What is Medical Support Belt - Global Market?

Medical support belts are specialized devices designed to provide support and stability to various parts of the body, primarily focusing on the back and abdominal regions. These belts are widely used in the medical field to aid individuals suffering from conditions such as lower back pain, herniated discs, and post-surgical recovery. The global market for medical support belts has been expanding due to the increasing awareness of health and wellness, coupled with the rising prevalence of musculoskeletal disorders. These belts are crafted from materials that offer both flexibility and durability, ensuring comfort while providing the necessary support. The market is characterized by a variety of products catering to different needs, including back support belts, lumbar support belts, and other specialized belts for specific medical conditions. The demand for these products is driven by an aging population, increased participation in sports and physical activities, and a growing emphasis on preventive healthcare. As more people seek non-invasive solutions for pain management and injury prevention, the medical support belt market is poised for continued growth. Manufacturers are focusing on innovation, incorporating advanced materials and ergonomic designs to enhance the effectiveness and comfort of these belts.

Back Support, Lumbar Support, Others in the Medical Support Belt - Global Market:

Back support belts are a crucial segment within the medical support belt market, designed to alleviate pain and provide stability to individuals suffering from back-related issues. These belts are commonly used by people who engage in heavy lifting or have jobs that require prolonged standing. They work by compressing the abdominal area, which in turn reduces the strain on the lower back. Lumbar support belts, a subset of back support belts, specifically target the lumbar region of the spine. These belts are often recommended by healthcare professionals for individuals with chronic lower back pain or those recovering from back surgery. The design of lumbar support belts typically includes adjustable straps and breathable materials to ensure comfort during extended use. Other types of medical support belts include maternity belts, which provide support to pregnant women by alleviating pressure on the lower back and pelvis. Hernia belts are another category, designed to support the abdominal area and prevent the protrusion of hernias. These belts are often used post-surgery to aid in recovery and prevent further complications. The market for these various types of support belts is driven by the increasing prevalence of lifestyle-related health issues, such as obesity and sedentary behavior, which contribute to back problems. Additionally, the growing awareness of the benefits of preventive healthcare has led to a rise in the adoption of these belts among health-conscious individuals. Manufacturers are continuously innovating to meet the diverse needs of consumers, offering products with enhanced features such as moisture-wicking fabrics, adjustable compression levels, and ergonomic designs. The global market for medical support belts is also influenced by regional factors, with North America and Europe being significant markets due to their advanced healthcare infrastructure and high awareness levels. In contrast, emerging markets in Asia and Latin America are witnessing rapid growth due to increasing healthcare expenditure and rising awareness of musculoskeletal disorders. The competitive landscape of the medical support belt market is characterized by the presence of numerous players, ranging from established medical device companies to small-scale manufacturers. These companies are focusing on expanding their product portfolios and enhancing their distribution networks to capture a larger share of the market. Strategic partnerships, mergers, and acquisitions are common strategies employed by key players to strengthen their market position. As the demand for medical support belts continues to grow, manufacturers are also exploring opportunities in the online retail space, leveraging e-commerce platforms to reach a wider audience. The convenience of online shopping, coupled with the availability of detailed product information and customer reviews, has made it easier for consumers to make informed purchasing decisions. Overall, the medical support belt market is poised for sustained growth, driven by factors such as increasing health awareness, technological advancements, and the rising prevalence of musculoskeletal disorders.

Adult, Child in the Medical Support Belt - Global Market:

Medical support belts are used by both adults and children, although the specific needs and applications may vary between these two groups. For adults, medical support belts are commonly used to manage chronic pain, support recovery from injuries, and prevent further damage to vulnerable areas of the body. Adults who suffer from conditions such as sciatica, herniated discs, or degenerative disc disease often rely on back support belts to alleviate pain and improve mobility. These belts are also popular among athletes and individuals who engage in strenuous physical activities, as they provide additional support and reduce the risk of injury. In the workplace, adults who perform manual labor or have jobs that require prolonged standing or sitting may use lumbar support belts to prevent strain and discomfort. For pregnant women, maternity belts offer support to the lower back and abdomen, helping to alleviate the discomfort associated with carrying extra weight. On the other hand, the use of medical support belts in children is typically more specialized and often recommended by healthcare professionals. Children with conditions such as scoliosis or other spinal deformities may use back braces or support belts as part of their treatment plan. These belts help to correct posture and provide stability to the spine, promoting proper alignment and reducing the risk of further complications. In some cases, children recovering from surgery or injury may also benefit from the use of support belts to aid in their recovery process. The design of medical support belts for children often takes into consideration their smaller size and unique needs, ensuring that the belts are comfortable and effective. The global market for medical support belts catering to both adults and children is driven by factors such as the increasing prevalence of musculoskeletal disorders, rising awareness of preventive healthcare, and advancements in medical technology. Manufacturers are focusing on developing products that cater to the specific needs of different age groups, incorporating features such as adjustable sizing, breathable materials, and ergonomic designs. As the demand for non-invasive solutions for pain management and injury prevention continues to grow, the market for medical support belts is expected to expand further.

Medical Support Belt - Global Market Outlook:

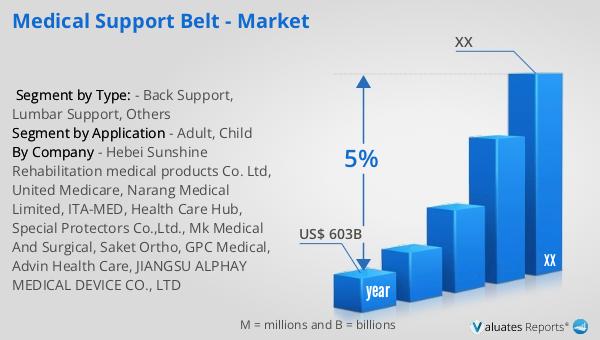

According to our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory highlights the increasing demand for medical devices, including medical support belts, as more individuals seek effective solutions for managing health conditions and improving their quality of life. The rising prevalence of chronic diseases, coupled with an aging population, is driving the demand for innovative medical devices that offer non-invasive and cost-effective solutions. Medical support belts, as a segment of this broader market, are gaining traction due to their ability to provide relief from pain and support recovery from injuries. The market is also benefiting from advancements in technology, which have led to the development of more comfortable and effective support belts. As healthcare systems around the world continue to evolve, there is a growing emphasis on preventive care and the management of chronic conditions, further fueling the demand for medical devices. The increasing awareness of the benefits of medical support belts, along with the availability of a wide range of products catering to different needs, is expected to contribute to the sustained growth of this market segment. Manufacturers are focusing on expanding their product offerings and enhancing their distribution networks to capture a larger share of the market. The competitive landscape is characterized by the presence of numerous players, ranging from established medical device companies to small-scale manufacturers, all vying for a share of this lucrative market. As the global market for medical devices continues to grow, the medical support belt segment is poised to play a significant role in meeting the evolving needs of consumers seeking effective solutions for pain management and injury prevention.

| Report Metric | Details |

| Report Name | Medical Support Belt - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Hebei Sunshine Rehabilitation medical products Co. Ltd, United Medicare, Narang Medical Limited, ITA-MED, Health Care Hub, Special Protectors Co.,Ltd., Mk Medical And Surgical, Saket Ortho, GPC Medical, Advin Health Care, JIANGSU ALPHAY MEDICAL DEVICE CO., LTD |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |