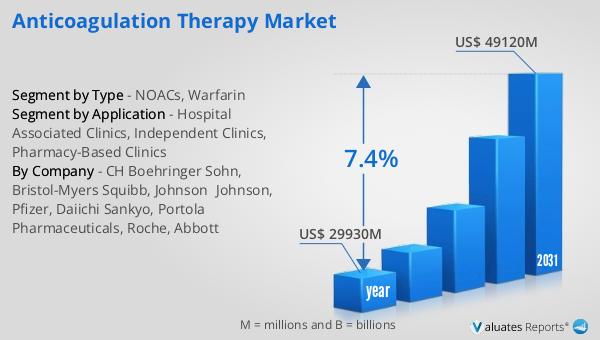

What is Global Adenovirus Vaccine Market?

The Global Adenovirus Vaccine Market is a rapidly evolving sector within the pharmaceutical industry, focusing on the development and distribution of vaccines targeting adenovirus infections. Adenoviruses are common pathogens that can cause a range of illnesses, from mild respiratory infections to more severe conditions like conjunctivitis and gastroenteritis. The market for adenovirus vaccines is driven by the increasing awareness of these infections and the need for effective preventive measures, especially in military and institutional settings where outbreaks are more common. The market is characterized by ongoing research and development efforts aimed at improving vaccine efficacy and expanding the range of adenovirus types covered. With advancements in biotechnology and a growing emphasis on public health, the Global Adenovirus Vaccine Market is poised for significant growth, offering promising opportunities for pharmaceutical companies and healthcare providers alike. The market's expansion is further supported by government initiatives and funding aimed at enhancing vaccine accessibility and distribution, ensuring that populations at risk are adequately protected against adenovirus infections. As the demand for effective vaccines continues to rise, the Global Adenovirus Vaccine Market is expected to play a crucial role in safeguarding public health on a global scale.

Type 4 Vaccine, Type 7 Vaccine in the Global Adenovirus Vaccine Market:

The Global Adenovirus Vaccine Market includes specific vaccines such as the Type 4 and Type 7 vaccines, which are particularly significant due to their targeted approach in preventing adenovirus infections. The Type 4 vaccine is designed to combat adenovirus type 4, a common cause of respiratory illness, especially in crowded environments like military barracks and college dormitories. This vaccine is typically administered to military recruits to prevent outbreaks that can lead to significant health issues and operational disruptions. The Type 4 vaccine works by stimulating the immune system to recognize and fight the adenovirus, thereby reducing the incidence of infection and its associated complications. On the other hand, the Type 7 vaccine targets adenovirus type 7, another prevalent strain that can cause severe respiratory illnesses. Similar to the Type 4 vaccine, the Type 7 vaccine is primarily used in military settings to protect recruits from outbreaks that can compromise their health and readiness. The development of these vaccines is based on extensive research and clinical trials, ensuring their safety and efficacy in preventing adenovirus infections. Both vaccines are administered orally, which simplifies the vaccination process and enhances compliance among recipients. The availability of these vaccines has significantly reduced the incidence of adenovirus-related illnesses in military populations, highlighting their importance in maintaining public health and operational efficiency. The Global Adenovirus Vaccine Market continues to evolve, with ongoing research aimed at improving existing vaccines and developing new ones to cover a broader range of adenovirus types. This includes efforts to enhance vaccine formulations, optimize dosing regimens, and expand the use of these vaccines beyond military settings to other high-risk populations. As the market grows, it is expected to contribute significantly to the prevention of adenovirus infections, ultimately improving health outcomes and reducing the burden on healthcare systems worldwide. The focus on Type 4 and Type 7 vaccines underscores the importance of targeted vaccination strategies in addressing specific public health challenges, demonstrating the potential of the Global Adenovirus Vaccine Market to make a meaningful impact on global health.

Research & Academic Laboratories, Pharmaceutical & Biotechnology Companies, Others in the Global Adenovirus Vaccine Market:

The Global Adenovirus Vaccine Market finds its application in various sectors, including research and academic laboratories, pharmaceutical and biotechnology companies, and other areas. In research and academic laboratories, adenovirus vaccines are used as a critical tool for studying viral pathogenesis, immune responses, and vaccine development. These laboratories conduct extensive research to understand the mechanisms of adenovirus infections and to develop new vaccines that can provide broader protection against multiple adenovirus types. The insights gained from this research are crucial for advancing vaccine technology and improving public health strategies. In pharmaceutical and biotechnology companies, adenovirus vaccines represent a significant area of investment and innovation. These companies are involved in the development, production, and distribution of adenovirus vaccines, leveraging advanced biotechnological techniques to enhance vaccine efficacy and safety. The competitive landscape in this sector drives continuous improvement and innovation, leading to the development of next-generation vaccines that can address emerging public health challenges. Additionally, pharmaceutical companies collaborate with government agencies and international organizations to ensure the widespread availability and accessibility of adenovirus vaccines, particularly in regions with high disease burden. Beyond research and pharmaceutical sectors, adenovirus vaccines are also used in other areas such as military and institutional settings, where the risk of adenovirus outbreaks is higher due to close living quarters and high population density. In these settings, adenovirus vaccines are administered to prevent outbreaks that can lead to significant health and operational challenges. The use of adenovirus vaccines in these areas underscores their importance in maintaining public health and operational readiness. As the Global Adenovirus Vaccine Market continues to grow, its applications are expected to expand, contributing to improved health outcomes and reduced healthcare costs worldwide. The integration of adenovirus vaccines into broader public health strategies highlights their potential to address pressing health challenges and enhance global health security.

Global Adenovirus Vaccine Market Outlook:

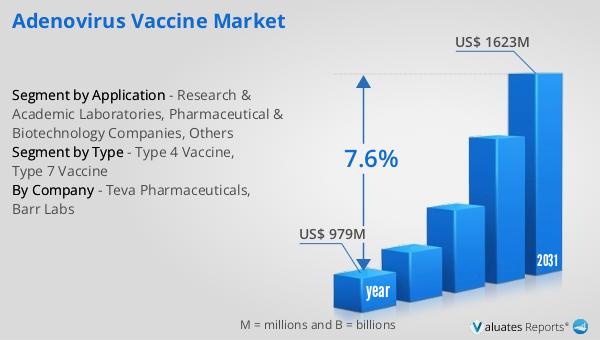

The global market for Adenovirus Vaccine was valued at approximately $979 million in 2024 and is anticipated to grow to a revised size of around $1,623 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.6% during the forecast period. This growth is indicative of the increasing demand for effective vaccines to combat adenovirus infections, driven by heightened awareness and the need for preventive healthcare solutions. In comparison, the global pharmaceutical market was valued at $1,475 billion in 2022, with an expected growth rate of 5% over the next six years. This broader market growth underscores the dynamic nature of the pharmaceutical industry, which encompasses a wide range of products and innovations. Meanwhile, the chemical drug market, a subset of the pharmaceutical industry, was projected to grow from $1,005 billion in 2018 to $1,094 billion by 2022. This growth trajectory highlights the ongoing advancements and investments in drug development and production. The Adenovirus Vaccine Market, with its robust growth rate, stands out within the pharmaceutical landscape, reflecting the critical role of vaccines in addressing public health challenges. The market's expansion is supported by technological advancements, increased research and development activities, and strategic collaborations among key stakeholders. As the demand for vaccines continues to rise, the Adenovirus Vaccine Market is poised to make significant contributions to global health, offering promising opportunities for innovation and investment.

| Report Metric | Details |

| Report Name | Adenovirus Vaccine Market |

| Accounted market size in year | US$ 979 million |

| Forecasted market size in 2031 | US$ 1623 million |

| CAGR | 7.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Teva Pharmaceuticals, Barr Labs |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |