What is Global Hematopoietic Stem Cell Transplantation (HSCT) Market?

Global Hematopoietic Stem Cell Transplantation (HSCT) Market is a rapidly evolving sector within the healthcare industry, focusing on the transplantation of hematopoietic stem cells to treat various blood-related disorders and cancers. These stem cells are crucial as they have the ability to develop into different types of blood cells, including red blood cells, white blood cells, and platelets. The market is driven by the increasing prevalence of blood disorders such as leukemia, lymphoma, and multiple myeloma, which require stem cell transplantation as a part of their treatment regimen. Technological advancements in stem cell collection and transplantation techniques have further propelled the market's growth. Additionally, the rising awareness about stem cell therapies and their potential benefits has led to increased demand for these procedures globally. The market is also influenced by the growing number of stem cell banks and research initiatives aimed at improving transplantation outcomes. As healthcare systems worldwide continue to recognize the importance of stem cell therapies, the Global Hematopoietic Stem Cell Transplantation Market is expected to witness significant growth in the coming years, offering new hope to patients with life-threatening conditions.

Allogeneic, Autologous in the Global Hematopoietic Stem Cell Transplantation (HSCT) Market:

In the realm of Global Hematopoietic Stem Cell Transplantation (HSCT), two primary types of transplants are commonly discussed: Allogeneic and Autologous. Allogeneic transplantation involves the transfer of stem cells from a donor to a recipient. This type of transplant is often used when a patient's own stem cells are not healthy or are insufficient for effective treatment. The donor can be a family member or an unrelated individual whose stem cells closely match the recipient's tissue type. Allogeneic transplants are particularly beneficial for treating conditions like leukemia, where the patient's bone marrow is affected. The introduction of healthy donor stem cells can help rebuild the patient's immune system and combat the disease. However, this type of transplant comes with challenges, such as the risk of graft-versus-host disease (GVHD), where the donor's immune cells attack the recipient's body. To mitigate this risk, careful matching and immunosuppressive therapies are employed. On the other hand, Autologous transplantation involves using the patient's own stem cells. This approach is typically used when the patient's stem cells are healthy but need to be collected and stored before undergoing treatments like chemotherapy or radiation, which can damage the bone marrow. After the treatment, the stored stem cells are reintroduced into the patient's body to restore the bone marrow's function. Autologous transplants are commonly used for conditions such as lymphoma and multiple myeloma. One of the main advantages of autologous transplantation is the reduced risk of immune-related complications since the patient's own cells are used. However, there is a risk of reintroducing cancerous cells if they were present in the harvested stem cells. To address this, techniques like purging are used to remove any residual cancer cells before transplantation. Both allogeneic and autologous transplants have their unique benefits and challenges, and the choice between them depends on various factors, including the patient's condition, the availability of a suitable donor, and the specific goals of the treatment. The Global Hematopoietic Stem Cell Transplantation Market continues to evolve as research and technology advance, offering new possibilities for improving patient outcomes. Innovations in stem cell harvesting, storage, and transplantation techniques are enhancing the safety and efficacy of these procedures. Additionally, the development of targeted therapies and personalized medicine approaches is further shaping the landscape of HSCT. As the understanding of stem cell biology deepens, the potential for more effective and tailored treatments becomes increasingly promising. The market's growth is also supported by the increasing number of clinical trials and research initiatives aimed at exploring new applications and improving existing protocols. As a result, the Global Hematopoietic Stem Cell Transplantation Market is poised for continued expansion, driven by the ongoing quest to provide better treatment options for patients with hematological disorders.

Peripheral Blood Stem Cells Transplant (PBSCT), Bone Marrow Transplant (BMT), Cord Blood Transplant (CBT) in the Global Hematopoietic Stem Cell Transplantation (HSCT) Market:

The Global Hematopoietic Stem Cell Transplantation (HSCT) Market finds its application in various transplantation methods, including Peripheral Blood Stem Cells Transplant (PBSCT), Bone Marrow Transplant (BMT), and Cord Blood Transplant (CBT). Each of these methods has its unique characteristics and applications, contributing to the overall growth and development of the HSCT market. Peripheral Blood Stem Cells Transplant (PBSCT) involves collecting stem cells from the peripheral blood of a donor or patient. This method has gained popularity due to its less invasive nature compared to traditional bone marrow harvesting. PBSCT is often preferred for its quicker recovery time and the ability to collect a larger number of stem cells, which can enhance the chances of successful engraftment. It is commonly used in both allogeneic and autologous transplants, offering flexibility in treatment options. The ease of collection and reduced discomfort for donors make PBSCT an attractive choice for many patients and healthcare providers. Bone Marrow Transplant (BMT) is one of the oldest and most established methods of stem cell transplantation. It involves extracting stem cells directly from the bone marrow, usually from the pelvic bone. BMT is often used when a higher concentration of stem cells is required, or when peripheral blood stem cells are not suitable. This method is particularly effective for treating certain types of leukemia and other blood disorders. Despite being more invasive than PBSCT, BMT remains a critical component of the HSCT market due to its proven efficacy in specific cases. Advances in anesthesia and surgical techniques have improved the safety and comfort of bone marrow harvesting, making it a viable option for many patients. Cord Blood Transplant (CBT) utilizes stem cells collected from the umbilical cord blood of newborns. This method has gained attention for its potential to provide a readily available source of stem cells, especially for patients who do not have a suitable donor match. Cord blood stem cells are less mature than those from other sources, which can reduce the risk of graft-versus-host disease (GVHD) and allow for more flexible matching criteria. CBT is particularly valuable for pediatric patients and those with rare tissue types. The increasing establishment of cord blood banks and the growing awareness of the benefits of cord blood donation have contributed to the expansion of this segment within the HSCT market. Each of these transplantation methods plays a vital role in the Global Hematopoietic Stem Cell Transplantation Market, offering diverse options for patients with different needs and conditions. The choice of method depends on various factors, including the patient's medical condition, the availability of a suitable donor, and the specific goals of the treatment. As research and technology continue to advance, the HSCT market is expected to see further innovations and improvements in transplantation techniques. The ongoing development of new therapies and the increasing understanding of stem cell biology are likely to enhance the effectiveness and safety of these procedures, ultimately benefiting patients worldwide.

Global Hematopoietic Stem Cell Transplantation (HSCT) Market Outlook:

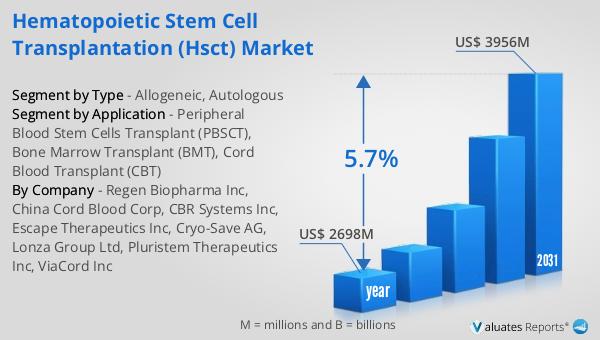

The global market for Hematopoietic Stem Cell Transplantation (HSCT) was valued at approximately $2,698 million in 2024. It is anticipated to grow to a revised size of around $3,956 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.7% over the forecast period. This growth is indicative of the increasing demand for HSCT procedures driven by the rising prevalence of blood disorders and advancements in transplantation techniques. In parallel, the broader global market for medical devices is estimated to be valued at $603 billion in 2023, with a projected growth rate of 5% over the next six years. This growth in the medical devices sector underscores the expanding healthcare landscape and the increasing adoption of advanced medical technologies. The synergy between the HSCT market and the broader medical devices market highlights the interconnectedness of healthcare innovations and the potential for continued advancements in patient care. As the HSCT market continues to evolve, it is poised to play a significant role in the future of medical treatments, offering new hope and improved outcomes for patients with hematological disorders.

| Report Metric | Details |

| Report Name | Hematopoietic Stem Cell Transplantation (HSCT) Market |

| Accounted market size in year | US$ 2698 million |

| Forecasted market size in 2031 | US$ 3956 million |

| CAGR | 5.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Regen Biopharma Inc, China Cord Blood Corp, CBR Systems Inc, Escape Therapeutics Inc, Cryo-Save AG, Lonza Group Ltd, Pluristem Therapeutics Inc, ViaCord Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |