What is Global Virtual Reality (VR) for Consumer Market?

Global Virtual Reality (VR) for the Consumer Market refers to the expansive and rapidly evolving industry focused on delivering immersive virtual experiences to everyday users. This market encompasses a wide range of products and services designed to transport users into simulated environments, offering experiences that can be both entertaining and educational. VR technology has made significant strides in recent years, becoming more accessible and affordable for consumers. It includes various applications such as gaming, virtual tours, education, and social interactions, all of which are enhanced by the immersive nature of VR. The consumer VR market is driven by advancements in technology, including improvements in hardware like headsets and controllers, as well as software developments that create more realistic and engaging virtual worlds. As VR continues to grow, it is expected to transform how people interact with digital content, providing new opportunities for entertainment, learning, and communication. The global VR market for consumers is a dynamic space, constantly evolving with technological innovations and consumer demands, making it an exciting area to watch in the coming years.

Hardware, Software, Solutions in the Global Virtual Reality (VR) for Consumer Market:

The Global Virtual Reality (VR) for Consumer Market is composed of three main components: hardware, software, and solutions, each playing a crucial role in delivering the immersive experiences that VR promises. Hardware is the backbone of VR technology, encompassing devices like headsets, controllers, and sensors that allow users to interact with virtual environments. These devices have seen significant advancements, with modern VR headsets offering high-resolution displays, improved field of view, and enhanced motion tracking capabilities. Companies like Oculus, HTC, and Sony have been at the forefront, pushing the boundaries of what VR hardware can achieve. The development of wireless VR headsets has also been a game-changer, providing users with more freedom of movement and a more seamless experience. On the software side, VR applications and platforms are essential for creating and delivering content. Software developers are tasked with designing virtual worlds and experiences that are not only visually stunning but also interactive and engaging. This includes everything from VR games and simulations to educational programs and virtual social spaces. The software must be optimized to run smoothly on various hardware configurations, ensuring a consistent experience for all users. Solutions in the VR market refer to the integration of hardware and software to address specific consumer needs. This can include VR systems designed for gaming, where the focus is on delivering high-performance graphics and responsive controls, or educational VR solutions that prioritize content delivery and ease of use. Solutions also encompass the development of VR ecosystems, where hardware and software work together seamlessly to provide a comprehensive user experience. Companies are increasingly focusing on creating ecosystems that allow for easy access to a wide range of VR content, enhancing the overall value proposition for consumers. As the VR market continues to grow, the interplay between hardware, software, and solutions will be critical in shaping the future of consumer VR experiences.

3D Audio, Computer Vision, 3D Depth Sensors, 4K & 8K Video, Adaptive Streaming in the Global Virtual Reality (VR) for Consumer Market:

The usage of Global Virtual Reality (VR) for the Consumer Market spans several innovative areas, including 3D audio, computer vision, 3D depth sensors, 4K & 8K video, and adaptive streaming, each contributing to the immersive quality of VR experiences. 3D audio is a crucial component of VR, providing spatial sound that enhances the realism of virtual environments. By simulating how sound waves interact with the environment and reach the listener's ears, 3D audio creates a sense of presence, making users feel as if they are truly inside the virtual world. This technology is essential for applications like gaming and virtual tours, where audio cues can guide users and enhance the overall experience. Computer vision is another vital aspect of VR, enabling devices to interpret and understand the user's physical environment. This technology allows for more accurate motion tracking and interaction within the virtual space, providing a more intuitive and natural user experience. 3D depth sensors work in tandem with computer vision, capturing detailed information about the user's surroundings and movements. These sensors are crucial for creating realistic interactions and ensuring that virtual objects behave as expected in relation to the user's actions. High-resolution video, such as 4K and 8K, is essential for delivering visually stunning VR experiences. These video formats provide the clarity and detail needed to create lifelike virtual environments, enhancing the sense of immersion. Adaptive streaming technology ensures that VR content is delivered smoothly, regardless of the user's internet connection. By adjusting the quality of the video stream in real-time, adaptive streaming minimizes buffering and latency, providing a seamless experience. Together, these technologies form the foundation of the consumer VR market, enabling the creation of rich, immersive experiences that captivate users and push the boundaries of what is possible in virtual reality.

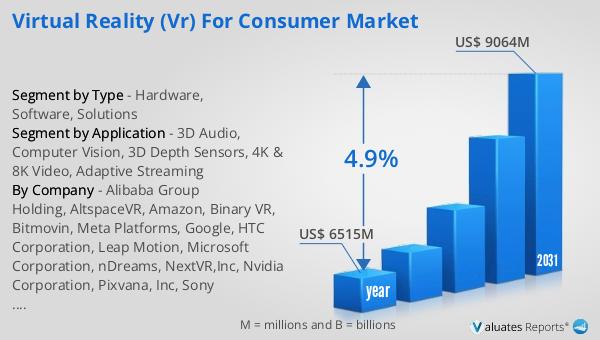

Global Virtual Reality (VR) for Consumer Market Outlook:

The global market for Virtual Reality (VR) for consumers has shown promising growth and potential. In 2024, the market was valued at approximately US$ 6,515 million, reflecting the increasing interest and investment in VR technologies. This market is projected to expand significantly, reaching an estimated size of US$ 9,064 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.9% over the forecast period. The steady increase in market size can be attributed to several factors, including advancements in VR technology, increased consumer awareness, and the growing availability of VR content. As more consumers become familiar with VR and its potential applications, demand for VR products and services is expected to rise. Additionally, the development of more affordable and user-friendly VR devices is likely to drive further adoption among consumers. The market's growth is also supported by the expanding range of VR applications, from gaming and entertainment to education and virtual tourism. As the VR market continues to evolve, it is poised to become an integral part of the consumer technology landscape, offering new and exciting ways for people to interact with digital content.

| Report Metric | Details |

| Report Name | Virtual Reality (VR) for Consumer Market |

| Accounted market size in year | US$ 6515 million |

| Forecasted market size in 2031 | US$ 9064 million |

| CAGR | 4.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Alibaba Group Holding, AltspaceVR, Amazon, Binary VR, Bitmovin, Meta Platforms, Google, HTC Corporation, Leap Motion, Microsoft Corporation, nDreams, NextVR,Inc, Nvidia Corporation, Pixvana, Inc, Sony Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |