What is Global Antihemophilic Factor Market?

The Global Antihemophilic Factor Market is a specialized segment within the broader pharmaceutical and healthcare industry, focusing on the development, production, and distribution of antihemophilic factors. These are essential proteins used in the treatment of hemophilia, a genetic disorder that impairs the body's ability to make blood clots, leading to excessive bleeding. The market is driven by the increasing prevalence of hemophilia worldwide, advancements in biotechnology, and the growing awareness about the disease and its management. Antihemophilic factors are primarily used to replace the missing or deficient clotting factors in patients, thereby preventing or controlling bleeding episodes. The market is characterized by a range of products, including recombinant and plasma-derived factors, each with its own set of benefits and challenges. Companies operating in this market are continually investing in research and development to improve the efficacy and safety of these products, as well as to explore new therapeutic options. The market is also influenced by regulatory policies, pricing pressures, and the need for cost-effective treatment options, particularly in developing regions. Overall, the Global Antihemophilic Factor Market plays a crucial role in improving the quality of life for individuals with hemophilia.

Powder, Liquid in the Global Antihemophilic Factor Market:

In the Global Antihemophilic Factor Market, products are primarily available in two forms: powder and liquid. Each form has its own unique characteristics, advantages, and considerations for use. Powdered antihemophilic factors are typically lyophilized, meaning they are freeze-dried to remove moisture, which helps in preserving the stability and potency of the product over time. This form is advantageous for storage and transportation, as it generally has a longer shelf life compared to liquid forms. Before administration, the powdered form needs to be reconstituted with a sterile diluent, which can be a straightforward process but requires careful handling to ensure the correct dosage and prevent contamination. On the other hand, liquid antihemophilic factors are ready-to-use solutions that do not require reconstitution, offering convenience and ease of use, particularly in emergency situations where time is of the essence. However, liquid forms may have a shorter shelf life and require specific storage conditions to maintain their efficacy. The choice between powder and liquid forms often depends on various factors, including the patient's needs, the healthcare setting, and logistical considerations. For instance, in hospital settings where immediate treatment is crucial, liquid forms may be preferred for their quick administration. Conversely, in home care settings, powdered forms might be favored for their storage benefits and longer shelf life. Additionally, the development of both forms involves rigorous quality control and adherence to regulatory standards to ensure safety and effectiveness. Manufacturers are continually working to improve the formulations of both powder and liquid antihemophilic factors, focusing on enhancing stability, reducing the risk of adverse reactions, and improving patient compliance. The market for these products is also influenced by technological advancements, such as the development of novel delivery systems and the exploration of gene therapy as a potential long-term solution for hemophilia. As the demand for effective hemophilia treatments continues to grow, the Global Antihemophilic Factor Market is expected to see ongoing innovation and expansion in both powder and liquid product offerings.

Hospital, Clinic in the Global Antihemophilic Factor Market:

The usage of Global Antihemophilic Factor Market products is particularly significant in hospitals and clinics, where they play a vital role in the management and treatment of hemophilia. In hospital settings, antihemophilic factors are essential for both routine care and emergency interventions. Hospitals often serve as the primary point of care for patients experiencing severe bleeding episodes, where immediate administration of antihemophilic factors can be life-saving. The availability of both powder and liquid forms allows healthcare providers to choose the most appropriate option based on the urgency of the situation and the specific needs of the patient. In addition to acute care, hospitals also use these factors for prophylactic treatment, aiming to prevent bleeding episodes in patients with severe hemophilia. This proactive approach helps in reducing hospital admissions and improving the overall quality of life for patients. Clinics, on the other hand, often focus on the ongoing management and monitoring of hemophilia patients. They provide a more accessible and less intensive setting for regular check-ups, consultations, and prophylactic treatments. Clinics may also offer educational programs to help patients and their families understand the condition and manage it effectively at home. The use of antihemophilic factors in clinics is typically more focused on long-term care and prevention, with an emphasis on maintaining optimal health and preventing complications. Both hospitals and clinics rely on a multidisciplinary approach to hemophilia care, involving hematologists, nurses, and other healthcare professionals who work together to develop individualized treatment plans. The integration of antihemophilic factors into these plans is crucial for achieving the best possible outcomes for patients. Furthermore, the collaboration between hospitals, clinics, and pharmaceutical companies is essential for ensuring the availability and accessibility of these life-saving treatments. As the Global Antihemophilic Factor Market continues to evolve, the role of hospitals and clinics in delivering comprehensive hemophilia care remains indispensable.

Global Antihemophilic Factor Market Outlook:

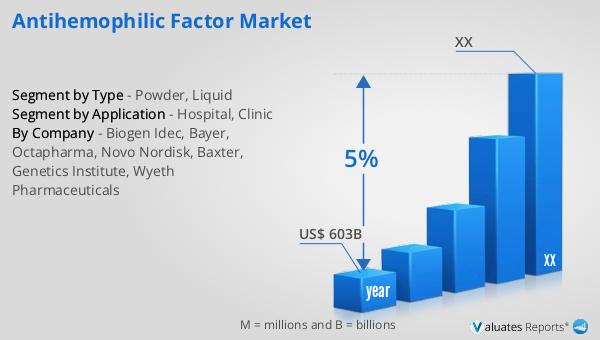

Our research indicates that the global market for medical devices, which includes the Global Antihemophilic Factor Market, is projected to reach approximately US$ 603 billion in 2023. This substantial market size reflects the growing demand for medical devices and related products worldwide. Over the next six years, the market is expected to expand at a compound annual growth rate (CAGR) of 5%. This growth trajectory underscores the increasing importance of medical devices in healthcare, driven by factors such as technological advancements, rising healthcare expenditures, and the growing prevalence of chronic diseases. The Global Antihemophilic Factor Market, as a part of this broader medical device market, is poised to benefit from these trends. The demand for effective hemophilia treatments is likely to contribute to the overall growth of the market, as healthcare providers and patients seek innovative solutions to manage this complex condition. Additionally, the focus on improving patient outcomes and enhancing the quality of life for individuals with hemophilia will continue to drive research and development efforts in this field. As the market evolves, stakeholders across the healthcare ecosystem, including manufacturers, healthcare providers, and policymakers, will play a crucial role in shaping the future of the Global Antihemophilic Factor Market.

| Report Metric | Details |

| Report Name | Antihemophilic Factor Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Biogen Idec, Bayer, Octapharma, Novo Nordisk, Baxter, Genetics Institute, Wyeth Pharmaceuticals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |