What is Fiber Splicing Equipment - Global Market?

Fiber splicing equipment is a crucial component in the telecommunications and data transmission industries, playing a vital role in connecting optical fibers to ensure seamless data flow. This equipment is used to join two fiber optic cables end-to-end, allowing for the transmission of light signals with minimal loss. The global market for fiber splicing equipment is driven by the increasing demand for high-speed internet and the expansion of telecommunication networks worldwide. As more regions adopt fiber optic technology for faster and more reliable internet connections, the need for efficient and precise splicing equipment has grown. This market encompasses various types of splicing equipment, including fusion splicers and mechanical splicers, each catering to different needs and applications. Fusion splicers, for instance, are known for their precision and are widely used in industries where high-quality connections are essential. The market is also influenced by technological advancements, which have led to the development of more sophisticated and user-friendly splicing equipment. As a result, the fiber splicing equipment market is poised for continued growth, driven by the ongoing expansion of fiber optic networks and the increasing demand for high-speed data transmission solutions.

Single Fiber Splicing Equipment, Ribbon Fiber Splicing Equipment, Special Fiber Splicing Equipment in the Fiber Splicing Equipment - Global Market:

Single fiber splicing equipment is designed to splice individual optical fibers, making it ideal for applications where precision and accuracy are paramount. This type of equipment is commonly used in telecommunications, data centers, and other industries where high-quality fiber optic connections are essential. Single fiber splicers are known for their ability to create low-loss splices, ensuring that data transmission remains efficient and reliable. These splicers typically use fusion splicing technology, which involves aligning the fibers and then fusing them together using an electric arc. This process results in a strong and durable splice that can withstand various environmental conditions. Ribbon fiber splicing equipment, on the other hand, is designed to splice multiple fibers simultaneously, making it a more efficient option for large-scale projects. This type of equipment is often used in applications where multiple fibers need to be spliced quickly and accurately, such as in the construction of fiber optic networks. Ribbon splicers can splice up to 12 fibers at once, significantly reducing the time and effort required for large-scale splicing projects. Special fiber splicing equipment is designed for unique applications that require specialized splicing techniques. This type of equipment is often used in industries such as aerospace, defense, and medical, where specialized fibers and splicing techniques are required. Special splicers may be used to splice fibers with different core sizes, shapes, or materials, making them a versatile option for a wide range of applications. These splicers often incorporate advanced technologies and features to ensure precise and reliable splicing, even in challenging conditions. The global market for fiber splicing equipment is diverse, with a wide range of products available to meet the needs of various industries and applications. As the demand for high-speed data transmission continues to grow, the market for fiber splicing equipment is expected to expand, driven by the increasing adoption of fiber optic technology and the need for efficient and reliable splicing solutions.

Communication, Electronics and Semiconductors, Others in the Fiber Splicing Equipment - Global Market:

Fiber splicing equipment plays a crucial role in various industries, including communication, electronics and semiconductors, and others. In the communication sector, fiber splicing equipment is essential for the construction and maintenance of fiber optic networks. These networks form the backbone of modern telecommunications, enabling high-speed internet, voice, and data services. Fiber splicing equipment ensures that these networks are built and maintained with precision, allowing for seamless data transmission and minimal signal loss. As the demand for faster and more reliable internet connections continues to grow, the need for efficient and accurate fiber splicing equipment in the communication sector is more important than ever. In the electronics and semiconductors industry, fiber splicing equipment is used to connect optical fibers in various devices and systems. These connections are critical for the performance and reliability of electronic devices, as they enable the transmission of data at high speeds and with minimal interference. Fiber splicing equipment ensures that these connections are made with precision, allowing for optimal performance and reliability. As the electronics and semiconductors industry continues to evolve, the demand for advanced fiber splicing equipment is expected to increase, driven by the need for faster and more efficient data transmission solutions. In addition to communication and electronics, fiber splicing equipment is also used in other industries, such as aerospace, defense, and medical. In these industries, fiber splicing equipment is used to connect specialized fibers that are used in various applications, such as sensors, imaging systems, and communication devices. These connections are critical for the performance and reliability of these systems, as they enable the transmission of data and signals with precision and accuracy. As these industries continue to grow and evolve, the demand for specialized fiber splicing equipment is expected to increase, driven by the need for advanced and reliable splicing solutions. Overall, the global market for fiber splicing equipment is diverse and dynamic, with a wide range of applications and industries driving demand for these essential tools.

Fiber Splicing Equipment - Global Market Outlook:

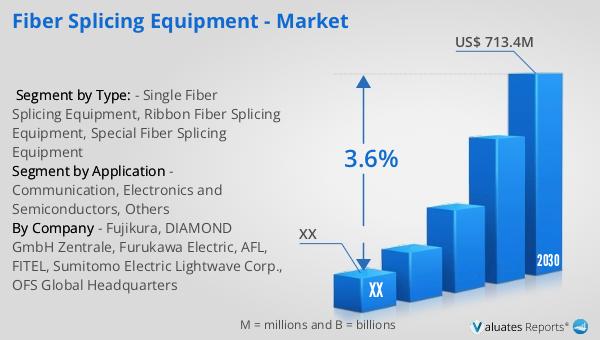

The global market for fiber splicing equipment was valued at approximately $555 million in 2023 and is projected to grow to around $713.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.6% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for high-speed data transmission solutions and the expansion of fiber optic networks worldwide. The North American market for fiber splicing equipment, in particular, is expected to experience significant growth during this period, driven by the ongoing development of telecommunications infrastructure and the increasing adoption of fiber optic technology. While specific figures for the North American market were not provided, it is anticipated that this region will contribute significantly to the overall growth of the global market. The steady increase in demand for fiber splicing equipment can be attributed to the growing need for efficient and reliable data transmission solutions across various industries, including telecommunications, electronics, and others. As more regions invest in the development of fiber optic networks, the market for fiber splicing equipment is expected to continue its upward trajectory, driven by the need for advanced and precise splicing solutions.

| Report Metric | Details |

| Report Name | Fiber Splicing Equipment - Market |

| Forecasted market size in 2030 | US$ 713.4 million |

| CAGR | 3.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Fujikura, DIAMOND GmbH Zentrale, Furukawa Electric, AFL, FITEL, Sumitomo Electric Lightwave Corp., OFS Global Headquarters |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |