What is Global Class 1E Nuclear Power Plant Instrumentation Cables Market?

The Global Class 1E Nuclear Power Plant Instrumentation Cables Market refers to the specialized market for cables used in nuclear power plants that meet the stringent safety and performance standards classified under Class 1E. These cables are essential for the reliable operation of nuclear power plants, ensuring the safe transmission of signals and power within the plant's critical systems. They are designed to withstand extreme conditions such as high radiation, temperature, and pressure, which are typical in nuclear environments. The market encompasses various types of cables, including those used inside and outside the reactor, and is driven by the need for enhanced safety measures, regulatory compliance, and the modernization of aging nuclear facilities. The demand for these cables is influenced by the global expansion of nuclear power generation, technological advancements, and the increasing focus on sustainable and reliable energy sources.

Nuclear Island Cable, Conventional Island Cable in the Global Class 1E Nuclear Power Plant Instrumentation Cables Market:

Nuclear Island Cables and Conventional Island Cables are two primary segments within the Global Class 1E Nuclear Power Plant Instrumentation Cables Market. Nuclear Island Cables are specifically designed for use within the nuclear island, which is the section of a nuclear power plant that houses the reactor and its associated systems. These cables must meet the highest safety and performance standards due to their proximity to the reactor core, where they are exposed to high levels of radiation, extreme temperatures, and pressure. They are used to transmit critical signals and power necessary for the operation and control of the reactor, ensuring the plant's safety and efficiency. On the other hand, Conventional Island Cables are used in the conventional island, which includes the non-nuclear parts of the power plant, such as the turbine building and auxiliary systems. While these cables also need to meet stringent safety standards, they are not subjected to the same extreme conditions as Nuclear Island Cables. Conventional Island Cables are used for various applications, including power distribution, control systems, and communication networks within the plant. Both types of cables play a crucial role in the overall operation of a nuclear power plant, ensuring the safe and efficient transmission of signals and power across different sections of the facility. The market for these cables is driven by the need for reliable and durable solutions that can withstand the harsh conditions of a nuclear power plant, as well as the ongoing efforts to modernize and upgrade existing facilities.

Inside The Reactors, Outside The Reactor in the Global Class 1E Nuclear Power Plant Instrumentation Cables Market:

The usage of Global Class 1E Nuclear Power Plant Instrumentation Cables Market can be broadly categorized into two areas: Inside The Reactors and Outside The Reactor. Inside the reactors, these cables are used in the most critical and sensitive parts of the nuclear power plant. They are responsible for transmitting vital signals and power necessary for the operation and control of the reactor core. These cables must be highly resistant to radiation, extreme temperatures, and pressure, ensuring they can perform reliably under the harshest conditions. They are used in various applications, including monitoring and control systems, safety systems, and communication networks within the reactor. The reliability and durability of these cables are paramount, as any failure could have severe consequences for the plant's safety and operation. Outside the reactor, Class 1E cables are used in other parts of the nuclear power plant, such as the turbine building, auxiliary systems, and control rooms. While these areas are not exposed to the same extreme conditions as the reactor core, the cables still need to meet stringent safety and performance standards. They are used for power distribution, control systems, and communication networks, ensuring the smooth and efficient operation of the plant. The cables used outside the reactor must be durable and reliable, capable of withstanding the demanding environment of a nuclear power plant. The market for these cables is driven by the need for enhanced safety measures, regulatory compliance, and the modernization of aging nuclear facilities. The demand for reliable and durable cables is essential for the safe and efficient operation of nuclear power plants, ensuring the continuous and stable generation of nuclear energy.

Global Class 1E Nuclear Power Plant Instrumentation Cables Market Outlook:

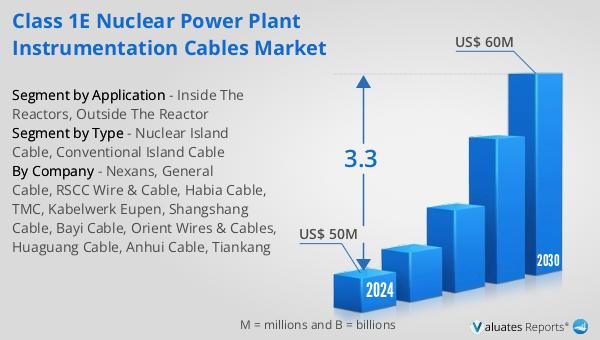

The global Class 1E Nuclear Power Plant Instrumentation Cables market is expected to grow from US$ 50 million in 2024 to US$ 60 million by 2030, with a Compound Annual Growth Rate (CAGR) of 3.3% during the forecast period. The top four manufacturers globally hold a significant share of over 55% of the market. China is the largest market, accounting for over 30% of the global share, followed by Europe and the US, which together hold about 50% of the market share. In terms of product segments, Conventional Island Cable is the largest, with a share of over 85%. This growth is driven by the increasing demand for reliable and durable cables that can withstand the harsh conditions of nuclear power plants, as well as the ongoing efforts to modernize and upgrade existing facilities. The market is also influenced by the global expansion of nuclear power generation, technological advancements, and the increasing focus on sustainable and reliable energy sources. The demand for these cables is essential for the safe and efficient operation of nuclear power plants, ensuring the continuous and stable generation of nuclear energy.

| Report Metric | Details |

| Report Name | Class 1E Nuclear Power Plant Instrumentation Cables Market |

| Accounted market size in 2024 | US$ 50 million |

| Forecasted market size in 2030 | US$ 60 million |

| CAGR | 3.3 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Nexans, General Cable, RSCC Wire & Cable, Habia Cable, TMC, Kabelwerk Eupen, Shangshang Cable, Bayi Cable, Orient Wires & Cables, Huaguang Cable, Anhui Cable, Tiankang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |