What is Global Emollient Market?

The global emollient market refers to the industry that produces and sells substances designed to soften and moisturize the skin. Emollients are key ingredients in many personal care products, including lotions, creams, and ointments. They work by forming a protective barrier on the skin's surface, which helps to retain moisture and prevent dryness. This market encompasses a wide range of products, from synthetic to natural oils, catering to various consumer preferences and needs. The demand for emollients is driven by their extensive use in skincare, hair care, and other personal care applications. As consumers become more aware of the benefits of maintaining healthy skin and hair, the market for emollients continues to grow. Additionally, the increasing prevalence of skin conditions such as eczema and psoriasis has further fueled the demand for effective moisturizing products. The global emollient market is characterized by a diverse range of products and a competitive landscape, with numerous manufacturers vying for market share.

Synthetic, Natural oil in the Global Emollient Market:

In the global emollient market, synthetic and natural oil-based emollients play significant roles. Synthetic emollients are man-made substances that mimic the properties of natural oils. They are often preferred for their consistency, stability, and cost-effectiveness. Common synthetic emollients include ingredients like mineral oil, petrolatum, and silicones. These substances are widely used in various personal care products due to their ability to provide long-lasting moisture and a smooth texture. On the other hand, natural oil-based emollients are derived from plant or animal sources. Examples include coconut oil, shea butter, and jojoba oil. These natural oils are favored for their perceived health benefits and eco-friendliness. They are rich in essential fatty acids, vitamins, and antioxidants, which can nourish and protect the skin. The choice between synthetic and natural oil-based emollients often depends on consumer preferences, product formulation requirements, and regulatory considerations. Both types of emollients have their unique advantages and are used in a wide range of applications, from skincare to hair care. The global emollient market continues to evolve as manufacturers innovate and develop new formulations to meet the diverse needs of consumers.

Skin Care, Hair Care, Oral Care, Others in the Global Emollient Market:

The global emollient market finds extensive usage in various areas, including skincare, hair care, oral care, and others. In skincare, emollients are essential for maintaining healthy and hydrated skin. They are used in products such as moisturizers, lotions, and creams to prevent dryness, flakiness, and irritation. Emollients help to create a protective barrier on the skin's surface, locking in moisture and improving skin texture. In hair care, emollients are used in conditioners, shampoos, and styling products to provide moisture, reduce frizz, and enhance shine. They help to smooth the hair cuticle, making it more manageable and less prone to breakage. In oral care, emollients are used in products like toothpaste and mouthwash to provide a smooth texture and prevent dryness in the mouth. They help to maintain oral health by keeping the mucous membranes hydrated. Other applications of emollients include their use in pharmaceuticals, where they are incorporated into ointments and creams to treat various skin conditions. Emollients are also used in baby care products, sun care products, and cosmetics. The versatility and effectiveness of emollients make them a crucial component in a wide range of personal care and healthcare products.

Global Emollient Market Outlook:

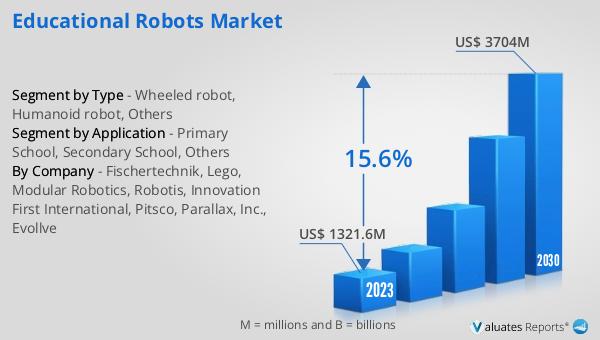

The global emollient market is anticipated to expand from USD 1,349.6 million in 2024 to USD 1,565.2 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 2.5% over the forecast period. The top three global manufacturers collectively hold a market share exceeding 50%. Europe stands as the largest market, accounting for approximately 35% of the total share, followed by China and North America, both of which hold shares exceeding 40%. In terms of product segmentation, synthetic emollients dominate the market with a share surpassing 75%. This data underscores the significant role of synthetic emollients in the industry, driven by their cost-effectiveness and consistent performance. The market dynamics are shaped by various factors, including consumer preferences, regulatory frameworks, and technological advancements. As the demand for personal care products continues to rise, the emollient market is poised for steady growth. The competitive landscape is marked by innovation and strategic collaborations among key players, aiming to cater to the evolving needs of consumers.

| Report Metric | Details |

| Report Name | Emollient Market |

| Accounted market size in 2024 | US$ 1349.6 million |

| Forecasted market size in 2030 | US$ 1565.2 million |

| CAGR | 2.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Lubrizol Corporation, Ashland Inc, Evonik Industries AG, Stepan, AAK AB, Lipo Chemicals, Innospec Inc., Lonza Group Ltd, Kunshan Shuangyou |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |