What is Global All-Electric E-Commerce Delivery Market?

The Global All-Electric E-Commerce Delivery Market refers to the sector of the e-commerce industry that utilizes electric vehicles (EVs) for the delivery of goods. This market is driven by the increasing demand for sustainable and eco-friendly delivery solutions, as traditional delivery methods often rely on fossil fuels, contributing to pollution and climate change. Electric vehicles, on the other hand, produce zero emissions, making them an attractive option for companies looking to reduce their carbon footprint. The market encompasses a wide range of electric delivery vehicles, including electric vans, trucks, and bikes, which are used to transport goods from warehouses to consumers' doorsteps. The adoption of all-electric delivery vehicles is also supported by advancements in battery technology, which have improved the range and efficiency of these vehicles. Additionally, government incentives and regulations aimed at promoting the use of electric vehicles further boost the growth of this market. As more consumers and businesses prioritize sustainability, the Global All-Electric E-Commerce Delivery Market is expected to continue expanding, offering a greener alternative to traditional delivery methods.

B2C, B2B in the Global All-Electric E-Commerce Delivery Market:

In the context of the Global All-Electric E-Commerce Delivery Market, B2C (Business-to-Consumer) and B2B (Business-to-Business) models play significant roles. B2C refers to transactions where businesses sell products directly to consumers. In this market, electric delivery vehicles are used to transport goods purchased online from e-commerce platforms directly to the consumer's home. This model benefits from the growing consumer preference for online shopping and the increasing awareness of environmental issues. Electric vehicles offer a quieter, cleaner, and more efficient delivery solution, enhancing the overall customer experience. On the other hand, B2B involves transactions between businesses. In this scenario, electric delivery vehicles are used to transport goods from one business to another, such as from manufacturers to retailers or from wholesalers to smaller businesses. The use of electric vehicles in B2B transactions can lead to significant cost savings for businesses due to lower fuel and maintenance costs. Additionally, businesses can enhance their corporate social responsibility (CSR) profiles by adopting sustainable delivery practices. Both B2C and B2B models benefit from the advancements in electric vehicle technology, such as improved battery life and faster charging times, which make electric delivery vehicles more practical and reliable. Furthermore, the integration of smart logistics and route optimization software can enhance the efficiency of electric delivery vehicles, reducing delivery times and operational costs. As businesses and consumers alike become more environmentally conscious, the adoption of electric delivery vehicles in both B2C and B2B models is likely to increase, driving the growth of the Global All-Electric E-Commerce Delivery Market.

3C Products, Fresh Products, Others in the Global All-Electric E-Commerce Delivery Market:

The Global All-Electric E-Commerce Delivery Market finds extensive usage in various product categories, including 3C products, fresh products, and others. 3C products refer to computers, communications, and consumer electronics. These items are often high-value and require careful handling during delivery. Electric delivery vehicles, with their smooth and quiet operation, are well-suited for transporting delicate 3C products. Additionally, the use of electric vehicles can help reduce the carbon footprint associated with the delivery of these products, aligning with the sustainability goals of many tech companies. Fresh products, such as groceries, fruits, vegetables, and other perishable items, also benefit from electric delivery solutions. Electric vehicles equipped with refrigeration units can maintain the required temperature for fresh products, ensuring they reach consumers in optimal condition. The zero-emission nature of electric vehicles is particularly advantageous for the delivery of fresh products, as it helps preserve air quality and reduce pollution in urban areas. Other product categories that utilize electric delivery vehicles include clothing, books, household items, and more. The versatility of electric delivery vehicles makes them suitable for a wide range of goods, contributing to their growing adoption in the e-commerce industry. Moreover, the use of electric vehicles for last-mile delivery can enhance the overall efficiency of the supply chain, reducing delivery times and operational costs. As the demand for sustainable and eco-friendly delivery solutions continues to rise, the Global All-Electric E-Commerce Delivery Market is expected to expand its reach across various product categories, offering a greener alternative to traditional delivery methods.

Global All-Electric E-Commerce Delivery Market Outlook:

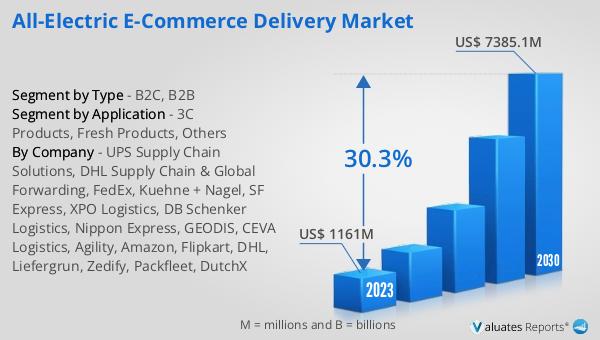

The global All-Electric E-Commerce Delivery market was valued at US$ 1161 million in 2023 and is anticipated to reach US$ 7385.1 million by 2030, witnessing a CAGR of 30.3% during the forecast period 2024-2030. This significant growth reflects the increasing adoption of electric vehicles for e-commerce deliveries, driven by the need for sustainable and eco-friendly delivery solutions. The market's expansion is supported by advancements in battery technology, government incentives, and the growing awareness of environmental issues among consumers and businesses. As more companies prioritize sustainability and seek to reduce their carbon footprint, the demand for electric delivery vehicles is expected to rise, contributing to the market's robust growth. The transition to all-electric delivery solutions not only helps in reducing emissions but also offers cost savings in terms of fuel and maintenance. With the continuous improvement in electric vehicle technology and infrastructure, the Global All-Electric E-Commerce Delivery Market is poised for substantial growth in the coming years, providing a greener and more efficient alternative to traditional delivery methods.

| Report Metric | Details |

| Report Name | All-Electric E-Commerce Delivery Market |

| Accounted market size in 2023 | US$ 1161 million |

| Forecasted market size in 2030 | US$ 7385.1 million |

| CAGR | 30.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | UPS Supply Chain Solutions, DHL Supply Chain & Global Forwarding, FedEx, Kuehne + Nagel, SF Express, XPO Logistics, DB Schenker Logistics, Nippon Express, GEODIS, CEVA Logistics, Agility, Amazon, Flipkart, DHL, Liefergrun, Zedify, Packfleet, DutchX |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |