What is Weapons Carriage and Release System - Global Market?

The Weapons Carriage and Release System is a crucial component in the global defense market, playing a vital role in the deployment of various munitions from military aircraft and naval vessels. This system is designed to securely carry and accurately release weapons such as missiles, bombs, rockets, and torpedoes, ensuring they reach their intended targets with precision. The global market for these systems is driven by the increasing demand for advanced military capabilities and the modernization of defense forces worldwide. As nations strive to enhance their defense mechanisms, the need for reliable and efficient weapons carriage and release systems becomes paramount. These systems are not only essential for offensive operations but also for maintaining strategic deterrence. The market is characterized by technological advancements, with manufacturers focusing on developing systems that offer greater accuracy, reliability, and ease of integration with various platforms. As a result, the global market for weapons carriage and release systems is poised for significant growth, driven by the continuous evolution of military strategies and the need for advanced defense solutions.

Torpedoes, Rockets, Missiles, Bombs in the Weapons Carriage and Release System - Global Market:

Torpedoes, rockets, missiles, and bombs are integral components of modern military arsenals, each serving distinct roles in warfare and defense strategies. In the context of the Weapons Carriage and Release System - Global Market, these munitions are carried and deployed with precision and reliability, ensuring effective engagement with targets. Torpedoes, primarily used by naval forces, are self-propelled underwater missiles designed to target and destroy enemy submarines and ships. The carriage and release systems for torpedoes are engineered to withstand harsh marine environments, ensuring that these weapons can be launched accurately from submarines and surface vessels. Rockets, on the other hand, are unguided weapons that rely on their propulsion system to reach targets. They are often used for close-range attacks and are carried by aircraft and ground vehicles. The carriage and release systems for rockets are designed to handle the high-speed deployment and ensure stability during launch. Missiles, which can be guided or unguided, are versatile weapons used by both air and naval forces. They are equipped with advanced guidance systems that allow them to track and engage moving targets with high precision. The carriage and release systems for missiles are sophisticated, incorporating technologies that ensure seamless integration with the aircraft or vessel's targeting systems. Bombs, typically used by air forces, are explosive devices designed to cause maximum damage to enemy infrastructure and personnel. The carriage and release systems for bombs are crucial for ensuring that these weapons are deployed accurately, minimizing collateral damage and maximizing operational effectiveness. In the global market, the demand for advanced carriage and release systems for these munitions is driven by the need for enhanced military capabilities and the modernization of defense forces. Manufacturers are focusing on developing systems that offer greater accuracy, reliability, and ease of integration with various platforms. As military strategies evolve, the role of torpedoes, rockets, missiles, and bombs in defense operations continues to grow, underscoring the importance of efficient and reliable weapons carriage and release systems.

Navy, Air Force, Other in the Weapons Carriage and Release System - Global Market:

The usage of Weapons Carriage and Release Systems in the global market spans across various branches of the military, including the Navy, Air Force, and other defense sectors. In the Navy, these systems are essential for the deployment of torpedoes, missiles, and other munitions from submarines and surface vessels. The harsh marine environment requires robust and reliable systems that can withstand extreme conditions and ensure accurate targeting. The Navy relies on these systems to maintain strategic deterrence and engage enemy targets effectively. In the Air Force, weapons carriage and release systems are critical for the deployment of bombs, missiles, and rockets from aircraft. These systems are designed to integrate seamlessly with the aircraft's targeting and guidance systems, ensuring precision and reliability during combat operations. The Air Force uses these systems to maintain air superiority and conduct strategic strikes against enemy targets. In addition to the Navy and Air Force, other defense sectors also utilize weapons carriage and release systems for various applications. Ground forces, for example, use these systems to deploy rockets and missiles from ground vehicles, providing them with the capability to engage enemy targets from a distance. The global market for weapons carriage and release systems is driven by the need for advanced military capabilities and the modernization of defense forces. As military strategies evolve, the demand for reliable and efficient systems continues to grow, underscoring their importance in modern warfare. Manufacturers are focusing on developing systems that offer greater accuracy, reliability, and ease of integration with various platforms, ensuring that defense forces can effectively engage enemy targets and maintain strategic deterrence.

Weapons Carriage and Release System - Global Market Outlook:

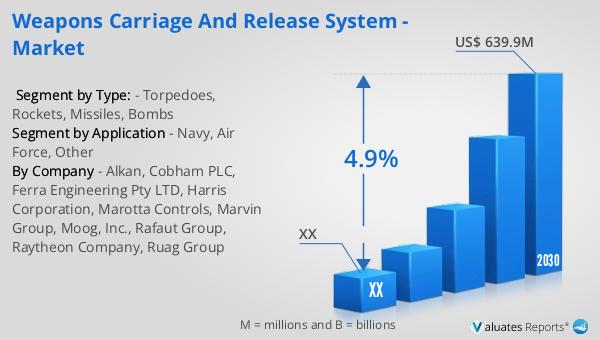

In 2023, the global market for Weapons Carriage and Release Systems was valued at approximately $454.6 million, with projections indicating a growth to $639.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.9% during the forecast period from 2024 to 2030. The United States holds the largest share of this market, accounting for nearly 58% of global consumption, followed by Europe, which represents 21% of the market. This significant market presence in the U.S. can be attributed to the country's substantial defense budget and continuous investment in advanced military technologies. Leading companies in this industry, such as Cobham, Harris Corporation, AVIC, Raytheon, Moog, Ultra Electronics, and Circor Aerospace & Defense, collectively dominate the market with an 81% share. These companies are at the forefront of innovation, developing cutting-edge systems that meet the evolving needs of modern defense forces. Their focus on research and development, coupled with strategic partnerships and collaborations, has enabled them to maintain a competitive edge in the market. As the demand for advanced weapons carriage and release systems continues to grow, these industry leaders are well-positioned to capitalize on emerging opportunities and drive further market expansion.

| Report Metric | Details |

| Report Name | Weapons Carriage and Release System - Market |

| Forecasted market size in 2030 | US$ 639.9 million |

| CAGR | 4.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Alkan, Cobham PLC, Ferra Engineering Pty LTD, Harris Corporation, Marotta Controls, Marvin Group, Moog, Inc., Rafaut Group, Raytheon Company, Ruag Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |