What is Global Polycondensation Reactor Market?

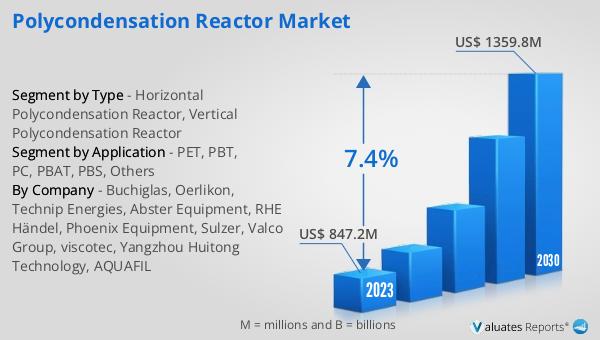

The global Polycondensation Reactor market is a specialized segment within the chemical engineering industry, focusing on the production and utilization of reactors designed for polycondensation processes. Polycondensation is a type of polymerization where monomers join together, releasing small molecules as by-products, such as water or methanol. These reactors are crucial in manufacturing various polymers and resins, which are essential components in numerous industries, including plastics, textiles, automotive, and electronics. The market for these reactors is driven by the increasing demand for high-performance materials and the need for efficient and sustainable production processes. As industries continue to innovate and seek more environmentally friendly solutions, the role of polycondensation reactors becomes even more significant. The market is characterized by advancements in reactor design, materials used for construction, and automation technologies that enhance efficiency and product quality. Companies operating in this market are continually investing in research and development to meet the evolving needs of their customers and to stay competitive. The global Polycondensation Reactor market was valued at US$ 847.2 million in 2023 and is anticipated to reach US$ 1359.8 million by 2030, witnessing a CAGR of 7.4% during the forecast period 2024-2030.

Horizontal Polycondensation Reactor, Vertical Polycondensation Reactor in the Global Polycondensation Reactor Market:

Horizontal and vertical polycondensation reactors are two primary types of reactors used in the global polycondensation reactor market, each with distinct features and applications. Horizontal polycondensation reactors are designed with a horizontal orientation, which allows for efficient mixing and heat transfer. These reactors are often used in processes where the polymerization reaction requires precise temperature control and uniform mixing. The horizontal design facilitates easy maintenance and cleaning, making it suitable for continuous production processes. On the other hand, vertical polycondensation reactors are oriented vertically, which can be advantageous for processes that rely on gravity for material flow. This design is particularly useful in batch processes where the reaction mixture needs to be drained or transferred to subsequent processing stages. Vertical reactors often have a smaller footprint compared to horizontal reactors, making them ideal for facilities with limited space. Both types of reactors are constructed using materials that can withstand high temperatures and corrosive environments, such as stainless steel or specialized alloys. The choice between horizontal and vertical reactors depends on various factors, including the specific requirements of the polycondensation process, the physical properties of the reactants and products, and the available space in the production facility. In the global polycondensation reactor market, manufacturers offer a range of reactor designs to cater to the diverse needs of different industries. Advanced features such as automated control systems, real-time monitoring, and energy-efficient designs are increasingly being incorporated into both horizontal and vertical reactors to enhance their performance and reduce operational costs. As the demand for high-quality polymers continues to grow, the market for polycondensation reactors is expected to expand, with innovations in reactor design playing a crucial role in meeting the evolving needs of the industry.

PET, PBT, PC, PBAT, PBS, Others in the Global Polycondensation Reactor Market:

The global polycondensation reactor market finds extensive usage in the production of various polymers, including PET, PBT, PC, PBAT, PBS, and others. Polyethylene terephthalate (PET) is one of the most common polymers produced using polycondensation reactors. PET is widely used in the packaging industry, particularly for making bottles and containers due to its excellent strength, clarity, and barrier properties. Polybutylene terephthalate (PBT) is another important polymer produced using these reactors. PBT is known for its high mechanical strength, thermal stability, and resistance to chemicals, making it suitable for applications in the automotive and electronics industries. Polycarbonate (PC) is a high-performance polymer produced through polycondensation, known for its exceptional impact resistance, transparency, and thermal stability. PC is used in a variety of applications, including optical discs, automotive components, and electronic devices. Polybutylene adipate terephthalate (PBAT) is a biodegradable polymer produced using polycondensation reactors. PBAT is used in the production of compostable bags, agricultural films, and other environmentally friendly products. Polybutylene succinate (PBS) is another biodegradable polymer produced through polycondensation. PBS is used in packaging, agricultural applications, and disposable products due to its biodegradability and good mechanical properties. In addition to these specific polymers, polycondensation reactors are also used to produce a wide range of other polymers and resins that find applications in various industries. The versatility of polycondensation reactors in producing different types of polymers makes them a critical component in the global polymer industry. As the demand for high-performance and sustainable materials continues to rise, the usage of polycondensation reactors in the production of these polymers is expected to grow, driving the expansion of the global polycondensation reactor market.

Global Polycondensation Reactor Market Outlook:

The global Polycondensation Reactor market was valued at US$ 847.2 million in 2023 and is anticipated to reach US$ 1359.8 million by 2030, witnessing a CAGR of 7.4% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced polycondensation reactors across various industries. The market's expansion is driven by the need for efficient and sustainable production processes, as well as the growing demand for high-performance polymers and resins. Companies operating in this market are investing in research and development to innovate and improve reactor designs, incorporating advanced features such as automated control systems and real-time monitoring. These advancements enhance the efficiency and quality of the production processes, making polycondensation reactors more attractive to manufacturers. The market's growth is also supported by the rising awareness of environmental sustainability and the need for eco-friendly materials. As industries continue to seek solutions that reduce their environmental impact, the demand for polycondensation reactors capable of producing biodegradable and recyclable polymers is expected to increase. Overall, the global Polycondensation Reactor market is poised for significant growth, driven by technological advancements, increasing demand for high-quality polymers, and the push for sustainable production practices.

| Report Metric | Details |

| Report Name | Polycondensation Reactor Market |

| Accounted market size in 2023 | US$ 847.2 million |

| Forecasted market size in 2030 | US$ 1359.8 million |

| CAGR | 7.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Buchiglas, Oerlikon, Technip Energies, Abster Equipment, RHE Händel, Phoenix Equipment, Sulzer, Valco Group, viscotec, Yangzhou Huitong Technology, AQUAFIL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |