What is Global Electric Apron Bus Market?

The Global Electric Apron Bus Market refers to the industry focused on the production and distribution of electric buses specifically designed for use on airport aprons. These buses are used to transport passengers between terminals and aircraft, as well as to shuttle crew and ground staff around the airport. The shift towards electric apron buses is driven by the need to reduce carbon emissions, improve air quality, and comply with stringent environmental regulations. Electric apron buses offer several advantages over their diesel counterparts, including lower operating costs, reduced noise pollution, and enhanced passenger comfort. The market encompasses various stakeholders, including bus manufacturers, battery suppliers, airport authorities, and regulatory bodies. As airports worldwide strive to become more sustainable, the demand for electric apron buses is expected to grow, making this market a crucial component of the broader push towards greener aviation operations.

LTO Battery, LFP Battery in the Global Electric Apron Bus Market:

LTO (Lithium Titanate Oxide) and LFP (Lithium Iron Phosphate) batteries are two prominent types of batteries used in the Global Electric Apron Bus Market. LTO batteries are known for their high safety, long cycle life, and fast charging capabilities. These batteries can withstand a large number of charge and discharge cycles, making them ideal for the rigorous demands of airport operations. LTO batteries also perform well in a wide range of temperatures, which is crucial for apron buses that operate in various climatic conditions. On the other hand, LFP batteries are favored for their high energy density, long lifespan, and thermal stability. They are less prone to overheating and are considered safer than other lithium-ion batteries. LFP batteries also offer a good balance between cost and performance, making them a popular choice for electric apron buses. Both LTO and LFP batteries contribute to the efficiency and reliability of electric apron buses, ensuring that they can operate effectively in the demanding environment of an airport. The choice between LTO and LFP batteries often depends on specific operational requirements, such as the need for rapid charging or the ability to function in extreme temperatures. As technology advances, the performance and cost-effectiveness of these batteries continue to improve, further driving the adoption of electric apron buses in airports around the world.

Domestic Airport, International Airport in the Global Electric Apron Bus Market:

The usage of electric apron buses in domestic and international airports is becoming increasingly prevalent as airports seek to enhance their sustainability and operational efficiency. In domestic airports, electric apron buses are primarily used to transport passengers between terminals and aircraft, as well as to shuttle crew and ground staff. These buses help reduce the carbon footprint of airport operations, contributing to cleaner air and a quieter environment. The reduced noise pollution is particularly beneficial in domestic airports located near residential areas, as it minimizes the impact on local communities. Additionally, the lower operating costs of electric apron buses make them an attractive option for domestic airports looking to optimize their budgets. In international airports, the scale of operations is typically larger, and the demand for efficient and reliable ground transportation is even more critical. Electric apron buses in international airports are used not only for passenger transport but also for moving luggage, cargo, and other essential equipment. The ability to quickly charge and deploy these buses ensures that international airports can maintain smooth and uninterrupted operations. Furthermore, the use of electric apron buses aligns with the global trend towards greener aviation practices, helping international airports meet stringent environmental regulations and enhance their reputation as sustainable travel hubs. Overall, the adoption of electric apron buses in both domestic and international airports represents a significant step towards more sustainable and efficient airport operations.

Global Electric Apron Bus Market Outlook:

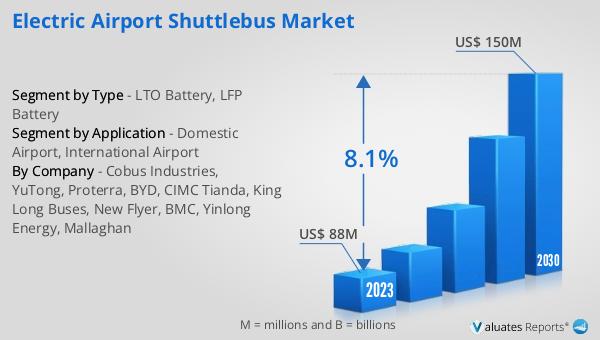

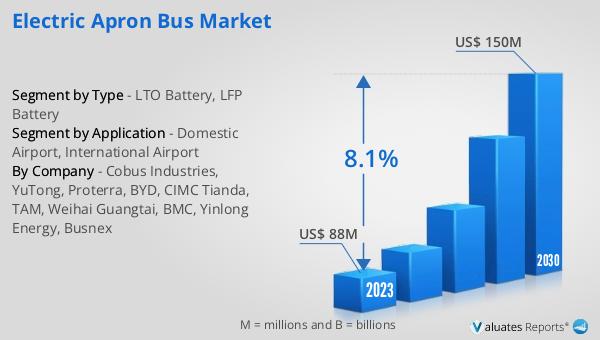

The global Electric Apron Bus market was valued at US$ 88 million in 2023 and is anticipated to reach US$ 150 million by 2030, witnessing a CAGR of 8.1% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for sustainable and efficient ground transportation solutions in airports worldwide. As airports continue to expand and modernize, the need for electric apron buses is expected to rise, driven by the benefits of reduced emissions, lower operating costs, and improved passenger experience. The market's growth is also supported by advancements in battery technology, which enhance the performance and reliability of electric apron buses. With the aviation industry under pressure to reduce its environmental impact, the adoption of electric apron buses is likely to become a key component of airport sustainability strategies. The projected growth of the Electric Apron Bus market underscores the importance of investing in green technologies to meet the evolving needs of modern airports.

| Report Metric | Details |

| Report Name | Electric Apron Bus Market |

| Accounted market size in 2023 | US$ 88 million |

| Forecasted market size in 2030 | US$ 150 million |

| CAGR | 8.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Cobus Industries, YuTong, Proterra, BYD, CIMC Tianda, TAM, Weihai Guangtai, BMC, Yinlong Energy, Busnex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |