What is Global Black Rice Market?

The global black rice market is an intriguing segment of the broader rice industry, characterized by its unique color, nutritional benefits, and cultural significance. Black rice, often referred to as "forbidden rice," is a variety of rice that is rich in anthocyanins, the same antioxidants found in blueberries and blackberries, which give it its distinctive dark hue. This type of rice is not only visually appealing but also packed with health benefits, including high levels of fiber, iron, and vitamin E. Traditionally, black rice was reserved for Chinese royalty due to its rarity and nutritional value, but today it is gaining popularity worldwide as a superfood. The market for black rice is expanding as consumers become more health-conscious and seek out nutrient-dense foods. This growth is also driven by the increasing demand for organic and natural food products, as black rice is often grown using sustainable farming practices. As a result, the global black rice market is poised for significant growth, with more people incorporating this nutritious grain into their diets. The market's expansion is further supported by the rising awareness of the health benefits associated with black rice, making it a staple in health-conscious households and gourmet kitchens alike.

Indonesian Black Rice, Philippine Balatinaw Black Rice, Thai Jasmine Black Rice, Others in the Global Black Rice Market:

Indonesian black rice, known for its nutty flavor and chewy texture, is a staple in Indonesian cuisine and is often used in traditional dishes such as black rice pudding. This variety of black rice is typically grown in the volcanic soils of Bali, which are rich in minerals, contributing to its unique taste and nutritional profile. Indonesian black rice is often cultivated using traditional methods, which not only preserve its natural qualities but also support local farming communities. In the global black rice market, Indonesian black rice is valued for its authenticity and cultural heritage, making it a popular choice among consumers seeking an exotic and nutritious grain. Philippine Balatinaw black rice, on the other hand, is a heritage variety that is deeply rooted in the agricultural traditions of the Philippines. Known for its aromatic scent and slightly sweet flavor, Balatinaw black rice is often used in Filipino desserts and festive dishes. This variety is grown in the mountainous regions of the Philippines, where indigenous farming practices have been passed down through generations. The global market for Balatinaw black rice is driven by its unique flavor profile and cultural significance, appealing to consumers who appreciate traditional and artisanal food products. Thai Jasmine black rice, also known as black jasmine rice, is a fragrant variety that combines the aromatic qualities of jasmine rice with the nutritional benefits of black rice. This variety is popular in Thai cuisine, where it is used in both savory and sweet dishes. Thai Jasmine black rice is often grown in the fertile plains of Thailand, where the climate and soil conditions are ideal for rice cultivation. In the global black rice market, Thai Jasmine black rice is sought after for its distinctive aroma and versatility in cooking, making it a favorite among chefs and home cooks alike. Other varieties of black rice, such as Chinese black rice and Indian black rice, also contribute to the diversity of the global black rice market. Chinese black rice, often referred to as "emperor's rice," is known for its rich flavor and high nutritional content, while Indian black rice, also known as "chak-hao," is prized for its medicinal properties and is often used in traditional Ayurvedic medicine. These varieties, along with others, add to the rich tapestry of the global black rice market, offering consumers a wide range of options to explore and enjoy. As the demand for black rice continues to grow, producers are focusing on sustainable farming practices and innovative marketing strategies to meet the needs of health-conscious consumers. The global black rice market is a dynamic and evolving segment, reflecting the diverse cultural and culinary traditions associated with this ancient grain.

Household, Commercial in the Global Black Rice Market:

The usage of black rice in households and commercial settings is diverse and multifaceted, reflecting its versatility and nutritional benefits. In households, black rice is increasingly being incorporated into everyday meals as a healthy alternative to white or brown rice. Its high fiber content and rich antioxidant profile make it an attractive option for health-conscious consumers looking to improve their diet. Black rice can be used in a variety of dishes, from salads and stir-fries to desserts and breakfast bowls. Its unique color and nutty flavor add a gourmet touch to home-cooked meals, making it a favorite among food enthusiasts and home chefs. Additionally, black rice is often used in gluten-free and vegan recipes, catering to the dietary preferences of a growing number of consumers. In commercial settings, black rice is gaining popularity in the foodservice industry, where it is used by chefs and restaurateurs to create innovative and visually appealing dishes. Its striking appearance and health benefits make it a popular choice for upscale restaurants and catering services looking to offer unique and nutritious menu options. Black rice is also being used in the production of packaged food products, such as rice cakes, snacks, and ready-to-eat meals, catering to the convenience-driven consumer market. The commercial demand for black rice is further fueled by the growing trend of plant-based and functional foods, as consumers seek out products that offer both taste and health benefits. In addition to its culinary uses, black rice is also being explored for its potential applications in the nutraceutical and cosmetic industries. Its high antioxidant content makes it a valuable ingredient in health supplements and skincare products, where it is used for its anti-aging and skin-enhancing properties. As the global black rice market continues to expand, the versatility and health benefits of this ancient grain are driving its adoption across various sectors, from household kitchens to commercial enterprises. The increasing awareness of the nutritional advantages of black rice, coupled with its unique culinary attributes, is positioning it as a staple ingredient in both traditional and modern cuisines.

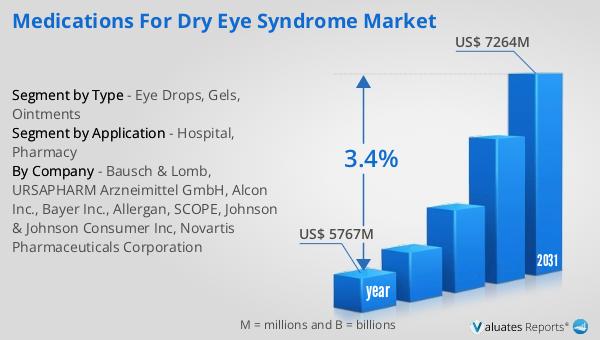

Global Black Rice Market Outlook:

The global market for black rice was valued at $185 million in 2024, and it is anticipated to grow significantly, reaching an estimated size of $259 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.0% over the forecast period. The increasing demand for black rice can be attributed to its rising popularity as a superfood, driven by its rich nutritional profile and health benefits. Consumers are becoming more health-conscious and are actively seeking out foods that offer both taste and nutritional value, which is contributing to the market's expansion. Additionally, the growing trend of organic and natural food products is supporting the demand for black rice, as it is often cultivated using sustainable farming practices. The market's growth is also being fueled by the increasing awareness of the health benefits associated with black rice, such as its high antioxidant content and potential to support heart health and weight management. As more consumers incorporate black rice into their diets, the market is expected to continue its upward trajectory, offering opportunities for producers and retailers to capitalize on this growing trend. The global black rice market is poised for significant growth, reflecting the changing consumer preferences and the increasing demand for nutrient-dense and health-promoting foods.

| Report Metric | Details |

| Report Name | Black Rice Market |

| Accounted market size in year | US$ 185 million |

| Forecasted market size in 2031 | US$ 259 million |

| CAGR | 5.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ROYAL NUT COMPANY, The Natural Rice Co, PraTithi Organic Foods, Lotus Food Inc, Greenpower Nanohana co.ltd., Pristine, Monsoon Valley Agro Exports, Shiyue Daotian Group, Zhejiang Wufangzhai Industry Co.,Ltd., Laishui County Jingu Cereal&Oil Foodstuff Co.,Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |