What is Global Automatic Electrochlorination Systems Market?

The Global Automatic Electrochlorination Systems Market refers to the industry focused on the production and distribution of systems that generate chlorine through the process of electrochlorination. This process involves the electrolysis of saltwater or brine to produce chlorine gas, which is then used for water disinfection. These systems are crucial in ensuring safe and clean water by eliminating harmful pathogens and microorganisms. The market for these systems is driven by the increasing demand for safe drinking water, stringent regulations on water quality, and the need for efficient and cost-effective disinfection methods. Automatic electrochlorination systems are preferred due to their ability to produce chlorine on-site, reducing the need for transportation and storage of hazardous chemicals. They are widely used in various sectors, including municipal water treatment, industrial water processing, and marine applications, due to their reliability and effectiveness in maintaining water quality. As the global population continues to grow and urbanize, the demand for these systems is expected to rise, making them an essential component of modern water treatment infrastructure.

Brine System, Seawater System in the Global Automatic Electrochlorination Systems Market:

In the Global Automatic Electrochlorination Systems Market, two primary systems are utilized: the Brine System and the Seawater System. The Brine System involves the use of a concentrated salt solution, or brine, which is subjected to electrolysis to produce chlorine. This system is particularly advantageous in areas where seawater is not readily available or where the quality of seawater is not suitable for electrochlorination. The brine system is highly efficient and can be easily controlled to produce the desired amount of chlorine, making it suitable for various applications, including municipal water treatment and industrial processes. On the other hand, the Seawater System utilizes natural seawater as the source for electrochlorination. This system is ideal for coastal regions where seawater is abundant and easily accessible. The seawater system is environmentally friendly, as it uses a natural resource and does not require the transportation or storage of chemicals. It is widely used in marine applications, such as on ships and offshore platforms, where it provides a reliable source of chlorine for disinfection purposes. Both systems have their unique advantages and are chosen based on the specific needs and conditions of the application. The choice between a brine system and a seawater system depends on factors such as availability of resources, cost considerations, and the specific requirements of the water treatment process. In the context of the global market, both systems play a crucial role in meeting the diverse needs of different regions and industries. The brine system is often preferred in inland areas or regions with limited access to seawater, while the seawater system is favored in coastal areas where seawater is plentiful. The versatility and adaptability of these systems make them essential components of the global electrochlorination market, catering to a wide range of applications and ensuring the provision of safe and clean water across the globe. As the demand for efficient and sustainable water treatment solutions continues to grow, the importance of both brine and seawater systems in the global market is expected to increase, driving innovation and development in this field.

Municipal, Commercial, Industrial, Marine in the Global Automatic Electrochlorination Systems Market:

The Global Automatic Electrochlorination Systems Market finds extensive usage across various sectors, including municipal, commercial, industrial, and marine applications. In the municipal sector, these systems are crucial for ensuring the safety and quality of public water supplies. They are used in water treatment plants to disinfect drinking water, making it safe for consumption by eliminating harmful bacteria and viruses. The ability to produce chlorine on-site reduces the need for transporting and storing hazardous chemicals, enhancing safety and efficiency in municipal water treatment processes. In the commercial sector, automatic electrochlorination systems are used in facilities such as hotels, resorts, and recreational centers to maintain the quality of swimming pools and spas. These systems ensure that the water is free from pathogens, providing a safe and enjoyable experience for guests. In the industrial sector, electrochlorination systems are employed in various processes, including cooling water treatment, wastewater treatment, and process water disinfection. They help industries comply with stringent environmental regulations by providing an effective means of water treatment and disinfection. In the marine sector, these systems are used on ships and offshore platforms to treat ballast water and prevent the spread of invasive species. They provide a reliable source of chlorine for disinfection, ensuring the safety and compliance of marine operations. The versatility and effectiveness of automatic electrochlorination systems make them indispensable in these sectors, contributing to the overall safety and sustainability of water resources. As the demand for clean and safe water continues to rise, the usage of these systems in various applications is expected to grow, highlighting their importance in modern water treatment infrastructure.

Global Automatic Electrochlorination Systems Market Outlook:

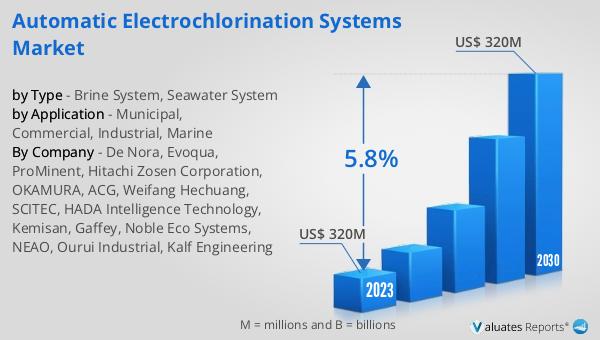

The outlook for the Global Automatic Electrochlorination Systems Market indicates a stable growth trajectory. In 2023, the market was valued at approximately US$ 320 million. Looking ahead to 2030, it is projected to maintain this valuation, with a compound annual growth rate (CAGR) of 5.8% anticipated during the forecast period from 2024 to 2030. This growth is driven by several factors, including the increasing demand for safe and clean water, the need for efficient and cost-effective disinfection methods, and the growing awareness of the importance of water quality. The market's stability is also supported by the widespread adoption of automatic electrochlorination systems across various sectors, including municipal, commercial, industrial, and marine applications. These systems offer numerous advantages, such as on-site chlorine production, reduced chemical handling, and enhanced safety, making them a preferred choice for water treatment and disinfection. As the global population continues to grow and urbanize, the demand for these systems is expected to rise, further driving market growth. The projected CAGR of 5.8% reflects the market's potential for expansion and innovation, as companies continue to develop advanced solutions to meet the evolving needs of water treatment and disinfection. Overall, the Global Automatic Electrochlorination Systems Market is poised for steady growth, driven by the increasing demand for safe and sustainable water treatment solutions.

| Report Metric | Details |

| Report Name | Automatic Electrochlorination Systems Market |

| Accounted market size in 2023 | US$ 320 million |

| Forecasted market size in 2030 | US$ 320 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | De Nora, Evoqua, ProMinent, Hitachi Zosen Corporation, OKAMURA, ACG, Weifang Hechuang, SCITEC, HADA Intelligence Technology, Kemisan, Gaffey, Noble Eco Systems, NEAO, Ourui Industrial, Kalf Engineering |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |