What is Global Kanban Software Market?

The Global Kanban Software Market is a dynamic and evolving sector that focuses on providing digital solutions to streamline workflow management and enhance productivity across various industries. Kanban, a methodology originating from Japan, emphasizes visualizing work, limiting work-in-progress, and maximizing efficiency. The software market for Kanban tools has grown significantly as businesses increasingly seek to optimize their processes and improve team collaboration. These tools offer features such as task boards, real-time updates, and analytics, which help organizations manage projects more effectively. The market caters to a wide range of industries, including manufacturing, IT, healthcare, and education, among others. As companies continue to embrace digital transformation, the demand for Kanban software is expected to rise, driven by the need for efficient project management solutions that can adapt to the changing business landscape. The market is characterized by a mix of established players and emerging startups, each offering unique features and capabilities to meet the diverse needs of their clients. Overall, the Global Kanban Software Market plays a crucial role in helping organizations achieve operational excellence and maintain a competitive edge in today's fast-paced business environment.

Cloud-based, On Premise in the Global Kanban Software Market:

In the Global Kanban Software Market, solutions are typically categorized into two main deployment models: cloud-based and on-premise. Cloud-based Kanban software is hosted on the vendor's servers and accessed via the internet, offering several advantages such as scalability, flexibility, and cost-effectiveness. This model allows businesses to access their Kanban tools from anywhere, at any time, making it ideal for organizations with remote teams or those that require a high degree of mobility. Cloud-based solutions often come with automatic updates and maintenance, reducing the burden on internal IT teams and ensuring that users always have access to the latest features and security enhancements. Additionally, cloud-based Kanban software typically operates on a subscription-based pricing model, which can be more budget-friendly for small and medium-sized businesses (SMBs) that may not have the resources to invest in expensive infrastructure. On the other hand, on-premise Kanban software is installed and run on the organization's own servers, providing greater control over data security and customization. This model is often preferred by large enterprises or industries with stringent regulatory requirements, as it allows them to maintain complete ownership of their data and tailor the software to their specific needs. On-premise solutions can be more costly upfront, as they require investment in hardware, software licenses, and IT personnel to manage and maintain the system. However, for organizations that prioritize data privacy and have the necessary resources, on-premise Kanban software can offer a level of security and customization that cloud-based solutions may not provide. Both cloud-based and on-premise Kanban software have their own set of benefits and challenges, and the choice between the two largely depends on the organization's specific needs, budget, and IT infrastructure. For instance, a company with a global presence and a distributed workforce may find cloud-based solutions more advantageous due to their accessibility and ease of collaboration. Conversely, a company operating in a highly regulated industry, such as finance or healthcare, may opt for on-premise solutions to ensure compliance with data protection laws and industry standards. As the Global Kanban Software Market continues to grow, vendors are increasingly offering hybrid solutions that combine the best of both worlds. These hybrid models allow organizations to leverage the scalability and flexibility of the cloud while maintaining control over sensitive data through on-premise deployments. This approach enables businesses to adapt to changing needs and regulatory environments while optimizing their workflow management processes. In conclusion, the choice between cloud-based and on-premise Kanban software depends on various factors, including the organization's size, industry, and specific requirements. Both models offer unique advantages and can significantly enhance productivity and efficiency when implemented effectively. As technology continues to evolve, the Global Kanban Software Market is likely to see further innovations and developments, providing businesses with even more options to optimize their operations and achieve their strategic goals.

Large Enterprise, SMBs in the Global Kanban Software Market:

The usage of Global Kanban Software Market solutions varies significantly between large enterprises and small to medium-sized businesses (SMBs), each with distinct needs and operational challenges. Large enterprises often have complex workflows and require robust project management tools to coordinate activities across multiple departments and locations. Kanban software helps these organizations visualize their processes, identify bottlenecks, and improve overall efficiency. By providing a clear overview of tasks and their progress, Kanban tools enable large enterprises to allocate resources more effectively, prioritize work, and ensure timely delivery of projects. Additionally, the analytics and reporting features offered by many Kanban solutions allow large enterprises to gain valuable insights into their operations, facilitating data-driven decision-making and continuous improvement. For SMBs, Kanban software offers a cost-effective solution to manage projects and streamline operations. These businesses often operate with limited resources and need tools that are easy to implement and use. Kanban software provides SMBs with a simple yet powerful way to organize tasks, track progress, and collaborate with team members. The visual nature of Kanban boards makes it easy for SMBs to understand their workflow and identify areas for improvement. Moreover, many Kanban solutions offer scalable pricing models, allowing SMBs to start with basic features and expand their capabilities as their needs grow. This flexibility is particularly beneficial for SMBs looking to optimize their operations without incurring significant costs. Both large enterprises and SMBs benefit from the collaborative features of Kanban software, which facilitate communication and teamwork. By providing a centralized platform for task management, Kanban tools help teams stay aligned and focused on their goals. This is especially important in today's fast-paced business environment, where effective collaboration can be a key differentiator. Furthermore, the ability to integrate Kanban software with other tools and systems, such as customer relationship management (CRM) and enterprise resource planning (ERP) systems, enhances its value for both large enterprises and SMBs. This integration allows organizations to create a seamless workflow and ensure that all relevant information is readily accessible to team members. In summary, the Global Kanban Software Market offers valuable solutions for both large enterprises and SMBs, helping them optimize their operations and improve productivity. While large enterprises benefit from the advanced features and scalability of Kanban tools, SMBs appreciate their simplicity and cost-effectiveness. As businesses continue to face increasing pressure to deliver results quickly and efficiently, the adoption of Kanban software is likely to grow, providing organizations with the tools they need to succeed in a competitive marketplace.

Global Kanban Software Market Outlook:

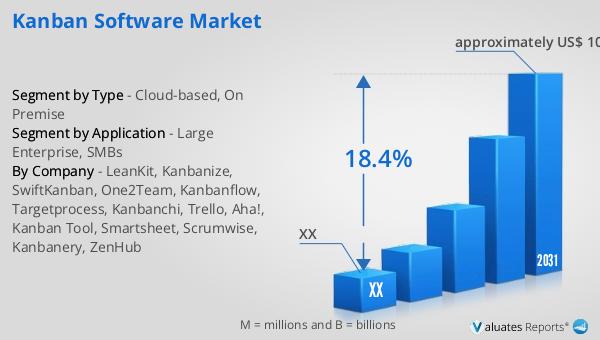

In 2024, the global market size of Kanban Software was valued at approximately US$ 328 million, with projections indicating a significant increase to around US$ 1054 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 18.4% during the forecast period from 2025 to 2031. North America holds the largest share of the Kanban Software market, accounting for about 55% of the total market. Europe follows with a 25% market share. The industry is dominated by key players such as LeanKit, Kanbanize, SwiftKanban, One2Team, and Trello, which collectively hold approximately 75% of the market share. These companies have established themselves as leaders in the field by offering innovative solutions that cater to the diverse needs of businesses across various industries. As the demand for efficient project management tools continues to rise, these manufacturers are well-positioned to capitalize on the growing market opportunities. The competitive landscape of the Kanban Software market is characterized by a mix of established players and emerging startups, each striving to offer unique features and capabilities to attract and retain customers. As businesses increasingly recognize the value of Kanban software in enhancing productivity and streamlining operations, the market is poised for continued growth and innovation.

| Report Metric | Details |

| Report Name | Kanban Software Market |

| Forecasted market size in 2031 | approximately US$ 1054 million |

| CAGR | 18.4% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | LeanKit, Kanbanize, SwiftKanban, One2Team, Kanbanflow, Targetprocess, Kanbanchi, Trello, Aha!, Kanban Tool, Smartsheet, Scrumwise, Kanbanery, ZenHub |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |