What is Global Rhythm Machines Market?

The Global Rhythm Machines Market refers to the worldwide industry focused on the production, distribution, and sale of rhythm machines, also known as drum machines. These devices are electronic musical instruments designed to imitate the sound of drums, cymbals, and other percussion instruments. They are widely used in various music genres, including electronic dance music (EDM), hip-hop, and pop, among others. The market encompasses a range of products from high-end professional machines to more affordable options for amateurs and hobbyists. The growth of this market is driven by the increasing popularity of electronic music, advancements in technology, and the rising number of music producers and enthusiasts globally. Companies in this market are continuously innovating to offer more features, better sound quality, and user-friendly interfaces to meet the diverse needs of their customers.

High-end Rhythm Machines, Mid-low end Rhythm Machines in the Global Rhythm Machines Market:

High-end rhythm machines are designed for professional musicians and producers who require advanced features, superior sound quality, and robust build quality. These machines often come with a wide range of sounds, extensive programmability, and the ability to integrate seamlessly with other music production equipment. They are typically used in professional studios and live performances, where reliability and versatility are crucial. Brands like Roland, Native Instruments, and Novation Focusrite are well-known for their high-end rhythm machines, which are often priced at a premium due to their advanced capabilities and superior build quality. On the other hand, mid-low end rhythm machines cater to amateurs, hobbyists, and semi-professional musicians who need reliable and versatile equipment but at a more affordable price point. These machines may not have all the advanced features of their high-end counterparts but still offer a good range of sounds and programmability options. They are ideal for home studios, small gigs, and practice sessions. Companies in this segment focus on providing value for money, ensuring that their products are accessible to a broader audience without compromising too much on quality. The global rhythm machines market is thus segmented into these two main categories, each serving different customer needs and preferences. The high-end segment is characterized by innovation and premium pricing, while the mid-low end segment focuses on affordability and accessibility. Both segments are essential for the overall growth and diversity of the market, as they cater to different levels of expertise and budget constraints. As technology continues to evolve, the lines between these segments may blur, with mid-low end machines incorporating more advanced features and high-end machines becoming more affordable. This dynamic nature of the market ensures that there is always something new and exciting for musicians and producers at all levels.

Professional Musician, Amateur in the Global Rhythm Machines Market:

The usage of rhythm machines varies significantly between professional musicians and amateurs. Professional musicians often rely on high-end rhythm machines for their studio recordings and live performances. These machines provide them with the flexibility to create complex rhythms, experiment with different sounds, and integrate seamlessly with other music production tools. For instance, a professional DJ might use a high-end rhythm machine to create custom beats for their sets, ensuring that their performances are unique and engaging. Similarly, a music producer might use these machines to lay down the foundational beats for a track, allowing them to focus on other elements like melody and harmony. The advanced features and superior sound quality of high-end rhythm machines make them indispensable tools for professionals who need reliable and versatile equipment to bring their musical visions to life. On the other hand, amateurs and hobbyists typically use mid-low end rhythm machines for their music-making endeavors. These machines are more affordable and user-friendly, making them accessible to individuals who are just starting out or who make music as a hobby. An amateur musician might use a mid-low end rhythm machine to practice their drumming skills, create backing tracks for their songs, or experiment with different genres of music. These machines provide a great way for beginners to learn the basics of rhythm and beat-making without having to invest in expensive equipment. Additionally, the portability and ease of use of mid-low end rhythm machines make them ideal for casual jam sessions, small gigs, and home studio setups. Despite the differences in usage, both professional musicians and amateurs benefit from the versatility and creativity that rhythm machines offer. Whether it's creating intricate beats for a professional track or experimenting with new sounds in a home studio, rhythm machines play a crucial role in the music-making process for individuals at all levels of expertise.

Global Rhythm Machines Market Outlook:

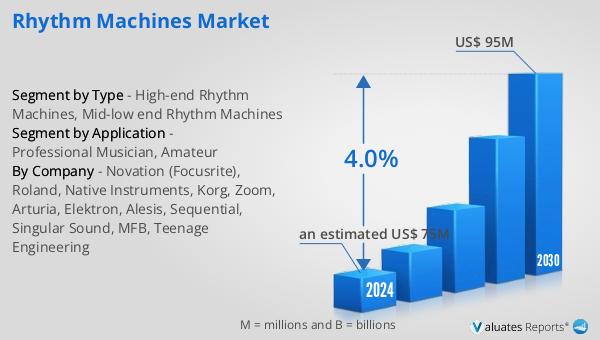

The global rhythm machines market is anticipated to grow from an estimated US$ 75 million in 2024 to US$ 95 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.0% during this period. In 2019, Novation Focusrite held a significant share of the market, accounting for 14.99% of the global rhythm machines revenue. Other notable players in the market include Roland and Native Instruments, which together accounted for 14.72% and 13.40% of the market share, respectively. This growth is driven by the increasing demand for rhythm machines across various segments, including professional musicians and amateurs. Companies in this market are continuously innovating to offer better features, improved sound quality, and more user-friendly interfaces to meet the diverse needs of their customers. The competitive landscape of the market is characterized by the presence of both established brands and new entrants, each striving to capture a larger share of the market through product innovation and strategic partnerships. As the popularity of electronic music continues to rise, the demand for rhythm machines is expected to grow, providing ample opportunities for companies to expand their market presence and enhance their product offerings.

| Report Metric | Details |

| Report Name | Rhythm Machines Market |

| Accounted market size in 2024 | an estimated US$ 75 in million |

| Forecasted market size in 2030 | US$ 95 million |

| CAGR | 4.0% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Novation (Focusrite), Roland, Native Instruments, Korg, Zoom, Arturia, Elektron, Alesis, Sequential, Singular Sound, MFB, Teenage Engineering |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |