What is Global UAV Power Systems Market?

The Global UAV Power Systems Market refers to the industry focused on the development, production, and distribution of power systems specifically designed for Unmanned Aerial Vehicles (UAVs). These power systems are crucial for the operation of UAVs, providing the necessary energy to power their engines, sensors, and communication systems. The market encompasses a wide range of technologies, including batteries, fuel cells, and hybrid systems, each offering different advantages in terms of energy density, weight, and operational efficiency. The increasing adoption of UAVs across various sectors such as military, commercial, and industrial applications has significantly driven the demand for advanced power systems. Innovations in battery technology and the development of more efficient fuel cells are key trends in this market, aimed at enhancing the flight time and payload capacity of UAVs. The market is also influenced by regulatory frameworks and environmental considerations, pushing for more sustainable and efficient power solutions. Overall, the Global UAV Power Systems Market is a dynamic and rapidly evolving sector, playing a critical role in the advancement of UAV technology and its applications across different industries.

Uniaxial, Coaxial in the Global UAV Power Systems Market:

Uniaxial and coaxial power systems are two prominent types of propulsion mechanisms used in the Global UAV Power Systems Market. Uniaxial power systems refer to configurations where a single axis is used for the propulsion and control of the UAV. This setup is typically simpler and lighter, making it suitable for smaller UAVs that require less power and have shorter flight durations. Uniaxial systems are often powered by electric motors and batteries, which provide a good balance between weight and energy efficiency. These systems are commonly used in commercial drones for applications such as aerial photography, surveying, and small-scale deliveries. On the other hand, coaxial power systems involve the use of two or more rotors mounted on the same axis but rotating in opposite directions. This configuration offers several advantages, including increased lift capacity, improved stability, and redundancy in case of motor failure. Coaxial systems are particularly beneficial for larger UAVs that need to carry heavier payloads or operate in challenging environments. They are often powered by a combination of batteries and fuel cells, providing a hybrid solution that extends flight time and enhances performance. Coaxial systems are widely used in military applications, where reliability and robustness are critical, as well as in industrial settings for tasks such as inspection, mapping, and logistics. Both uniaxial and coaxial power systems are integral to the advancement of UAV technology, each offering unique benefits that cater to different operational requirements and industry needs. The choice between uniaxial and coaxial systems depends on various factors, including the size of the UAV, the nature of the mission, and the specific performance criteria. As the Global UAV Power Systems Market continues to grow, ongoing research and development efforts are focused on optimizing these propulsion mechanisms to achieve greater efficiency, longer flight times, and enhanced capabilities. This includes advancements in battery technology, the integration of renewable energy sources, and the development of more sophisticated control systems. The evolution of uniaxial and coaxial power systems is a testament to the innovative spirit driving the UAV industry, paving the way for new applications and expanding the potential of unmanned aerial technology.

Business, Military, Industrial Factories and Mines in the Global UAV Power Systems Market:

The usage of Global UAV Power Systems Market spans across various sectors, including business, military, industrial factories, and mines, each benefiting from the unique capabilities of UAVs. In the business sector, UAVs powered by advanced power systems are increasingly used for tasks such as aerial photography, real estate marketing, and delivery services. Companies leverage UAVs to capture high-resolution images and videos, providing a competitive edge in marketing and promotional activities. Additionally, UAVs are employed for last-mile delivery, offering a faster and more efficient alternative to traditional delivery methods. The military sector is one of the largest users of UAVs, relying on them for surveillance, reconnaissance, and combat missions. Advanced power systems enable military UAVs to operate for extended periods, carry sophisticated payloads, and perform complex maneuvers. These capabilities are crucial for gathering intelligence, monitoring enemy movements, and conducting precision strikes. In industrial factories, UAVs are used for inspection and maintenance tasks, particularly in hard-to-reach areas. Equipped with high-capacity power systems, these UAVs can perform detailed inspections of machinery, pipelines, and infrastructure, reducing the need for manual inspections and minimizing downtime. In the mining industry, UAVs are utilized for mapping and surveying large areas, providing accurate data on terrain and mineral deposits. The power systems in these UAVs ensure they can cover vast distances and operate in harsh environments, enhancing the efficiency and safety of mining operations. Overall, the Global UAV Power Systems Market plays a pivotal role in enabling the diverse applications of UAVs across different sectors, driving innovation and improving operational efficiency.

Global UAV Power Systems Market Outlook:

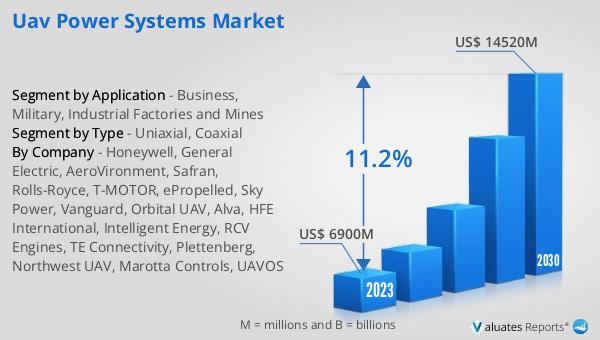

The global UAV Power Systems market, valued at US$ 6900 million in 2023, is projected to reach US$ 14520 million by 2030, reflecting a compound annual growth rate (CAGR) of 11.2% during the forecast period from 2024 to 2030. This significant growth underscores the increasing demand for advanced power systems that can enhance the performance and capabilities of UAVs. The market's expansion is driven by the rising adoption of UAVs across various industries, including military, commercial, and industrial sectors. Innovations in battery technology, fuel cells, and hybrid systems are key factors contributing to this growth, as they offer improved energy efficiency, longer flight times, and greater payload capacities. Additionally, regulatory frameworks and environmental considerations are pushing for more sustainable and efficient power solutions, further propelling the market forward. The continuous advancements in UAV power systems are expected to unlock new applications and opportunities, solidifying the market's position as a critical component of the broader UAV industry.

| Report Metric | Details |

| Report Name | UAV Power Systems Market |

| Accounted market size in 2023 | US$ 6900 million |

| Forecasted market size in 2030 | US$ 14520 million |

| CAGR | 11.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Honeywell, General Electric, AeroVironment, Safran, Rolls-Royce, T-MOTOR, ePropelled, Sky Power, Vanguard, Orbital UAV, Alva, HFE International, Intelligent Energy, RCV Engines, TE Connectivity, Plettenberg, Northwest UAV, Marotta Controls, UAVOS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |