What is Global Liquid Polysulfide Polymer Market?

The Global Liquid Polysulfide Polymer Market is an intriguing sector that delves into the production and distribution of a unique type of polymer known for its exceptional durability and flexibility. This market focuses on the synthesis and application of liquid polysulfide polymers, which are primarily utilized in various industrial applications due to their superior properties such as chemical resistance, waterproofing, and insulating capabilities. At its core, the market caters to a wide range of industries, including construction, aerospace, automotive, and marine sectors, providing them with critical materials that enhance the longevity and performance of their products. As of 2023, the market has been valued at a significant figure, showcasing its importance and the growing demand for these polymers across the globe. The industry's dynamics are influenced by technological advancements, environmental regulations, and the evolving needs of the end-use sectors, making it a vital component of the modern industrial landscape.

Thiol-terminated Type, Epoxy-terminated Type in the Global Liquid Polysulfide Polymer Market:

Diving into the specifics of the Global Liquid Polysulfide Polymer Market, we encounter two primary types of these polymers: Thiol-terminated and Epoxy-terminated. Thiol-terminated polysulfide polymers are known for their exceptional ability to cure at room temperature, offering a versatile solution for sealing and bonding applications. This type is widely appreciated in industries that require materials with high elasticity, good chemical resistance, and waterproofing capabilities. On the other hand, Epoxy-terminated polysulfide polymers are designed to enhance adhesion and mechanical properties when cured, making them ideal for more demanding applications that require robust, durable bonds. These polymers are particularly valued in sectors that demand high-performance materials capable of withstanding harsh environmental conditions, such as the aerospace and construction industries. The distinction between these two types lies in their chemical structure and curing mechanisms, which directly influence their application potential and performance in various industrial settings. The market's depth is further enriched by the ongoing research and development activities aimed at improving the efficiency, sustainability, and application range of these polymers, ensuring that they continue to meet the evolving demands of their diverse user base.

Building and Construction, Aerospace, Automotive, Marine, Others in the Global Liquid Polysulfide Polymer Market:

The usage of Global Liquid Polysulfide Polymer in various sectors such as Building and Construction, Aerospace, Automotive, Marine, among others, highlights its versatility and critical importance across different industries. In the Building and Construction sector, these polymers are extensively used for waterproofing, sealing, and repairing, providing long-lasting protection against moisture and environmental degradation. The Aerospace industry benefits from the high-performance characteristics of liquid polysulfide polymers, utilizing them in sealing applications that demand exceptional chemical and temperature resistance. Automotive manufacturers incorporate these polymers for their durability and flexibility, using them in sealants and coatings that enhance vehicle longevity and performance. The Marine sector relies on the waterproof and corrosion-resistant properties of liquid polysulfide polymers to protect ships and marine structures from the harsh marine environment. Additionally, other industries leverage these polymers for various applications, including but not limited to, coatings, adhesives, and insulation, showcasing the broad applicability and significance of liquid polysulfide polymers in modern industrial practices. The widespread use of these materials underscores their integral role in enhancing the durability, safety, and efficiency of products and structures across a multitude of sectors.

Global Liquid Polysulfide Polymer Market Outlook:

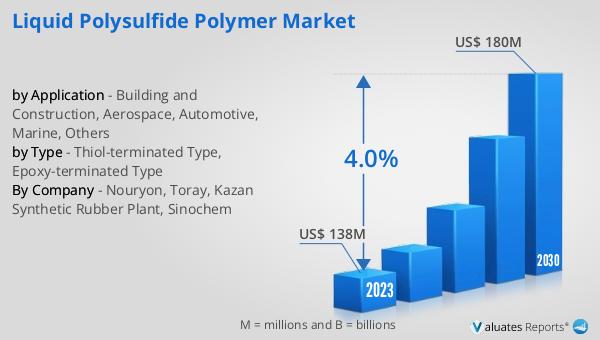

The market outlook for Global Liquid Polysulfide Polymer presents a promising future, with its valuation set at US$ 138 million in 2023 and an anticipated growth to reach US$ 180 million by 2030. This growth trajectory, marked by a Compound Annual Growth Rate (CAGR) of 4.0% during the forecast period from 2024 to 2030, underscores the increasing demand and potential of this market. A significant concentration of market share is held by the top four manufacturers, who collectively account for approximately 94% of the global market, with Nouryon standing out as the largest manufacturer, holding around 54% of the market share. This concentration highlights the competitive landscape and the dominance of key players within the market. From a downstream market perspective, the Building and Construction segment emerges as the largest, claiming about 67% of the market share. This is followed by the Aerospace sector, which holds a substantial 24% share. These figures not only reflect the diverse applications of liquid polysulfide polymers but also indicate the sectors where their impact and utility are most pronounced. The market's growth and the distribution of shares among different sectors and manufacturers provide valuable insights into the current state and future prospects of the Global Liquid Polysulfide Polymer Market.

| Report Metric | Details |

| Report Name | Liquid Polysulfide Polymer Market |

| Accounted market size in 2023 | US$ 138 million |

| Forecasted market size in 2030 | US$ 180 million |

| CAGR | 4.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nouryon, Toray, Kazan Synthetic Rubber Plant, Sinochem |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |