What is Global Head Protection Safety Helmets Market?

The Global Head Protection Safety Helmets Market refers to the worldwide industry focused on the production and distribution of helmets designed to protect the head from injuries. These helmets are essential in various sectors, including construction, manufacturing, mining, and sports, where head injuries are a significant risk. The market encompasses a wide range of helmet types, each tailored to specific hazards and environments. Innovations in materials and design have led to helmets that offer enhanced protection, comfort, and durability. The market is driven by stringent safety regulations, increasing awareness about workplace safety, and the growing emphasis on reducing occupational hazards. As industries continue to prioritize employee safety, the demand for high-quality head protection helmets is expected to rise, making this market a crucial component of global occupational health and safety initiatives.

Class G, Class E, Class C in the Global Head Protection Safety Helmets Market:

Class G, Class E, and Class C helmets are categories within the Global Head Protection Safety Helmets Market, each designed to meet specific safety standards and requirements. Class G helmets, also known as General helmets, are designed to reduce the danger of contact with low-voltage conductors and offer dielectric protection up to 2,200 volts. These helmets are commonly used in construction and utility work where there is a risk of electrical hazards. They are made from materials that provide a balance between impact resistance and electrical insulation. Class E helmets, or Electrical helmets, provide a higher level of protection against electrical hazards, with dielectric protection up to 20,000 volts. These helmets are essential for workers in high-voltage environments, such as electrical linemen and utility workers. They are constructed from materials that offer superior electrical insulation and impact resistance, ensuring maximum safety in hazardous conditions. Class C helmets, or Conductive helmets, do not provide any electrical protection and are primarily designed for impact protection. These helmets are typically used in environments where there is no risk of electrical hazards, such as manufacturing, mining, and general industrial applications. They are made from lightweight materials that offer comfort and ease of use while providing adequate protection against head injuries. Each class of helmet is designed to meet specific safety standards and requirements, ensuring that workers are adequately protected in their respective environments. The choice of helmet depends on the specific hazards present in the workplace and the level of protection required. The Global Head Protection Safety Helmets Market continues to evolve, with ongoing advancements in materials and design aimed at enhancing the safety and comfort of these essential protective devices.

Industrial Use, Government in the Global Head Protection Safety Helmets Market:

The usage of Global Head Protection Safety Helmets Market in industrial and government sectors is extensive and critical for ensuring the safety of workers and personnel. In industrial settings, head protection helmets are a fundamental component of personal protective equipment (PPE). Industries such as construction, manufacturing, mining, and oil and gas rely heavily on these helmets to protect workers from head injuries caused by falling objects, collisions, and other hazards. In construction, for example, workers are often exposed to risks from heavy machinery, falling debris, and structural collapses. Helmets designed for this environment are built to withstand significant impact and provide a secure fit to prevent displacement during accidents. In manufacturing, helmets protect workers from head injuries caused by machinery, tools, and materials. The design of these helmets often includes features such as adjustable straps and ventilation to ensure comfort during long hours of use. In the mining industry, helmets are crucial for protecting workers from falling rocks, low ceilings, and other underground hazards. These helmets are typically equipped with additional features such as built-in lights and communication systems to enhance safety and efficiency. In the oil and gas sector, helmets protect workers from head injuries caused by explosions, falls, and equipment malfunctions. These helmets are designed to withstand extreme conditions and provide maximum protection in hazardous environments. In the government sector, head protection helmets are used by military personnel, law enforcement officers, and emergency responders. Military helmets are designed to provide ballistic protection and are equipped with features such as night vision mounts and communication systems. Law enforcement helmets protect officers from head injuries during riots, protests, and other high-risk situations. These helmets are often equipped with visors and face shields to provide additional protection. Emergency responders, such as firefighters and paramedics, use helmets to protect themselves from falling debris, heat, and other hazards encountered during rescue operations. These helmets are designed to be lightweight and comfortable, allowing for quick and efficient movement in emergency situations. The Global Head Protection Safety Helmets Market plays a vital role in ensuring the safety and well-being of workers and personnel in both industrial and government sectors. The continuous development and improvement of helmet designs and materials are essential for meeting the evolving safety needs of these critical industries.

Global Head Protection Safety Helmets Market Outlook:

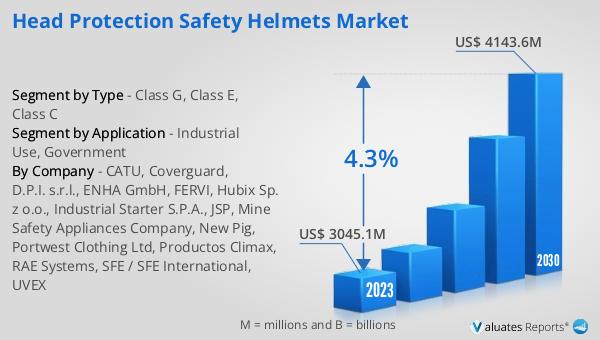

The global Head Protection Safety Helmets market was valued at US$ 3045.1 million in 2023 and is anticipated to reach US$ 4143.6 million by 2030, witnessing a CAGR of 4.3% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the head protection safety helmets market over the next several years. The increasing awareness about workplace safety and the stringent regulations imposed by governments and safety organizations are key factors driving this growth. As industries continue to prioritize the safety and well-being of their employees, the demand for high-quality head protection helmets is expected to rise. The market is also benefiting from advancements in materials and technology, which are leading to the development of helmets that offer enhanced protection, comfort, and durability. The projected growth in the market value reflects the increasing adoption of these helmets across various industries and sectors. The continuous focus on improving safety standards and reducing occupational hazards will further contribute to the expansion of the Global Head Protection Safety Helmets Market.

| Report Metric | Details |

| Report Name | Head Protection Safety Helmets Market |

| Accounted market size in 2023 | US$ 3045.1 million |

| Forecasted market size in 2030 | US$ 4143.6 million |

| CAGR | 4.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | CATU, Coverguard, D.P.I. s.r.l., ENHA GmbH, FERVI, Hubix Sp. z o.o., Industrial Starter S.P.A., JSP, Mine Safety Appliances Company, New Pig, Portwest Clothing Ltd, Productos Climax, RAE Systems, SFE / SFE International, UVEX |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |