What is Oral Anti-allergic Drugs - Global Market?

Oral anti-allergic drugs are a crucial segment of the global pharmaceutical market, designed to alleviate symptoms associated with allergic reactions. These medications work by targeting the body's immune response to allergens, which can include pollen, dust, pet dander, and certain foods. The global market for these drugs is driven by the increasing prevalence of allergies worldwide, which affects millions of people and can significantly impact their quality of life. Oral anti-allergic drugs are available in various forms, including tablets, capsules, and liquid formulations, making them accessible and convenient for patients. The market is characterized by a wide range of products, from over-the-counter options to prescription medications, catering to different levels of allergy severity. As awareness of allergies and their impact grows, so does the demand for effective treatments, driving innovation and competition among pharmaceutical companies. This market is also influenced by factors such as regulatory approvals, healthcare infrastructure, and consumer preferences, which vary across different regions. Overall, the oral anti-allergic drugs market is a dynamic and essential component of the healthcare industry, providing relief to allergy sufferers and contributing to the broader goal of improving public health.

Antihistamine Drugs, Allergic Mediator Release Agent, Immunosuppressant Drugs in the Oral Anti-allergic Drugs - Global Market:

Antihistamine drugs are a cornerstone of oral anti-allergic treatments, primarily used to counteract the effects of histamines in the body. Histamines are chemicals released during an allergic reaction, leading to symptoms such as itching, swelling, and runny nose. Antihistamines work by blocking the receptors that histamines bind to, thereby reducing these symptoms. They are available in both first-generation and second-generation forms. First-generation antihistamines, like diphenhydramine, are effective but often cause drowsiness, limiting their use for some patients. Second-generation antihistamines, such as loratadine and cetirizine, are less likely to cause sedation and are preferred for long-term management of allergies. These drugs are widely used due to their efficacy and relatively low side effects, making them a popular choice for both healthcare providers and patients. Allergic mediator release agents, on the other hand, focus on preventing the release of various chemicals that trigger allergic reactions. These drugs are particularly useful in managing conditions like asthma and chronic urticaria, where controlling the release of mediators can significantly improve patient outcomes. By stabilizing mast cells and other immune cells, these agents help in reducing the frequency and severity of allergic episodes. Immunosuppressant drugs, although not the first line of treatment for allergies, play a role in managing severe allergic conditions that do not respond to conventional therapies. These drugs work by dampening the overall immune response, thereby reducing the body's reaction to allergens. They are typically used in cases of severe eczema or allergic asthma, where other treatments have failed. However, due to their potential side effects, including increased susceptibility to infections, their use is carefully monitored by healthcare professionals. The global market for these oral anti-allergic drugs is shaped by ongoing research and development efforts aimed at improving efficacy and safety profiles. Pharmaceutical companies are investing in new formulations and delivery methods to enhance patient compliance and outcomes. Additionally, the market is influenced by regulatory frameworks that govern the approval and distribution of these drugs, ensuring that they meet safety and efficacy standards. As the understanding of allergy mechanisms advances, there is potential for the development of more targeted therapies that address the underlying causes of allergic reactions rather than just the symptoms. This could lead to a shift in the market landscape, with new entrants and innovative products gaining traction. Overall, the oral anti-allergic drugs market is a vital component of the healthcare industry, addressing a significant and growing need for effective allergy management solutions.

Hospital Pharmacies, Retail Pharmacies, Online Pharmacies in the Oral Anti-allergic Drugs - Global Market:

The usage of oral anti-allergic drugs spans various distribution channels, including hospital pharmacies, retail pharmacies, and online pharmacies, each playing a crucial role in ensuring patient access to these medications. Hospital pharmacies are integral in providing oral anti-allergic drugs to patients who are admitted for severe allergic reactions or related conditions. These pharmacies ensure that patients receive the appropriate medication as part of their treatment regimen, often in conjunction with other therapies. Hospital pharmacists work closely with healthcare providers to manage and monitor patient responses to these drugs, adjusting dosages as needed to optimize outcomes. This setting is particularly important for patients with complex medical histories or those who require close supervision during treatment. Retail pharmacies, on the other hand, serve as the primary point of access for most patients seeking oral anti-allergic drugs. These pharmacies offer a wide range of over-the-counter and prescription medications, making it convenient for patients to obtain the necessary treatments. Pharmacists in retail settings provide valuable guidance on the selection and use of these drugs, helping patients understand potential side effects and interactions with other medications. The accessibility and convenience of retail pharmacies make them a popular choice for individuals managing mild to moderate allergies. Online pharmacies have emerged as a growing distribution channel for oral anti-allergic drugs, offering patients the convenience of ordering medications from the comfort of their homes. This option is particularly appealing to those with busy schedules or limited mobility, as it eliminates the need for physical visits to a pharmacy. Online platforms often provide detailed information about the drugs, including usage instructions and potential side effects, empowering patients to make informed decisions about their treatment. However, the rise of online pharmacies also raises concerns about the authenticity and safety of medications, highlighting the importance of purchasing from reputable sources. The global market for oral anti-allergic drugs is influenced by the availability and accessibility of these distribution channels, which vary across regions. In areas with well-developed healthcare infrastructure, patients have greater access to a wide range of medications and distribution options. Conversely, in regions with limited healthcare resources, access to these drugs may be restricted, impacting patient outcomes. Efforts to improve distribution networks and ensure the availability of oral anti-allergic drugs are crucial in addressing the growing demand for allergy treatments worldwide. As technology continues to advance, the integration of digital tools and platforms in the distribution of these drugs is likely to expand, offering new opportunities for enhancing patient access and engagement. Overall, the distribution of oral anti-allergic drugs through hospital, retail, and online pharmacies plays a vital role in meeting the diverse needs of allergy sufferers, contributing to the broader goal of improving public health and quality of life.

Oral Anti-allergic Drugs - Global Market Outlook:

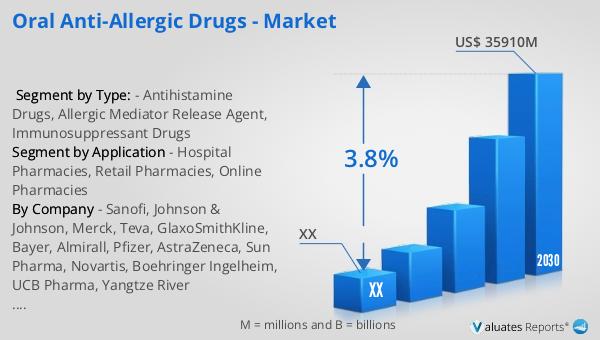

The global market for oral anti-allergic drugs was valued at approximately $27.71 billion in 2023, with projections indicating a growth to around $35.91 billion by 2030. This represents a compound annual growth rate (CAGR) of 3.8% during the forecast period from 2024 to 2030. In comparison, the broader global pharmaceutical market was valued at $1.475 trillion in 2022 and is expected to grow at a CAGR of 5% over the next six years. Meanwhile, the chemical drug market, a subset of the pharmaceutical industry, was estimated to grow from $1.005 trillion in 2018 to $1.094 trillion by 2022. These figures highlight the significant role that oral anti-allergic drugs play within the pharmaceutical landscape, addressing a critical need for effective allergy management solutions. The steady growth of the oral anti-allergic drugs market reflects the increasing prevalence of allergies worldwide and the ongoing demand for innovative treatments. As the market continues to evolve, driven by advancements in research and development, it is poised to make a substantial impact on the healthcare industry, offering relief to millions of allergy sufferers globally.

| Report Metric | Details |

| Report Name | Oral Anti-allergic Drugs - Market |

| Forecasted market size in 2030 | US$ 35910 million |

| CAGR | 3.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Sanofi, Johnson & Johnson, Merck, Teva, GlaxoSmithKline, Bayer, Almirall, Pfizer, AstraZeneca, Sun Pharma, Novartis, Boehringer Ingelheim, UCB Pharma, Yangtze River Pharmaceutical Group, Hainan Poly Pharm, Chongqing Huapont Pharmaceutical, Dawnrays Pharma |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |