What is Global Spring-type Floor Drain Market?

The Global Spring-type Floor Drain Market refers to the worldwide industry focused on the production, distribution, and sale of spring-type floor drains. These specialized drains are designed to prevent backflow and ensure efficient drainage in various settings, including residential, commercial, municipal, industrial, and marine environments. The market encompasses a wide range of products made from different materials such as cast iron, stainless steel, and other metals. The demand for these drains is driven by their effectiveness in preventing water accumulation and their ability to maintain hygiene by preventing the entry of pests and odors. The market is influenced by factors such as urbanization, construction activities, and the need for efficient water management systems. As infrastructure development continues globally, the demand for reliable and durable drainage solutions like spring-type floor drains is expected to grow.

Cast Iron Material, Stainless Steel Material in the Global Spring-type Floor Drain Market:

In the Global Spring-type Floor Drain Market, materials like cast iron and stainless steel play a crucial role in determining the durability, efficiency, and application of the products. Cast iron material is known for its robustness and longevity, making it a popular choice for heavy-duty applications. It is highly resistant to wear and tear, which makes it suitable for industrial and municipal uses where the drains are subjected to high traffic and heavy loads. Cast iron drains are also favored for their ability to withstand extreme temperatures and harsh environmental conditions, ensuring reliable performance over time. On the other hand, stainless steel material is prized for its corrosion resistance and aesthetic appeal. Stainless steel drains are commonly used in settings where hygiene is paramount, such as in commercial kitchens, hospitals, and food processing plants. The smooth surface of stainless steel prevents the buildup of bacteria and is easy to clean, making it ideal for environments that require stringent sanitary standards. Additionally, stainless steel drains are lightweight compared to cast iron, which can simplify installation and reduce labor costs. Both materials have their unique advantages and are chosen based on the specific requirements of the application. The choice between cast iron and stainless steel often depends on factors such as the nature of the environment, the load-bearing capacity needed, and the budget constraints. As the Global Spring-type Floor Drain Market continues to evolve, manufacturers are constantly innovating to improve the performance and versatility of these materials, ensuring that they meet the diverse needs of their customers.

Household Used, Commercial Used, Municipal Used, Industrial Used, Marine Used in the Global Spring-type Floor Drain Market:

The usage of Global Spring-type Floor Drain Market products spans across various sectors, each with its unique requirements and challenges. In household settings, these drains are essential for maintaining clean and dry environments in areas like bathrooms, kitchens, and basements. They help prevent water accumulation, which can lead to mold growth and structural damage. In commercial settings, such as restaurants, hotels, and shopping malls, spring-type floor drains are crucial for managing large volumes of water efficiently. They ensure that areas remain safe and hygienic for both customers and staff. Municipal applications of spring-type floor drains include their use in public infrastructure like streets, parks, and public restrooms. These drains help manage stormwater and prevent flooding, ensuring that public spaces remain accessible and safe. In industrial settings, spring-type floor drains are used in factories, warehouses, and manufacturing plants to handle wastewater and spills. They are designed to withstand heavy loads and harsh conditions, ensuring reliable performance in demanding environments. Marine applications of spring-type floor drains include their use on ships and offshore platforms. These drains are essential for managing water on board, preventing flooding, and ensuring the safety and stability of the vessel. Each of these applications requires specific features and capabilities from the floor drains, and manufacturers in the Global Spring-type Floor Drain Market are continually innovating to meet these diverse needs.

Global Spring-type Floor Drain Market Outlook:

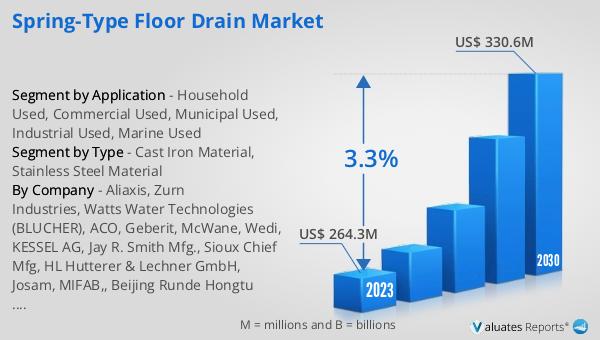

The global Spring-type Floor Drain market was valued at US$ 264.3 million in 2023 and is anticipated to reach US$ 330.6 million by 2030, witnessing a CAGR of 3.3% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by increasing demand for efficient drainage solutions across various sectors. The growth is attributed to factors such as urbanization, infrastructure development, and the need for effective water management systems. As more residential, commercial, and industrial projects are undertaken globally, the demand for reliable and durable floor drains is expected to rise. The market's expansion is also supported by advancements in materials and technology, which enhance the performance and longevity of spring-type floor drains. With a focus on preventing water accumulation, backflow, and ensuring hygiene, these drains are becoming an essential component in modern construction and infrastructure projects. The projected growth in the market underscores the importance of innovative and high-quality drainage solutions in addressing the challenges posed by increasing urbanization and environmental concerns.

| Report Metric | Details |

| Report Name | Spring-type Floor Drain Market |

| Accounted market size in 2023 | US$ 264.3 million |

| Forecasted market size in 2030 | US$ 330.6 million |

| CAGR | 3.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Aliaxis, Zurn Industries, Watts Water Technologies (BLUCHER), ACO, Geberit, McWane, Wedi, KESSEL AG, Jay R. Smith Mfg., Sioux Chief Mfg, HL Hutterer & Lechner GmbH, Josam, MIFAB,, Beijing Runde Hongtu Technology Development, Unidrain A/S, Gridiron SpA, Jomoo, AWI, Caggiati Maurizio, Miro Europe, WeiXing NBM, Ferplast Srl |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |