What is Global Aluminum-Magnesium Alloy Welding Wire Market?

The Global Aluminum-Magnesium Alloy Welding Wire Market refers to the worldwide industry involved in the production, distribution, and utilization of welding wires made from aluminum-magnesium alloys. These welding wires are essential in various industries due to their excellent corrosion resistance, high strength, and lightweight properties. They are primarily used in applications where durability and performance are critical, such as in the automotive, shipbuilding, and appliance industries. The market encompasses a wide range of activities, including the extraction of raw materials, manufacturing processes, quality control, and distribution channels. The demand for aluminum-magnesium alloy welding wires is driven by the increasing need for lightweight and durable materials in various industrial applications. As industries continue to innovate and seek more efficient and sustainable solutions, the market for these specialized welding wires is expected to grow. The global nature of this market means that it is influenced by international trade policies, technological advancements, and economic conditions across different regions.

0.4mm Diameter, 0.5mm Diameter, Other in the Global Aluminum-Magnesium Alloy Welding Wire Market:

In the Global Aluminum-Magnesium Alloy Welding Wire Market, the diameters of the wires play a crucial role in determining their suitability for various applications. The 0.4mm diameter welding wire is typically used for precision welding tasks where fine control and minimal material deposition are required. This makes it ideal for intricate work in industries such as electronics and small-scale manufacturing. The 0.5mm diameter welding wire, on the other hand, offers a balance between precision and material deposition, making it suitable for a broader range of applications, including automotive and appliance manufacturing. Other diameters, which can range from very thin wires to thicker ones, cater to specific needs in different industries. For instance, thicker wires are often used in heavy-duty applications such as shipbuilding and construction, where strength and durability are paramount. The choice of wire diameter depends on several factors, including the type of material being welded, the required strength of the weld, and the specific application. In the automotive industry, for example, different diameters may be used for welding various components, from body panels to structural parts. Similarly, in the shipbuilding industry, the choice of wire diameter can affect the overall integrity and performance of the welded structures. The versatility of aluminum-magnesium alloy welding wires in terms of diameter options allows manufacturers to select the most appropriate wire for their specific needs, ensuring optimal performance and efficiency. This flexibility is one of the key factors driving the growth of the Global Aluminum-Magnesium Alloy Welding Wire Market, as it enables industries to meet their unique requirements and achieve high-quality welds.

Automobile Industry, Shipbuilding Industry, Appliance Industry, Others in the Global Aluminum-Magnesium Alloy Welding Wire Market:

The usage of Global Aluminum-Magnesium Alloy Welding Wire Market in various industries highlights its versatility and importance. In the automobile industry, these welding wires are used extensively for joining different components of vehicles, including body panels, frames, and engine parts. The lightweight and high-strength properties of aluminum-magnesium alloys make them ideal for automotive applications, where reducing weight without compromising strength is crucial for improving fuel efficiency and performance. In the shipbuilding industry, aluminum-magnesium alloy welding wires are used for constructing and repairing ships and other marine structures. The excellent corrosion resistance of these alloys is particularly beneficial in marine environments, where exposure to saltwater and harsh conditions can lead to rapid deterioration of materials. The appliance industry also relies on aluminum-magnesium alloy welding wires for manufacturing various household and industrial appliances. These wires are used to join different metal parts, ensuring durability and longevity of the appliances. Other industries, such as aerospace, construction, and electronics, also utilize these welding wires for their specific needs. In aerospace, for instance, the lightweight and high-strength properties of aluminum-magnesium alloys are essential for constructing aircraft components. In construction, these welding wires are used for joining structural elements, providing strength and stability to buildings and infrastructure. The electronics industry benefits from the precision and reliability of aluminum-magnesium alloy welding wires for assembling electronic devices and components. Overall, the widespread usage of these welding wires across different industries underscores their significance and the growing demand for high-quality, durable, and efficient welding solutions.

Global Aluminum-Magnesium Alloy Welding Wire Market Outlook:

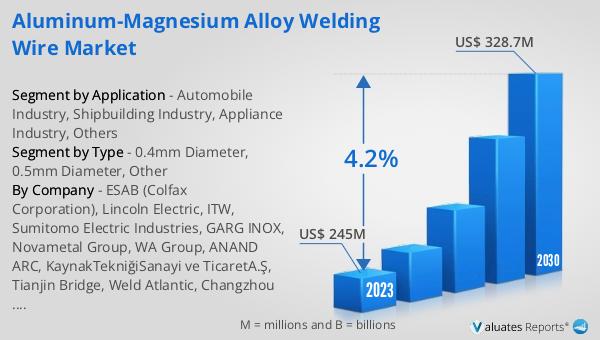

The global Aluminum-Magnesium Alloy Welding Wire market was valued at US$ 245 million in 2023 and is anticipated to reach US$ 328.7 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. Major manufacturers in the global aluminum welding wires market include ESAB, Colfax Corporation, Lincoln Electric, and ITW, collectively accounting for about 35% of the market. China stands out as the largest market, holding a share of over 10%. This market outlook indicates a steady growth trajectory driven by the increasing demand for lightweight and durable materials across various industries. The presence of key manufacturers and the significant market share held by China highlight the competitive landscape and the importance of strategic positioning in this market. As industries continue to seek innovative and efficient welding solutions, the Global Aluminum-Magnesium Alloy Welding Wire Market is poised for sustained growth and development.

| Report Metric | Details |

| Report Name | Aluminum-Magnesium Alloy Welding Wire Market |

| Accounted market size in 2023 | US$ 245 million |

| Forecasted market size in 2030 | US$ 328.7 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ESAB (Colfax Corporation), Lincoln Electric, ITW, Sumitomo Electric Industries, GARG INOX, Novametal Group, WA Group, ANAND ARC, KaynakTekniğiSanayi ve TicaretA.Ş, Tianjin Bridge, Weld Atlantic, Changzhou Huatong Welding, Jinglei Welding, Shandong Juli Welding, Huaya Aluminium |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |