What is Global Non-corticosteroid Immunomodulator Market?

The Global Non-corticosteroid Immunomodulator Market refers to the segment of the pharmaceutical industry that focuses on drugs designed to modulate the immune system without using corticosteroids. These medications are crucial in treating various autoimmune diseases and conditions where the immune system needs regulation. Unlike corticosteroids, which can have significant side effects with long-term use, non-corticosteroid immunomodulators offer a targeted approach to managing immune responses. This market includes a range of drug classes, each with unique mechanisms of action, aimed at reducing inflammation and preventing the immune system from attacking the body's own tissues. The demand for these drugs is driven by the increasing prevalence of autoimmune diseases, advancements in biotechnology, and a growing understanding of the immune system's role in various health conditions. As research continues to evolve, the market is expected to expand, offering new and improved treatment options for patients worldwide. The focus on non-corticosteroid options highlights the ongoing efforts to provide safer, more effective therapies with fewer side effects, addressing a critical need in the management of chronic and debilitating diseases.

Calcineurin Inhibitors, Antiproliferative Agents, mTOR Inhibitors, IMDH Inhibitors, Others in the Global Non-corticosteroid Immunomodulator Market:

Calcineurin inhibitors are a class of drugs that play a pivotal role in the Global Non-corticosteroid Immunomodulator Market. These drugs work by inhibiting the activity of calcineurin, a protein phosphatase involved in activating T-cells of the immune system. By blocking this pathway, calcineurin inhibitors effectively reduce the immune response, making them invaluable in preventing organ transplant rejection and treating autoimmune diseases. Common examples include cyclosporine and tacrolimus, which are widely used in clinical settings. Antiproliferative agents, on the other hand, target the proliferation of immune cells. These drugs are crucial in conditions where the immune system is overactive, such as in organ transplantation, where they help prevent the rejection of transplanted organs by inhibiting the growth of T and B lymphocytes. Mycophenolate mofetil is a well-known antiproliferative agent used in this context. mTOR inhibitors, such as sirolimus and everolimus, are another critical component of this market. They work by inhibiting the mammalian target of rapamycin (mTOR) pathway, which is essential for cell growth and proliferation. By targeting this pathway, mTOR inhibitors help control the immune response, making them useful in both organ transplantation and certain cancers. IMDH inhibitors, like mycophenolic acid, specifically target the enzyme inosine monophosphate dehydrogenase (IMDH), which is crucial for the proliferation of lymphocytes. By inhibiting this enzyme, these drugs effectively suppress the immune response, providing another tool in the management of autoimmune diseases and transplant rejection. The "Others" category in the Global Non-corticosteroid Immunomodulator Market includes a variety of drugs with unique mechanisms of action that do not fit neatly into the other categories. These may include newer biologics and small molecules that offer innovative approaches to immune modulation. As research in immunology advances, this category is expected to grow, incorporating cutting-edge therapies that provide more personalized and effective treatment options for patients. Each of these drug classes contributes to the overall landscape of the Global Non-corticosteroid Immunomodulator Market, offering diverse options for clinicians to tailor treatments to individual patient needs. The development and refinement of these drugs continue to be a focus of pharmaceutical research, driven by the need for safer, more effective therapies for managing complex immune-mediated conditions.

Organ Transplantation, Atopic Dermatitis, Crohn's Disease, Ulcerative Colitis, Others in the Global Non-corticosteroid Immunomodulator Market:

The Global Non-corticosteroid Immunomodulator Market finds its application in several critical areas of medicine, each with unique challenges and treatment requirements. In organ transplantation, these drugs are indispensable. They help prevent the body's immune system from rejecting the transplanted organ, a common complication that can lead to organ failure. Calcineurin inhibitors, antiproliferative agents, and mTOR inhibitors are commonly used in this context, providing a multi-faceted approach to immune suppression that enhances the success rates of transplants. In the realm of dermatology, non-corticosteroid immunomodulators are used to treat atopic dermatitis, a chronic inflammatory skin condition characterized by itchy and inflamed skin. These drugs help modulate the immune response, reducing inflammation and providing relief to patients who may not respond well to traditional corticosteroid treatments. Inflammatory bowel diseases, such as Crohn's disease and ulcerative colitis, also benefit from these medications. These conditions involve chronic inflammation of the gastrointestinal tract, leading to severe symptoms and complications. Non-corticosteroid immunomodulators help manage these diseases by targeting specific pathways involved in the inflammatory process, thereby reducing symptoms and improving the quality of life for patients. Beyond these specific conditions, the Global Non-corticosteroid Immunomodulator Market also addresses a range of other autoimmune and inflammatory diseases. These may include rheumatoid arthritis, lupus, and multiple sclerosis, where the immune system mistakenly attacks healthy tissues. By offering targeted immune modulation, these drugs provide a crucial tool in managing these complex diseases, reducing symptoms, and preventing long-term damage. The versatility and effectiveness of non-corticosteroid immunomodulators make them a cornerstone in the treatment of various immune-mediated conditions, highlighting their importance in modern medicine.

Global Non-corticosteroid Immunomodulator Market Outlook:

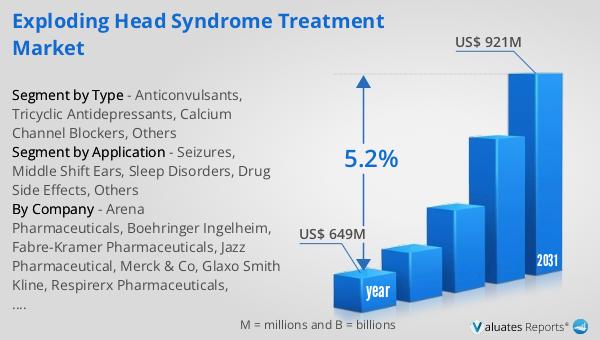

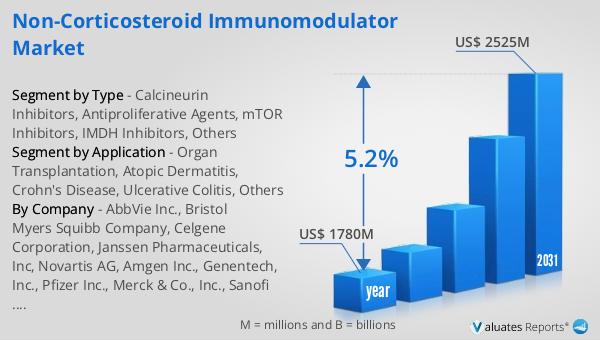

The global market for Non-corticosteroid Immunomodulators was valued at $1,780 million in 2024, with projections indicating a growth to $2,525 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.2% over the forecast period. The increasing demand for these drugs is driven by the rising prevalence of autoimmune diseases and the need for safer, more effective treatment options. As the understanding of the immune system and its role in various diseases continues to evolve, the market for non-corticosteroid immunomodulators is expected to expand, offering new opportunities for pharmaceutical companies and healthcare providers. The focus on non-corticosteroid options reflects a broader trend in medicine towards more targeted and personalized therapies, addressing the unique needs of individual patients. This market growth is also supported by advancements in biotechnology and drug development, which are enabling the creation of more sophisticated and effective immunomodulatory drugs. As research continues to uncover new insights into the immune system, the potential for innovation in this market remains high, promising improved outcomes for patients and a more sustainable approach to managing chronic and complex diseases.

| Report Metric | Details |

| Report Name | Non-corticosteroid Immunomodulator Market |

| Accounted market size in year | US$ 1780 million |

| Forecasted market size in 2031 | US$ 2525 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | AbbVie Inc., Bristol Myers Squibb Company, Celgene Corporation, Janssen Pharmaceuticals, Inc, Novartis AG, Amgen Inc., Genentech, Inc., Pfizer Inc., Merck & Co., Inc., Sanofi S.A., Eli Lilly and Company, GlaxoSmithKline PLC, Mylan Laboratories Inc., Glenmark Pharmaceuticals, Inc., Zydus Cadila, Takeda Pharmaceutical Company Limited, AstraZeneca PLC, Gilead Sciences, Inc., Boehringer Ingelheim GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |