buses, and industrial machinery, also rely on emissions catalysts to reduce harmful emissions. These engines produce higher levels of nitrogen oxides and particulate matter compared to gasoline engines, making the use of Quaternary Conversion Catalysts essential. These catalysts, which include diesel oxidation catalysts, diesel particulate filters, and selective catalytic reduction systems, work together to minimize emissions and meet stringent regulations. The use of emissions catalysts in heavy-duty diesel engines is critical for reducing the environmental impact of these vehicles and ensuring compliance with emission standards. Motorcycles, which are popular modes of transportation in many parts of the world, also benefit from the use of emissions catalysts. These vehicles typically use smaller engines, but they can still produce significant amounts of pollutants. Emissions catalysts in motorcycles are designed to reduce carbon monoxide, hydrocarbons, and nitrogen oxides, similar to those used in light vehicles. The use of catalysts in motorcycles is important for improving air quality, especially in urban areas where these vehicles are commonly used. As emission standards for motorcycles become more stringent, the demand for effective emissions catalysts in this segment is expected to grow. In addition to light vehicles, heavy-duty diesel engines, and motorcycles, emissions catalysts are used in other applications, such as marine engines, off-road vehicles, and stationary engines. These applications often have unique emission challenges and require specialized catalyst solutions. For example, marine engines, which are used in ships and boats, produce large amounts of nitrogen oxides and sulfur oxides, requiring catalysts that can effectively reduce these emissions. Off-road vehicles, such as construction and agricultural equipment, also produce significant emissions and benefit from the use of catalysts to meet regulatory requirements. Stationary engines, used in power generation and industrial applications, also rely on emissions catalysts to reduce pollutants and improve air quality. Overall, the use of mobile emissions catalysts in various applications is essential for reducing the environmental impact of internal combustion engines and contributing to a cleaner, more sustainable future.

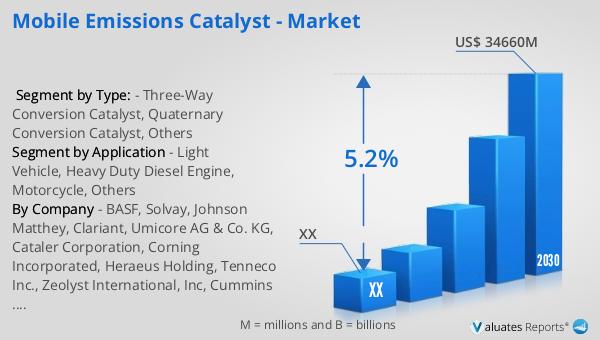

Mobile Emissions Catalyst - Global Market Outlook:

In 2023, the global market for mobile emissions catalysts was valued at approximately $24,280 million. This market is projected to grow significantly, reaching an estimated size of $34,660 million by 2030, with a compound annual growth rate (CAGR) of 5.2% during the forecast period from 2024 to 2030. This growth is driven by increasing environmental regulations and the demand for cleaner and more efficient vehicles. The North American market for mobile emissions catalysts also shows promising growth potential. Although specific figures for the North American market in 2023 and 2030 are not provided, it is expected to follow a similar growth trajectory as the global market, driven by stringent emission standards and the adoption of advanced emission control technologies. The growth of the mobile emissions catalyst market presents numerous opportunities for manufacturers and suppliers in the industry. Companies that invest in research and development to create innovative solutions that meet the evolving needs of the automotive industry are likely to benefit from this growth. As the market expands, it is essential for stakeholders to stay informed about the latest trends and developments to remain competitive and capitalize on emerging opportunities.

| Report Metric | Details |

| Report Name | Mobile Emissions Catalyst - Market |

| Forecasted market size in 2030 | US$ 34660 million |

| CAGR | 5.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BASF, Solvay, Johnson Matthey, Clariant, Umicore AG & Co. KG, Cataler Corporation, Corning Incorporated, Heraeus Holding, Tenneco Inc., Zeolyst International, Inc, Cummins Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |