What is Oil Field Special Vehicles - Global Market?

Oil Field Special Vehicles are specialized machines designed to perform various tasks in the oil and gas industry. These vehicles are crucial for operations in oil fields, where they are used to transport equipment, support drilling activities, and facilitate the extraction and processing of oil and gas. The global market for these vehicles is driven by the increasing demand for energy and the need for efficient and safe operations in oil fields. These vehicles are built to withstand harsh environments and are equipped with advanced technology to enhance their performance. The market is characterized by a wide range of vehicles, each designed for specific tasks, such as drilling, fracturing, and maintenance. As the oil and gas industry continues to grow, the demand for these specialized vehicles is expected to increase, driving innovation and development in the market. Companies in this sector are focusing on developing vehicles that are not only efficient but also environmentally friendly, as there is a growing emphasis on reducing the environmental impact of oil and gas operations. The market is also influenced by factors such as technological advancements, regulatory changes, and economic conditions, which can affect the demand and supply dynamics of these vehicles.

Frac Truck, Workover Rig Truck, Fracturing Blender Truck, Others in the Oil Field Special Vehicles - Global Market:

Frac trucks, workover rig trucks, fracturing blender trucks, and other specialized vehicles play a vital role in the oil field special vehicles market. Frac trucks are essential for hydraulic fracturing operations, where they are used to transport and pump fracturing fluid into wells to create fractures in the rock formations, allowing oil and gas to flow more freely. These trucks are equipped with high-pressure pumps and storage tanks to handle the large volumes of fluid required for the fracturing process. Workover rig trucks, on the other hand, are used for well maintenance and repair operations. They are designed to perform tasks such as removing and replacing well components, cleaning out wells, and performing other maintenance activities to ensure the efficient operation of oil and gas wells. These trucks are equipped with specialized equipment such as derricks, hoists, and winches to perform these tasks. Fracturing blender trucks are used to mix the fracturing fluid with proppants and other additives before it is pumped into the well. These trucks are equipped with mixing tanks, pumps, and other equipment to ensure the proper blending of the fluid. Other specialized vehicles in the oil field market include cementing trucks, which are used to pump cement into wells to secure the casing and prevent fluid migration, and coiled tubing trucks, which are used for various well intervention operations. These vehicles are equipped with coiled tubing reels, injectors, and other equipment to perform tasks such as well cleaning, stimulation, and logging. The demand for these specialized vehicles is driven by the increasing complexity of oil and gas operations, which require advanced technology and equipment to ensure efficient and safe operations. As the oil and gas industry continues to evolve, the market for these vehicles is expected to grow, driven by factors such as technological advancements, regulatory changes, and the increasing demand for energy. Companies in this sector are focusing on developing vehicles that are not only efficient but also environmentally friendly, as there is a growing emphasis on reducing the environmental impact of oil and gas operations. The market is also influenced by factors such as economic conditions, which can affect the demand and supply dynamics of these vehicles.

Petroleum, Natural Gas, Others in the Oil Field Special Vehicles - Global Market:

Oil field special vehicles are used extensively in the petroleum and natural gas industries, as well as in other sectors that require specialized equipment for drilling, extraction, and maintenance operations. In the petroleum industry, these vehicles are used for a wide range of tasks, including drilling, fracturing, and well maintenance. They are essential for transporting equipment and materials to and from drilling sites, as well as for performing various tasks such as cementing, coiled tubing operations, and well intervention. The use of these vehicles helps to ensure the efficient and safe operation of oil wells, reducing downtime and increasing productivity. In the natural gas industry, oil field special vehicles are used for similar tasks, including drilling, fracturing, and well maintenance. They are also used for transporting equipment and materials to and from drilling sites, as well as for performing various tasks such as cementing, coiled tubing operations, and well intervention. The use of these vehicles helps to ensure the efficient and safe operation of natural gas wells, reducing downtime and increasing productivity. In addition to the petroleum and natural gas industries, oil field special vehicles are also used in other sectors that require specialized equipment for drilling, extraction, and maintenance operations. These sectors include geothermal energy, mining, and construction, where these vehicles are used for tasks such as drilling, excavation, and transportation of materials. The use of these vehicles helps to ensure the efficient and safe operation of these industries, reducing downtime and increasing productivity. As the demand for energy continues to grow, the use of oil field special vehicles is expected to increase, driving innovation and development in the market. Companies in this sector are focusing on developing vehicles that are not only efficient but also environmentally friendly, as there is a growing emphasis on reducing the environmental impact of energy operations. The market is also influenced by factors such as technological advancements, regulatory changes, and economic conditions, which can affect the demand and supply dynamics of these vehicles.

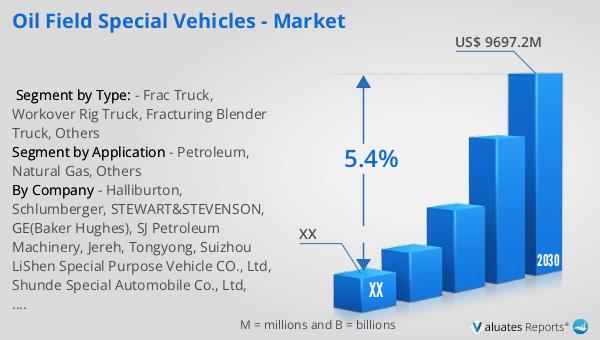

Oil Field Special Vehicles - Global Market Outlook:

The global market for oil field special vehicles was valued at approximately $6,795 million in 2023. It is projected to grow to a revised size of $9,697.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.4% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for energy and the need for efficient and safe operations in the oil and gas industry. The North American market for oil field special vehicles was valued at a certain amount in 2023 and is expected to reach a specific value by 2030, with a CAGR of a certain percentage during the forecast period from 2024 through 2030. This growth is attributed to the increasing complexity of oil and gas operations, which require advanced technology and equipment to ensure efficient and safe operations. Companies in this sector are focusing on developing vehicles that are not only efficient but also environmentally friendly, as there is a growing emphasis on reducing the environmental impact of oil and gas operations. The market is also influenced by factors such as technological advancements, regulatory changes, and economic conditions, which can affect the demand and supply dynamics of these vehicles. As the oil and gas industry continues to evolve, the market for these vehicles is expected to grow, driven by factors such as technological advancements, regulatory changes, and the increasing demand for energy.

| Report Metric | Details |

| Report Name | Oil Field Special Vehicles - Market |

| Forecasted market size in 2030 | US$ 9697.2 million |

| CAGR | 5.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Halliburton, Schlumberger, STEWART&STEVENSON, GE(Baker Hughes), SJ Petroleum Machinery, Jereh, Tongyong, Suizhou LiShen Special Purpose Vehicle CO., Ltd, Shunde Special Automobile Co., Ltd, SANY Group, Chusheng Vehicle Group, Shaanxi Automobile Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |