What is Global Clinical Trial Imaging Service Market?

The Global Clinical Trial Imaging Service Market is a specialized sector that focuses on providing imaging services such as MRI, CT scans, and PET scans, which are crucial in clinical trials. These services help in the accurate assessment of how a new drug or a medical device affects the human body. The importance of these imaging services has grown significantly as they offer precise and detailed insights into the efficacy and safety of new pharmaceutical products or medical devices before they are launched in the market. This market plays a pivotal role in the development of new medical treatments by ensuring that the clinical trials are conducted efficiently and meet the regulatory standards set by health authorities around the world. With the advancement in medical technology and the increasing demand for new healthcare solutions, the Global Clinical Trial Imaging Service Market is witnessing substantial growth. This sector is essential for pharmaceutical companies, biotechnology firms, and medical device manufacturers who are constantly striving to innovate and bring new products to the market that can improve patient care and treatment outcomes.

In-house Imaging Service, Central Imaging Service in the Global Clinical Trial Imaging Service Market:

In the realm of the Global Clinical Trial Imaging Service Market, two primary service models stand out: In-house Imaging Services and Central Imaging Services. In-house Imaging Services refer to the scenario where pharmaceutical, biotechnology companies, or clinical research organizations manage and conduct imaging aspects of clinical trials within their own facilities, utilizing their own resources and personnel. This model allows for direct control over the imaging process, potentially leading to quicker decision-making and adjustments. However, it requires significant investment in equipment, technology, and skilled personnel. On the other hand, Central Imaging Services are provided by specialized companies that focus solely on delivering imaging services for clinical trials. This model offers a standardized, unbiased approach to image analysis, which can enhance the reliability and comparability of data across different trial sites. Central Imaging Services can also offer advanced technologies and expertise that might not be available in-house, along with scalability and flexibility to handle varying volumes of work. This approach can lead to cost efficiencies and a reduction in the burden on the trial sponsor's resources. Both service models play crucial roles in the Global Clinical Trial Imaging Service Market, each offering distinct advantages that can suit different needs and strategies of trial sponsors. The choice between in-house and central imaging services depends on various factors, including the complexity of the trial, the specific imaging requirements, budget constraints, and the strategic priorities of the organizations involved.

Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Research Institutes, Others in the Global Clinical Trial Imaging Service Market:

The Global Clinical Trial Imaging Service Market finds its application across a diverse range of sectors including Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Research Institutes, and others. In Pharmaceutical Companies, imaging services are crucial for drug development processes, especially in the phases of clinical trials where the safety and efficacy of new drugs are tested. These services provide valuable data that help in understanding the drug's impact on the body, thereby facilitating regulatory approvals. Biotechnology Companies, often working on cutting-edge therapies, rely on advanced imaging services to visualize the biological processes and the effects of their products at a cellular or molecular level, which is critical for the development of targeted therapies. Medical Device Manufacturers use clinical trial imaging services to demonstrate the functionality and safety of new medical devices, such as implants or diagnostic equipment, ensuring they meet the required standards for market approval. Research Institutes utilize these services for academic and clinical research, contributing to the advancement of medical science by exploring new treatments and understanding diseases better. Other sectors, including contract research organizations and healthcare institutions, also leverage these imaging services to support their clinical trials and research projects. The versatility and critical nature of clinical trial imaging services underscore their importance across the entire spectrum of healthcare and medical research, facilitating the development of innovative solutions that can advance patient care.

Global Clinical Trial Imaging Service Market Outlook:

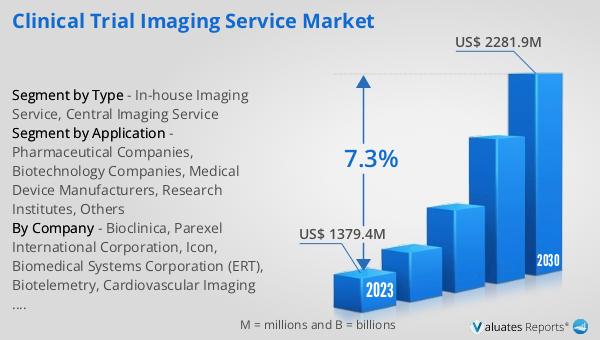

The market outlook for the Global Clinical Trial Imaging Service Market reveals a promising trajectory. As of 2023, the market was valued at approximately $1379.4 million and is projected to escalate to around $2281.9 million by 2030, marking a Compound Annual Growth Rate (CAGR) of 7.3% during the forecast period from 2024 to 2030. This growth is indicative of the increasing reliance on imaging services in clinical trials across the globe. The market is somewhat concentrated, with the top five companies accounting for about 40% of the market share, highlighting the presence of key players who dominate the sector. Geographically, North America emerges as the largest market, holding about a 33% share, which can be attributed to the advanced healthcare infrastructure and the high number of clinical trials conducted in the region. Europe and Asia Pacific follow closely, each accounting for approximately 27% of the market share, driven by the growing research and development activities in these regions. When it comes to the types of services provided, central imaging services dominate the market, representing about 70% of the product segment. This dominance underscores the critical role that centralized imaging plays in ensuring standardized, high-quality imaging data across multi-site trials, which is essential for the successful development and approval of new medical treatments.

| Report Metric | Details |

| Report Name | Clinical Trial Imaging Service Market |

| Accounted market size in 2023 | US$ 1379.4 million |

| Forecasted market size in 2030 | US$ 2281.9 million |

| CAGR | 7.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bioclinica, Parexel International Corporation, Icon, Biomedical Systems Corporation (ERT), Biotelemetry, Cardiovascular Imaging Technologies, Intrinsic Imaging, Ixico, Radiant Sage, Worldcare Clinical, Micron, Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |