What is Global Precision Planetary Gear Reducers Market?

The Global Precision Planetary Gear Reducers Market is a specialized segment within the broader gear reducer industry, focusing on high-precision, high-efficiency gear systems designed to decrease motor speed while increasing torque in various mechanical devices. These gear reducers are integral to numerous applications across a wide range of industries due to their superior attributes, including minimal backlash, high torsional stiffness, and exceptional accuracy. Precision planetary gear reducers are particularly favored for their compact design and robust performance, making them ideal for use in spaces where efficiency and precision are paramount. The market's growth is propelled by the increasing demand for automation and robotics across manufacturing sectors, as well as the ongoing advancements in gear technology that enhance the performance and reliability of these components. As industries continue to seek more efficient and precise motion control solutions, the global precision planetary gear reducers market is expected to witness significant growth, offering innovative solutions that meet the evolving needs of modern machinery and equipment.

Right Angle Precision Planetary Reducer, Parallel Output Shaft Precision Planetary Reducer in the Global Precision Planetary Gear Reducers Market:

Diving into the specifics of the Global Precision Planetary Gear Reducers Market, we find two main types that stand out due to their unique configurations and applications: the Right Angle Precision Planetary Reducer and the Parallel Output Shaft Precision Planetary Reducer. The Right Angle Precision Planetary Reducer is distinguished by its 90-degree angle output, which is particularly useful in tight spaces where a straight, in-line application is not feasible. This type of reducer is often employed in scenarios where space constraints demand a compact solution without sacrificing performance. On the other hand, the Parallel Output Shaft Precision Planetary Reducer features an output shaft that is parallel to the motor shaft, making it ideal for applications requiring a straightforward, linear approach. This variant is celebrated for its versatility and is commonly used in a variety of industrial applications where alignment and space are less of a concern. Both types of reducers are critical components in the global market, catering to a wide array of industrial needs by offering solutions that enhance precision, efficiency, and reliability in machinery. Their applications span across robotics, aerospace, automotive, and many other sectors, underscoring their importance in the advancement of modern industrial practices. The ongoing development and refinement of these reducers continue to open new avenues for their application, further solidifying their position in the global market as indispensable tools for achieving high precision and efficiency in mechanical operations.

Robot, Food Processing Machinery Industry, Packaging Machinery Industry, Textile and Printing Machinery Industry, Semiconductor Equipment Industry, Machine Tool, Aerospace, Medical Equipment, Construction Machinery, Others in the Global Precision Planetary Gear Reducers Market:

The Global Precision Planetary Gear Reducers Market finds its applications sprawling across a diverse range of industries, each benefiting from the precision and efficiency these components bring to machinery and equipment. In robotics, precision planetary gear reducers are crucial for ensuring the smooth, accurate movements required in automation and manufacturing processes. The food processing machinery industry relies on these reducers for the precise control necessary in handling and packaging delicate products. Similarly, the packaging machinery industry benefits from the high precision and efficiency of these gear reducers, enabling faster and more reliable packaging processes. In the textile and printing machinery industry, precision planetary gear reducers contribute to the fine control over machinery, essential for producing high-quality prints and textiles. The semiconductor equipment industry, where precision and reliability are paramount, utilizes these reducers to maintain the high standards required for semiconductor manufacturing. Machine tools, aerospace, medical equipment, and construction machinery industries also leverage the advanced technology of precision planetary gear reducers to enhance the performance and reliability of their equipment. Furthermore, these reducers find applications in other sectors, highlighting their versatility and critical role in modern industrial operations. The widespread use of precision planetary gear reducers across these industries underscores their importance in the advancement of technology and efficiency in various fields, driving innovation and productivity in the global market.

Global Precision Planetary Gear Reducers Market Outlook:

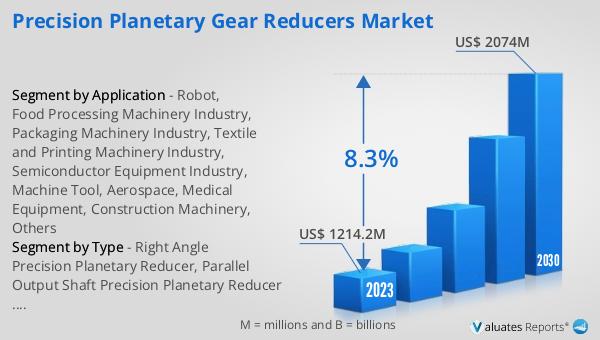

The market outlook for the Global Precision Planetary Gear Reducers Market presents a promising future, with its valuation at US$ 1214.2 million in 2023, and projections suggesting a climb to US$ 2074 million by 2030. This anticipated growth, marked by a Compound Annual Growth Rate (CAGR) of 8.3% during the forecast period from 2024 to 2030, underscores the increasing demand and potential within this sector. Nidec, a leading player, has carved out a significant portion of the market, securing a 12.64% share of the global Precision Planetary Reducers revenue in 2022. Other notable companies, including Neugart GmbH and Wittenstein SE, have also established themselves with shares of 9.23% and 9.14%, respectively. This competitive landscape highlights the dynamic nature of the market, with key players driving innovation and growth through their contributions. The increasing reliance on precision planetary gear reducers across various industries, from robotics to aerospace, further fuels this growth, reflecting the critical role these components play in modern machinery and equipment. As the market continues to expand, the focus on enhancing efficiency, precision, and reliability in industrial operations is expected to propel the demand for precision planetary gear reducers, making it a key area of interest for stakeholders in the coming years.

| Report Metric | Details |

| Report Name | Precision Planetary Gear Reducers Market |

| Accounted market size in 2023 | US$ 1214.2 million |

| Forecasted market size in 2030 | US$ 2074 million |

| CAGR | 8.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nidec, Neugart GmbH, Wittenstein SE, Apex Dynamics, KOFON Motion Group, LI-MING Machinery, Newstart, Rouist, STOBER, Harmonic Drive Systems, Ningbo ZhongDa Leader, ZF, Sesame Motor, Sumitomo, PIN HONG TECHNOLOGY, Shanghai Lian Heng Precision Machinery, Shenzhen Zhikong Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |