What is Global Diagnosis and Treatment Of Hemorrhoids Market?

The Global Diagnosis and Treatment of Hemorrhoids Market encompasses a wide range of medical solutions aimed at diagnosing and treating hemorrhoids, which are swollen veins in the lower rectum and anus. This market includes various diagnostic tools and treatment methods, ranging from non-invasive procedures to surgical interventions. Hemorrhoids can cause discomfort, pain, and bleeding, making effective diagnosis and treatment crucial for patient well-being. The market is driven by factors such as the increasing prevalence of hemorrhoids due to lifestyle changes, aging populations, and the rising awareness of available treatments. Medical professionals and healthcare facilities are continually seeking advanced and efficient methods to manage this condition, contributing to the growth and innovation within this market. The global scope of this market highlights the universal need for effective hemorrhoid management solutions, catering to diverse patient populations across different regions.

Sclerotherapy Injector, Infrared Coagulator, Bipolar Probe, Cryotherapy Device, Hemorrhoid Laser Probes, Others in the Global Diagnosis and Treatment Of Hemorrhoids Market:

The Global Diagnosis and Treatment of Hemorrhoids Market includes a variety of devices and tools designed to address hemorrhoids effectively. Sclerotherapy injectors are used to inject a sclerosing agent into the hemorrhoid, causing it to shrink and eventually disappear. This minimally invasive procedure is often preferred for its simplicity and effectiveness. Infrared coagulators use infrared light to coagulate the blood vessels in the hemorrhoid, leading to its reduction. This method is quick and typically performed in an outpatient setting. Bipolar probes utilize bipolar energy to coagulate the hemorrhoidal tissue, providing a precise and controlled treatment option. Cryotherapy devices apply extreme cold to the hemorrhoid, causing it to freeze and fall off. This method is less commonly used but can be effective for certain cases. Hemorrhoid laser probes use laser energy to remove or shrink hemorrhoids, offering a less invasive alternative to traditional surgery. These devices are known for their precision and reduced recovery times. Other treatment options in this market include rubber band ligation, where a rubber band is placed around the base of the hemorrhoid to cut off its blood supply, causing it to wither and fall off. Each of these devices and methods offers unique benefits and is chosen based on the specific needs and conditions of the patient. The continuous development and improvement of these tools reflect the ongoing efforts to provide better and more efficient hemorrhoid treatments.

Hospital and Clinics, Homecare, Others in the Global Diagnosis and Treatment Of Hemorrhoids Market:

The usage of the Global Diagnosis and Treatment of Hemorrhoids Market spans various settings, including hospitals and clinics, homecare, and other healthcare facilities. In hospitals and clinics, advanced diagnostic tools and treatment devices are readily available, allowing healthcare professionals to provide comprehensive care for patients with hemorrhoids. These settings offer the advantage of access to specialized medical staff and equipment, ensuring accurate diagnosis and effective treatment. Procedures such as sclerotherapy, infrared coagulation, and laser treatments are commonly performed in these environments, providing patients with a range of options based on their specific needs. Homecare solutions for hemorrhoid treatment have also gained popularity, offering patients the convenience of managing their condition in the comfort of their own homes. Over-the-counter creams, ointments, and suppositories are widely used for symptom relief, while portable devices such as cryotherapy kits and infrared coagulators are available for home use. These homecare options empower patients to take control of their treatment and manage their symptoms effectively. Other healthcare facilities, such as outpatient centers and specialized clinics, also play a significant role in the diagnosis and treatment of hemorrhoids. These facilities often provide a more focused approach, with specialized staff and equipment dedicated to treating hemorrhoidal conditions. The availability of various treatment options across different settings ensures that patients have access to the care they need, regardless of their location or circumstances. The integration of advanced technologies and innovative treatment methods in these settings highlights the dynamic nature of the Global Diagnosis and Treatment of Hemorrhoids Market, continually evolving to meet the needs of patients worldwide.

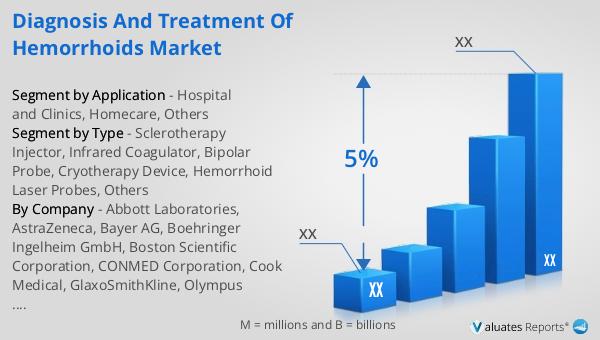

Global Diagnosis and Treatment Of Hemorrhoids Market Outlook:

The global pharmaceutical market was valued at 1475 billion USD in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. In comparison, the chemical drug market saw an increase from 1005 billion USD in 2018 to 1094 billion USD in 2022. This growth reflects the expanding demand for pharmaceutical products and the continuous advancements in drug development and healthcare solutions. The pharmaceutical market's robust growth is driven by factors such as increasing healthcare expenditures, the rising prevalence of chronic diseases, and the ongoing innovation in drug therapies. The chemical drug market, a significant segment of the broader pharmaceutical industry, also demonstrates steady growth, underscoring the importance of chemical-based medications in modern healthcare. These markets' expansion highlights the critical role of pharmaceuticals in improving patient outcomes and addressing various health challenges globally.

| Report Metric | Details |

| Report Name | Diagnosis and Treatment Of Hemorrhoids Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Abbott Laboratories, AstraZeneca, Bayer AG, Boehringer Ingelheim GmbH, Boston Scientific Corporation, CONMED Corporation, Cook Medical, GlaxoSmithKline, Olympus Corporation, Pfizer Inc., Johnson & Johnson Services, Inc, F. Hoffmann-La Roche Ltd, Novartis AG, Teva Pharmaceutical Industries Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |