What is Global Electronic Faucets Market?

The Global Electronic Faucets Market refers to the worldwide industry focused on the production and sale of faucets that operate electronically. These faucets are designed to provide water flow without the need for manual operation, often using sensors or touch technology. The market encompasses a variety of products, including touchless and touched electronic faucets, which are used in various settings such as residential homes, commercial buildings, medical institutions, and public spaces. The demand for electronic faucets is driven by factors such as increasing awareness of hygiene, water conservation efforts, and the convenience offered by these advanced fixtures. As technology continues to evolve, the market is expected to see further innovations and growth, catering to the needs of different consumer segments across the globe.

Touchless Electronic Faucets, Touched Electronic Faucets in the Global Electronic Faucets Market:

Touchless electronic faucets and touched electronic faucets are two primary segments within the Global Electronic Faucets Market. Touchless electronic faucets operate using sensors that detect the presence of hands or objects, automatically activating the water flow. These faucets are particularly popular in public restrooms, hospitals, and other high-traffic areas where hygiene is a top priority. The touchless technology minimizes the risk of cross-contamination and the spread of germs, making them an ideal choice for environments that require stringent cleanliness standards. On the other hand, touched electronic faucets require a light touch or tap to activate the water flow. These faucets often come with features such as temperature control and preset water flow settings, providing users with a customized experience. Touched electronic faucets are commonly used in residential settings, offering a blend of modern convenience and aesthetic appeal. Both types of electronic faucets contribute to water conservation by providing controlled water flow, reducing wastage. The integration of smart technology in these faucets allows for additional functionalities such as monitoring water usage and detecting leaks, further enhancing their appeal to environmentally conscious consumers. As the demand for smart home and building solutions continues to rise, the market for both touchless and touched electronic faucets is expected to expand, offering innovative solutions to meet the diverse needs of consumers.

Hotels, Offices, Medical Institutions, Residential, Others in the Global Electronic Faucets Market:

The usage of electronic faucets in various areas such as hotels, offices, medical institutions, residential spaces, and others highlights their versatility and growing popularity. In hotels, electronic faucets are often installed in guest rooms, public restrooms, and spa areas to provide a luxurious and hygienic experience for guests. The touchless technology ensures that guests can enjoy a seamless and germ-free interaction with the faucets, enhancing their overall stay. In offices, electronic faucets are commonly found in restrooms and kitchen areas, promoting a clean and professional environment. The convenience of touchless operation reduces the need for frequent cleaning and maintenance, making them a practical choice for busy workplaces. Medical institutions, such as hospitals and clinics, prioritize hygiene and infection control, making touchless electronic faucets an essential fixture in patient rooms, operating theaters, and public restrooms. These faucets help minimize the risk of cross-contamination, ensuring a safer environment for both patients and healthcare professionals. In residential settings, electronic faucets are becoming increasingly popular in kitchens and bathrooms, offering homeowners a modern and convenient solution for their daily needs. The ability to control water flow and temperature with a simple touch or sensor activation adds a touch of sophistication to home interiors. Other areas where electronic faucets are used include airports, shopping malls, and educational institutions, where high foot traffic necessitates the use of hygienic and efficient fixtures. The growing awareness of water conservation and the need for sustainable solutions further drive the adoption of electronic faucets across these diverse settings.

Global Electronic Faucets Market Outlook:

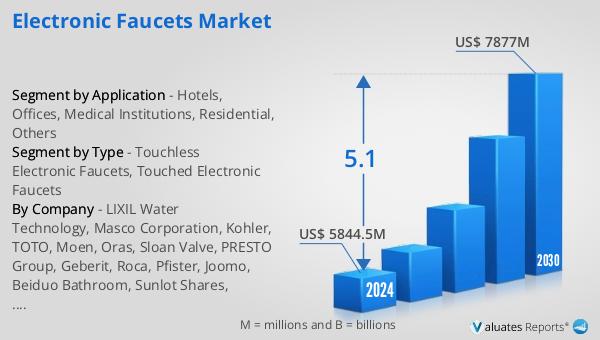

The global Electronic Faucets market is anticipated to experience significant growth, with projections indicating an increase from US$ 5844.5 million in 2024 to US$ 7877 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 5.1% during the forecast period. The market is dominated by the top four manufacturers, who collectively hold a share of approximately 30%. The Asia-Pacific region emerges as the largest market, accounting for about 50% of the global share, followed by Europe and North America, each holding around 30%. Within the product categories, Touchless Electronic Faucets represent the largest segment, commanding nearly 95% of the market share. This dominance is attributed to the increasing demand for hygiene and convenience, particularly in public and commercial spaces. The touchless technology, which minimizes physical contact and reduces the risk of germ transmission, is highly favored in environments such as hospitals, offices, and hotels. As the market continues to evolve, the focus on innovation and the integration of smart technologies are expected to further drive the adoption of electronic faucets, catering to the diverse needs of consumers across different regions.

| Report Metric | Details |

| Report Name | Electronic Faucets Market |

| Accounted market size in 2024 | US$ 5844.5 million |

| Forecasted market size in 2030 | US$ 7877 million |

| CAGR | 5.1 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | LIXIL Water Technology, Masco Corporation, Kohler, TOTO, Moen, Oras, Sloan Valve, PRESTO Group, Geberit, Roca, Pfister, Joomo, Beiduo Bathroom, Sunlot Shares, Advanced Modern Technologies, Fuzhou Sanxie Electron, TCK, ZILONG, YOCOSS Electronic Equipment, Fuzhou GIBO Induction Satinary Ware |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |